Capital One 2012 Annual Report Download - page 235

Download and view the complete annual report

Please find page 235 of the 2012 Capital One annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

225 -

226

226 -

227

227 -

228

228 -

229

229 -

230

230 -

231

231 -

232

232 -

233

233 -

234

234 -

235

235 -

236

236 -

237

237 -

238

238 -

239

239 -

240

240 -

241

241 -

242

242 -

243

243 -

244

244 -

245

245 -

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

|

|

CAPITAL ONE FINANCIAL CORPORATION

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS—(Continued)

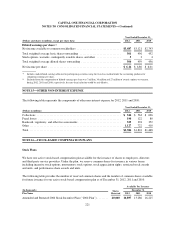

to demand immediate and ongoing full overnight collateralization on derivative instruments in a net liability

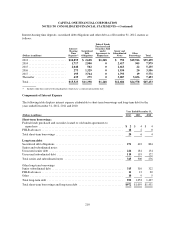

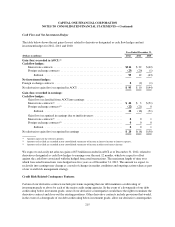

position. Certain of our derivative contracts may allow, in the event of a downgrade of our debt credit rating of

any kind, our derivative counterparties to demand additional collateralization on such derivative instruments in a

net liability position. The fair value of derivative instruments with credit-risk-related contingent features in a net

liability position was $7 million and $141 million as of December 31, 2012 and 2011, respectively. We were

required to post collateral, consisting of a combination of cash and securities, totaling $109 million and

$353 million as of December 31, 2012 and 2011, respectively. If our debt credit rating had fallen below

investment grade, we would have been required to post additional collateral of $4 million and $39 million as of

December 31, 2012 and 2011, respectively.

Derivative Counterparty Credit Risk

Derivative instruments contain an element of credit risk that arises from the potential failure of a counterparty to

perform according to the contractual terms of the contract. Our exposure to derivative counterparty credit risk, at

any point in time, is represented by the fair value of derivatives in a gain position, or derivative assets, assuming

no recoveries of underlying collateral. To mitigate the risk of counterparty default, we maintain collateral

agreements with certain derivative counterparties. These agreements typically require both parties to maintain

collateral in the event the fair values of derivative financial instruments exceed established thresholds. We

received cash collateral from derivatives counterparties totaling $922 million and $894 million as of

December 31, 2012 and 2011, respectively. We also received securities from derivatives counterparties totaling

$239 million as of December 31, 2012, which we have the ability to repledge. We posted cash collateral in

accounts maintained by derivative counterparties totaling $109 million and $353 million as of December 31,

2012 and 2011, respectively.

We record counterparty credit risk valuation adjustments on our derivative assets to properly reflect the credit

quality of the counterparty. We consider collateral and legally enforceable master netting agreements that

mitigate our credit exposure to each counterparty in determining the counterparty credit risk valuation

adjustment, which may be adjusted in future periods due to changes in the fair value of the derivative contract,

collateral and creditworthiness of the counterparty. The cumulative counterparty credit risk valuation adjustment

recorded on our consolidated balance sheets as a reduction in the derivative asset balance was $9 million and

$25 million as of December 31, 2012 and 2011, respectively. We also adjust the fair value of our derivative

liabilities to reflect the impact of our credit quality. We calculate this adjustment by comparing the spreads on

our credit default swaps to the discount benchmark curve. The cumulative credit risk valuation adjustment related

to our credit quality recorded on our consolidated balance sheets as a reduction in the derivative liability balance

was $1 million and $2 million as of December 31, 2012 and 2011, respectively.

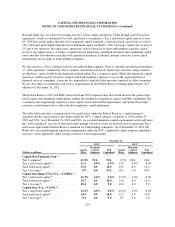

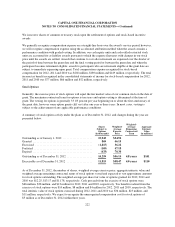

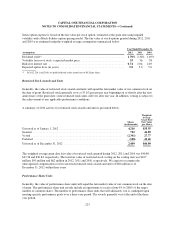

NOTE 12—STOCKHOLDERS’ EQUITY

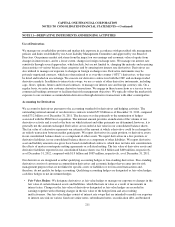

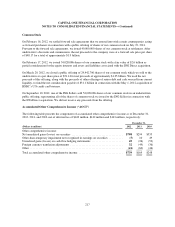

Preferred Stock

On August 20, 2012, we issued and sold 35,000,000 depositary shares (“Depositary Shares”), each representing a

1/40th interest in a share of Fixed Rate Non-Cumulative Perpetual Preferred Stock, Series B, $0.01 par value,

with a liquidation preference of $25.00 per Depositary Share (equivalent to $1,000 per share of Series B

Preferred Stock) (the “Series B Preferred Stock”). Dividends will accrue on the Series B Preferred Stock at a rate

of 6% per annum, payable quarterly in arrears. The net proceeds of the offering of the 35,000,000 Depositary

Shares were approximately $853 million, after deducting underwriting commissions and offering expenses.

216