Capital One 2011 Annual Report Download - page 93

Download and view the complete annual report

Please find page 93 of the 2011 Capital One annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

|

|

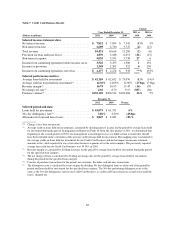

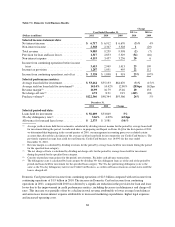

•Charge-off and Delinquency Statistics: The net charge-off rate decreased to 1.39% in 2011 from 1.82% in

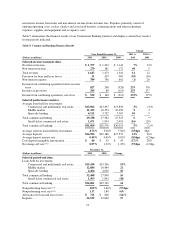

2010. The 30+ day delinquency rate was 5.99% as of December 31, 2011, compared with 5.96% as of

December 31, 2010. The improvement in the net charge-off rate reflects the impact from strong underlying

credit performance trends and the higher credit quality of our more recent auto loan vintages, as well as

current favorable benefits from elevated auction prices. Our home loan credit performance remained stable

during 2011.

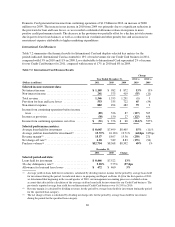

Key factors affecting the results of our Consumer Banking business for 2010, compared with 2009 included the

following:

•Net Interest Income: Net interest income increased by $496 million, or 15%, in 2010. The primary drivers of

the increase in net interest income were improved loan margins, primarily resulting from higher pricing for

new auto loan originations, deposit growth resulting from our continued strategy to leverage our banking

branches to attract lower cost funding sources and improved deposit spreads. The favorable impact from

these factors more than offset the decline in average loans held for investment resulting from the continued

run-off of home loans and reduction in auto loans in 2010.

•Non-Interest Income: Non-interest income increased by $115 million, or 15%, in 2010. The increase was

primarily attributable to a gain of $128 million recorded in the first quarter of 2010 related to the

deconsolidation of certain option-adjustable rate mortgage trusts that were consolidated on January 1, 2010

as a result of our adoption of the new consolidation accounting standards.

•Provision for Loan and Lease Losses: The provision for loan and lease losses decreased by $635 million in

2010, to $241 million. The substantial reduction in the provision was attributable to continued improvement

in credit performance trends and reduced loan balances. Delinquency and charge-off rates declined

throughout the year, reflecting the impact of the gradual improvement in economic conditions and the

higher credit quality of our most recent auto loan vintages. As a result, the Consumer Banking business

recorded a net allowance release (after taking into consideration the impact of the $73 million addition to

the allowance on January 1, 2010 from the adoption of the new consolidation accounting standards) of $474

million in 2010. In comparison, the Consumer Banking business recorded an allowance release of $238

million in 2009, primarily due to declining loan balances.

•Non-Interest Expense: Non-interest expense increased by $216 million, or 8%, in 2010. This increase was

largely attributable to infrastructure expenditures, primarily in our home loan and retail banking operations,

made in 2010 to attract and support new business volume and to integrate Chevy Chase Bank, and increased

marketing expenditures related to our retail banking operations.

•Total Loans: Period-end loans declined by $3.8 billion, or 10%, in 2010 to $34.4 billion as of December 31,

2010, from $38.2 billion as of December 31, 2009, primarily due to the run-off of home loans and a

reduction in auto loan balances.

•Deposits: Period-end deposits increased by $8.8 billion, or 12%, during 2010 to $83.0 billion as of

December 31, 2010, reflecting the impact of our strategy to replace maturing higher cost wholesale funding

sources with lower cost funding sources and our increased retail marketing efforts to attract new business to

meet this objective.

•Charge-off and Delinquency Statistics: The net charge-off and delinquency rates improved during 2010 as a

result of the improved economic environment and a tightening of our underwriting standards on new loan

originations. The net charge-off rate decreased to 1.82% in 2010, down significantly from the net charge-off

rate of 2.74% for 2009. The 30+ day delinquency rate for 2010 also improved from 2009.

Commercial Banking Business

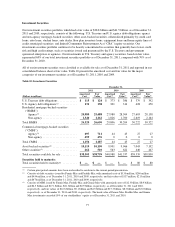

Our Commercial Banking business generated net income from continuing operations of $532 million in 2011,

compared with net income from continuing operations of $160 million in 2010 and a net loss from continuing

operations of $213 million in 2009. The primary sources of revenue for our Commercial Banking business are

73