Capital One 2011 Annual Report Download - page 79

Download and view the complete annual report

Please find page 79 of the 2011 Capital One annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

|

|

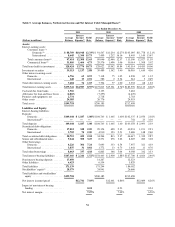

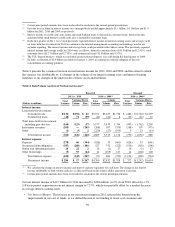

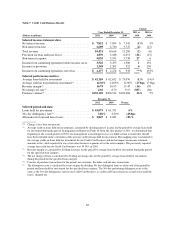

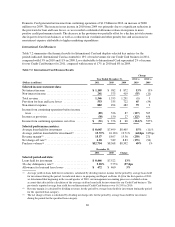

(1) Certain prior period amounts have been reclassified to conform to the current period presentation.

(2) Past due fees included in interest income on a managed basis totaled approximately $1.1 billion, $1.1 billion and $1.4

billion for 2011, 2010 and 2009, respectively.

(3) Interest income on credit card, auto, home and retail banking loans is reflected in consumer loans. Interest income

generated from small business credit cards also is included in consumer loans.

(4) In the first quarter of 2011, we revised previously reported interest income on interest-earning assets and average yield

on loans held for investment for 2010 to conform to the internal management accounting methodology used in our

segment reporting. The interest income and average loan yields presented reflect this revision. The previously reported

interest income and average yields for 2010 were as follows: domestic consumer loans ($11.5 billion and 12.51%); total

consumer loans ($12.7 billion and 12.79%); and commercial loans ($1.3 billion and 4.32%).

(5) The U.K. deposit business, which was included in international deposits, was sold during the third quarter of 2009.

(6) Includes a reduction of $2.9 billion recorded on January 1, 2010, in conjunction with the adoption of the new

consolidation accounting guidance.

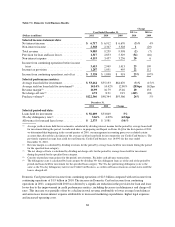

Table 4 presents the variances between our net interest income for 2011, 2010 and 2009, and the extent to which

the variance was attributable to: (i) changes in the volume of our interest-earning assets and interest-bearing

liabilities or (ii) changes in the interest rates of these assets and liabilities.

Table 4: Rate/Volume Analysis of Net Interest Income(1)

Reported Managed

2011 vs. 2010 2010 vs. 2009(2) 2010 vs. 2009(2)

Total

Variance

Variance Due to Total

Variance

Volume Total

Variance

Variance Due to

(Dollars in millions) Volume Rate Volume Rate Volume Rate

Interest income:

Loans held-for-investment:

Consumer loans ......... $(132) $(194) $ 62 $5,191 $3,455 $1,736 $ (481) $(1,740) $1,259

Commercial loans ........ (28) 71 (99) (14) (22) 8 (12) (22) 10

Total loans held for investment,

including past-due fees ...... (160) (123) (37) 5,177 3,433 1,744 (493) (1,762) 1,269

Investment securities ......... (205) — (205) (268) 107 (375) (268) 107 (375)

Other ...................... (1) (3) 2 (220) (27) (193) 9 23 (14)

Total interest income ..... (366) (126) (240) 4,689 3,513 1,176 (752) (1,632) 880

Interest expense:

Deposits ................... (278) 66 (344) (628) 33 (661) (628) 33 (661)

Securitized debt obligations .... (387) (286) (101) 527 752 (225) (526) (318) (208)

Senior and subordinated notes . . 24 22 2 16 (1) 17 16 (1) 17

Other borrowings ............ (9) 55 (64) 14 (103) 117 14 (104) 118

Total interest expense ..... (650) (143) (507) (71) 681 (752) (1,124) (390) (734)

Net interest income ....... $ 284 $ 17 $ 267 $4,760 $2,832 $1,928 $ 372 $(1,242) $1,614

(1) We calculate the change in interest income and interest expense separately for each item. The change in net interest

income attributable to both volume and rates is allocated based on the relative dollar amount of each item.

(2) Certain prior period amounts have been reclassified to conform to the current period presentation.

Our net interest income of $12.7 billion for 2011 increased by $284 million, or 2%, from 2010, driven by a 3%

(18 basis points) expansion in our net interest margin to 7.27%, which was partially offset by a modest decrease

in average interest-earning assets.

•Net Interest Margin: The increase in our net interest margin in 2011 reflected the benefit from the

improvement in our cost of funds, as we shifted the mix of our funding to lower cost consumer and

59