Capital One 2011 Annual Report Download - page 88

Download and view the complete annual report

Please find page 88 of the 2011 Capital One annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

|

|

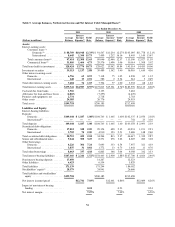

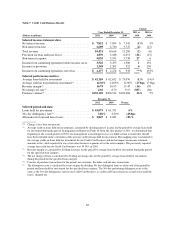

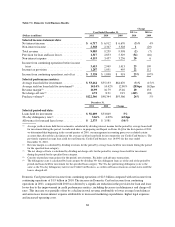

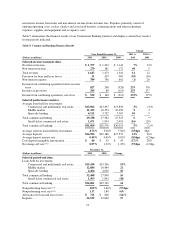

Table 7.1: Domestic Card Business Results

Change

Year Ended December 31, 2011 vs. 2010 vs.

(Dollars in millions) 2011 2010 2009 2010 2009

Selected income statement data:

Net interest income ......................... $ 6,717 $ 6,912 $ 6,670 (3)% 4%

Non-interest income ......................... 2,368 2,347 3,328 1(29)

Total revenue .............................. 9,085 9,259 9,998 (2) (7)

Provision for loan and lease losses .............. 1,317 2,853 5,329 (54) (46)

Non-interest expense ........................ 4,153 3,457 3,256 20 6

Income from continuing operations before income

taxes ................................... 3,615 2,949 1,413 23 109

Income tax provision ........................ 1,287 1,051 495 22 112

Income from continuing operations, net of tax .... $ 2,328 $ 1,898 $ 918 23% 107%

Selected performance metrics:

Average loans held for investment .............. $ 53,464 $55,133 $64,670 (3)% (15)%

Average yield on loans held for investment(1) ..... 14.14% 14.42% 12.80% (28)bps 162bps

Revenue margin(2) .......................... 16.99 16.79 15.46 20 133

Net charge-off rate(3) ........................ 4.72 8.91 9.19 (419) (28)

Purchase volume(4) .......................... $122,366 $98,344 $93,566 24% 5%

December 31,

2011 2010 Change

Selected period-end data:

Loans held for investment .................... $ 56,609 $53,849 5%

30+ day delinquency rate(5) ................... 3.66% 4.09% (43)bps

Allowance for loan and lease losses ............. $ 2,375 $ 3,581 (34)%

(1) Average yield on loans held for investment is calculated by dividing interest income for the period by average loans held

for investment during the period. As indicated above, in preparing our Report on Form 10-Q for the first quarter of 2011,

we determined that beginning in the second quarter of 2010, our management accounting processes excluded certain

accounts that affected the calculation of the average yield on loans held for investment for our Credit Card business. The

previously reported average loan yield for our Domestic Credit Card business was 14.09% for the year ended

December 31, 2010.

(2) Revenue margin is calculated by dividing revenues for the period by average loans held for investment during the period

for the specified loan category.

(3) The net charge-off rate is calculated by dividing net charge-offs for the period by average loans held for investment

during the period for the specified loan category.

(4) Consists of purchase transactions for the period, net of returns. Excludes cash advance transactions.

(5) The delinquency rate is calculated by loan category by dividing 30+ day delinquent loans as of the end of the period by

period-end loans held for investment for the specified loan category. The 30+ day performing delinquency rate is the

same as the 30+ day delinquency rate for our Credit Card business, as credit card loans remain on accrual status until the

loan is charged-off.

Domestic Card generated net income from continuing operations of $2.3 billion compared with net income from

continuing operations of $1.9 billion in 2010. The increase in Domestic Card net income from continuing

operations in 2011, compared with 2010 was driven by a significant reduction in the provision for loan and lease

losses due to the improvement in credit performance metrics, including decreases in delinquency and charge-off

rates. This increase was partially offset by a decline in total revenue attributable to lower average loan balances

and an increase in non-interest expense attributable to increased marketing expenditures, higher legal expenses

and increased operating costs.

68