Capital One 2012 Annual Report Download - page 68

Download and view the complete annual report

Please find page 68 of the 2012 Capital One annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

|

|

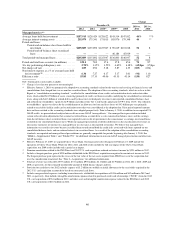

Business Segment Expectations

Credit Card Business

As noted above, in Domestic Card, the closing of the 2012 U.S. card acquisition has impacted and will continue

to affect quarterly trends in loan growth, revenue margin and credit metrics. We anticipate that the run-off of

parts of the portfolio acquired in the 2012 U.S. card acquisition as well as anticipated run-off of in our

installment loan portfolio will more than offset the underlying growth trajectory in other parts of our Domestic

Card business resulting in a modest decline in full-year average loan balances in 2013 from average loan

balances in the fourth quarter of 2012. In addition, the sale of the Best Buy loan portfolio will result in an

incremental reduction in loans held for investment of approximately $7 billion. We expect charge-off levels to

remain relatively stable with normal seasonal patterns in 2013.

As we have disclosed in the past, we are taking actions that we believe will enhance our franchise, such as

aligning customer practices related to the 2012 U.S. card acquisition with our own, and ending the sale of

products like payment protection, which will have a modest negative impact on revenue margin. We also expect

that the run-off of higher-margin, higher-loss receivables purchased in the 2012 U.S. card acquisition will change

the mix of loans in our Domestic Card business, driving a further modest reduction of revenue margin in 2013.

We expect the sale of the Best Buy portfolio, which resulted in our transferring these loans to held for sale from

held for investment in the first quarter of 2013, and the related held-for-sale loan accounting will increase our

revenue margins until the sale of the loans. Other factors which we are unable to accurately predict will also

affect revenue margin. These factors, which include market and pricing dynamics, credit trends, and competitive

intensity, could have positive or negative impacts on the Domestic Card revenue margin.

Consumer Banking Business

In our Consumer Banking business, we expect the ING Direct acquisition to continue to have a significant impact

on Consumer Banking loan volumes as we anticipate that run-off in the acquired Home Loans portfolio will more

than offset growth in auto loans.

Commercial Banking Business

Our Commercial Banking business continues to grow loans, deposits, and revenues as we attract new customers

and deepen relationships with existing customers. Although we anticipate some quarterly fluctuations in

nonperforming loan and charge-off rates, we expect our Commercial Banking business to continue strong and

relatively steady performance trends throughout 2013.

CRITICAL ACCOUNTING POLICIES AND ESTIMATES

The preparation of financial statements in accordance with U.S. GAAP requires management to make a number

of judgments, estimates and assumptions that affect the reported amount of assets, liabilities, income and

expenses in the consolidated financial statements. Understanding our accounting policies and the extent to which

we use management judgment and estimates in applying these policies is integral to understanding our financial

statements. We provide a summary of our significant accounting policies in “Note 1—Summary of Significant

Accounting Policies.”

49