Capital One 2012 Annual Report Download - page 122

Download and view the complete annual report

Please find page 122 of the 2012 Capital One annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

|

|

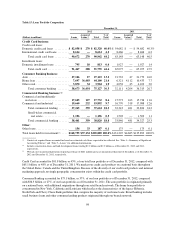

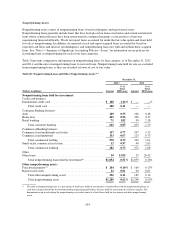

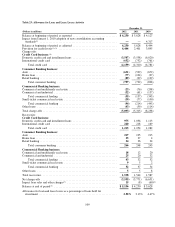

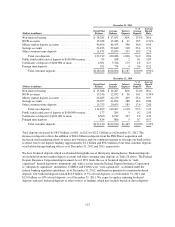

Table 18 presents an aging of 30+ day delinquent loans included in the above table.

Table 18: Aging and Geography of 30+ Day Delinquent Loans

December 31,

2012 2011

(Dollars in millions) Amount

% of

Total Loans(1) Amount

% of

Total Loans(1)

Total loan portfolio ................................. $205,889 100.0% $135,892 100.00%

Delinquency status:

30 – 59 days .................................. $ 2,664 1.29% $ 2,306 1.70%

60 – 89 days .................................. 1,440 0.70 1,092 0.80

90 + days ..................................... 2,256 1.10 1,970 1.45

Total ............................................ $ 6,360 3.09% $ 5,368 3.95%

Geographic region:

Domestic ..................................... $ 6,052 2.94% $ 4,930 3.63%

International ................................... 308 0.15 438 0.32

Total ............................................ $ 6,360 3.09% $ 5,368 3.95%

(1) Calculated by dividing loans in each delinquency status category or geographic region as of the end of the period by the total held-for-

investment loan portfolio, including acquired loans.

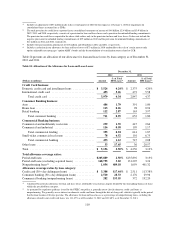

Table 19 summarizes loans that were 90 days or more past due as to interest or principal and still accruing

interest as of December 31, 2012, 2011 and 2010. These loans consist primarily of credit card accounts between

90 days and 179 days past due. As permitted by regulatory guidance issued by the Federal Financial Institutions

Examination Council (“FFIEC”), we generally continue to accrue interest on domestic credit card loans through

the date of charge-off, which is typically in the period the account becomes 180 days past due. While domestic

credit card loans typically remain on accrual status until the loan is charged-off, we establish a reserve for

finance charges and fees billed but not expected to be collected and exclude this amount from revenue.

Table 19: 90+ Days Delinquent Loans Accruing Interest

(Dollars in millions)

December 31,

2012 2011 2010

Amount

% of

Total Loans Amount

% of

Total Loans Amount

% of

Total Loans

Loan category: (1)

Credit card(2) .......................... $1,510 1.65% $1,196 1.84% $1,379 2.25%

Consumer ............................ 1 0.00 5 0.01 5 0.01

Commercial .......................... 16 0.04 41 0.12 14 0.05

Total ............................ $1,527 0.74% $1,242 0.91% $1,398 1.11%

Geographic region:(3)

Domestic ............................ $1,427 0.69% $1,047 0.77% $1,195 0.95%

International .......................... 100 0.05 195 0.14 203 0.16

Total ............................ $1,527 0.74% $1,242 0.91% $1,398 1.11%

(1) Delinquency rates are calculated by loan category by dividing 90+ day delinquent loans accruing interest as of the end of the period by

period-end loans held for investment for the specified loan category, including acquired loans as applicable.

(2) Includes credit card loans that continue to accrue finance charges and fees until charged-off, which is typically at 180 days past due. The

amounts reported for credit card loans are net of billed finance charges and fees that we do not expect to collect. The estimated

uncollectible portion of billed finance charges and fees excluded from revenue totaled $937 million, $371 million and $950 million in

2012, 2011 and 2010, respectively. The reserve for uncollectible billed finance charges and fees totaled $307 million, $74 million and

$211 million as of December 31, 2012, 2011 and 2010, respectively.

(3) Calculated by dividing loans in each geographic region as of the end of the period by the total loan portfolio.

103