Capital One 2011 Annual Report Download - page 116

Download and view the complete annual report

Please find page 116 of the 2011 Capital One annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

|

|

Strategic Risk Management

The Chief Executive Officer is responsible for our strategy. The Chief Executive Officer develops an overall

corporate strategy and leads alignment of the entire organization with this strategy through definition of strategic

imperatives and top-down communication. The Chief Executive Officer and other senior executives spend

significant time throughout the entire company sharing our strategic imperatives to promote an understanding of

our strategy and connect it to day-to-day associate activities to enable effective execution. Division Presidents are

accountable for defining business strategy within the context of the overall corporate level strategy and strategic

imperatives. Business strategies are integrated into the corporate strategic plan and are reviewed and approved

separately and together on an annual basis by the Chief Executive Officer and the Board of Directors.

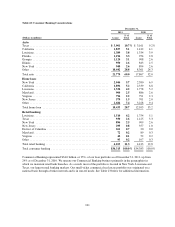

CREDIT RISK PROFILE

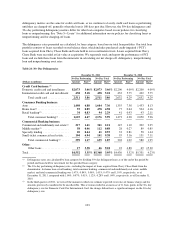

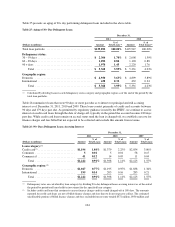

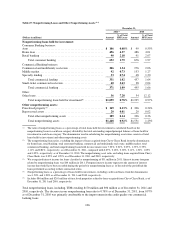

Our loan portfolio accounts for the substantial majority of our credit risk exposure. Below we provide

information about the composition of our loan portfolio, key concentrations and credit performance metrics.

We also engage in certain non-lending activities that may give rise to credit and counterparty settlement risk,

including the purchase of securities for our investment securities portfolio, entering into derivative transactions to

manage our market risk exposure and to accommodate customers, foreign exchange transactions and deposit

overdrafts. These activities are also governed under our credit policy and are subject to independent review and

approval. We provide additional information on credit risk related to our investment securities portfolio under

“Consolidated Balance Sheet Analysis—Investment Securities” and credit risk related to derivative transactions

in “Note 11—Derivative Instruments and Hedging Activities.”

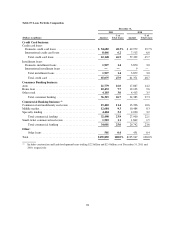

Loan Portfolio Composition

We provide a variety of lending products. Our primary products include credit cards, auto loans, home loans and

commercial loans.

•Credit cards: We market a range of credit card products across the credit spectrum and through a variety of

channels. Our credit cards generally have variable long-term interest rates. Credit card accounts are

underwritten using an automated underwriting system based on predictive models that we have developed.

The underwriting criteria, which are customized for individual products and marketing programs, are

established based on an analysis of the net present value of expected revenues, expenses and losses, subject

to a further analysis using a variety of stress conditions. Underwriting decisions are generally based on an

applicant’s income, estimated debt burden and credit bureau information. We maintain a credit card

securitization program and selectively sell charged-off credit card loans. However, subsequent to the

adoption of the consolidation accounting guidance on January 1, 2010, we retain all of our credit card loans

on our balance sheet.

•Auto loans: We market a range of auto loan products across the credit spectrum. Customers are acquired

through a network of auto dealers and direct marketing. Our auto loans generally have fixed interest rates

and loan terms of 72 months or less. Loan size limits are customized by program and subject to a current

maximum of $75,000. Similar to credit card accounts, the underwriting criteria are customized for

individual products and marketing programs and based on analysis of net present value of expected

revenues, expenses and losses, subject to maintaining resilience under a variety of stress conditions.

Underwriting decisions are generally based on an applicant’s income, estimated debt-to-income ratio, and

credit bureau information, along with collateral characteristics such as loan-to-value ratio. We generally

retain all of our auto loans, though we have securitized auto loans and sold charged-off auto loans in the past

and may do so in the future.

•Home loans: Most of the existing home loans in our loan portfolio were originated by banks we acquired.

The underwriting standards for these loans were less restrictive than our current underwriting standards.

96