Capital One 2011 Annual Report Download - page 108

Download and view the complete annual report

Please find page 108 of the 2011 Capital One annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

|

|

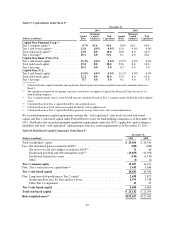

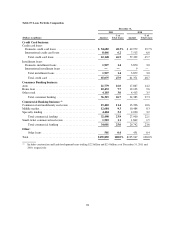

(1) Calculated under capital standards and regulations based on the international capital framework commonly known as

Basel I.

(2) Amounts presented are net of tax.

(3) Disallowed goodwill and other intangible assets are net of related deferred tax liability.

(4) Consists primarily of trust preferred securities.

(5) Under regulatory guidelines for risk-based capital, on-balance sheet assets and credit equivalent amounts of derivatives

and off-balance sheet items are assigned to one of several broad risk categories according to the obligor or, if relevant,

the guarantor or the nature of any collateral. The aggregate dollar amount in each risk category is then multiplied by the

risk weight associated with that category. The resulting weighted values from each of the risk categories are aggregated

for determining total risk-weighted assets.

In November 2011, the Federal Reserve finalized capital planning rules applicable to large bank holding

companies like us (commonly referred to as Comprehensive Capital Analysis and Review or CCAR). Under the

rules, bank holding companies with consolidated assets of $50 billion or more must submit capital plans to the

Federal Reserve on an annual basis and must obtain approval from the Federal Reserve before making most

capital distributions. The purpose of the rules is to ensure that large bank holding companies have robust,

forward-looking capital planning processes that account for their unique risks and capital needs to continue

operations through times of economic and financial stress. As part of its evaluation of a capital plan, the Federal

Reserve will consider the comprehensiveness of the plan, the reasonableness of assumptions and analysis and

methodologies used to assess capital adequacy and the ability of the bank holding company to maintain capital

above each minimum regulatory capital ratio and above a Tier 1 common ratio of 5% on a pro forma basis under

expected and stressful conditions throughout a planning horizon of at least nine quarters.

The January 1, 2010 adoption of the new consolidation accounting standards resulted in our consolidating a

substantial portion of our securitization trusts and establishing an allowance for loan and lease losses for the

assets underlying these trusts, which reduced retained earnings and our Tier 1 risk-based capital ratio. In January

2010, banking regulators issued regulatory capital rules related to the impact of the new consolidation accounting

standards. Under these rules, we are required to hold additional capital for the assets we consolidated. The capital

rules also provided for an optional phase-in of the impact from the adoption of the new consolidation accounting

standards, including a two-quarter implementation delay followed by a two-quarter partial implementation of the

effect on regulatory capital ratios.

We elected the phase-in option, which required us to phase-in 50% of consolidated assets beginning with the

third quarter of 2010 for purposes of determining risk-weighted assets. The phase-in provisions expired after

December 31, 2010, and we completed the final phase-in during the first quarter of 2011, which resulted in the

addition of approximately $15.5 billion of assets to the denominator used in calculating our regulatory ratios. The

addition of these assets negatively impacted our risk-based regulatory capital ratios as of December 31, 2011

from December 31, 2010.

Under the Dodd-Frank Act, many trust preferred securities will cease to qualify for Tier 1 capital, subject to a

three year phase-out period expected to begin in 2013.

Dividend Policy

The declaration and payment of dividends to our stockholders, as well as the amount thereof, are subject to the

discretion of our Board of Directors and will depend upon our results of operations, financial condition, capital

levels, cash requirements, future prospects and other factors deemed relevant by the Board of Directors. As a

bank holding company, our ability to pay dividends is largely dependent upon the receipt of dividends or other

payments from our subsidiaries. For additional information on dividends, see “Item 1. Business—Supervision

and Regulation—Dividends, Stock Purchases and Transfer of Funds.”

Regulatory restrictions exist that limit the ability of the Banks to transfer funds to our bank holding company.

Funds available for dividend payments from COBNA and CONA based on the Earnings Limitation Test were

88