Capital One 2011 Annual Report Download - page 122

Download and view the complete annual report

Please find page 122 of the 2011 Capital One annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

|

|

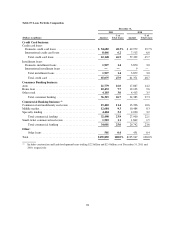

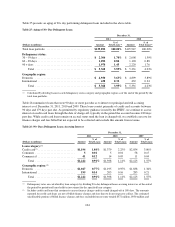

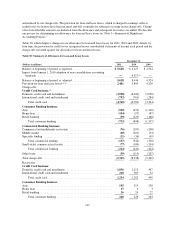

Table 23: Commercial Banking Concentrations

December 31,

2011 2010

(Dollars in millions) Loans

% of

Total Loans

% of

Total

Commercial lending:

New York ................................................... $13,213 38.9% $11,997 40.3%

Texas ....................................................... 4,246 12.5 2,990 10.1

Louisiana .................................................... 3,915 11.5 2,968 10.0

New Jersey .................................................. 2,031 6.0 2,149 7.2

Maryland .................................................... 921 2.7 646 2.2

Massachusetts ................................................ 911 2.7 800 2.7

District of Columbia ........................................... 763 2.2 389 1.3

Pennsylvania ................................................. 743 2.2 594 2.0

Virginia ..................................................... 730 2.1 534 1.8

California .................................................... 654 1.9 598 2.0

Other ....................................................... 4,371 12.9 4,235 14.2

Total commercial lending ....................................... 32,498 95.6 27,900 93.8

Small-ticket commercial real estate:

New York ................................................... 616 1.8 751 2.5

California .................................................... 329 1.0 402 1.4

Massachusetts ................................................ 117 0.3 146 0.5

New Jersey .................................................. 83 0.2 102 0.3

Florida ...................................................... 57 0.2 76 0.3

Other ....................................................... 301 0.9 365 1.2

Total small-ticket commercial real estate ........................... 1,503 4.4 1,842 6.2

Total commercial banking ....................................... $34,001 100.0% $29,742 100.0%

Credit Risk Measurement

We closely monitor economic conditions and loan performance trends to manage and evaluate our exposure to

credit risk. Trends in delinquency ratios are an indicator, among other considerations, of credit risk within our

loan portfolios. The level of nonperforming assets represents another indicator of the potential for future credit

losses. Accordingly, key metrics we track and use in evaluating the credit quality of our loan portfolio include

delinquency and nonperforming asset rates, as well as charge-off rates and our internal risk ratings of larger

balance, commercial loans. The improvements we have experienced in our credit trends across all of our

businesses are stabilizing and our credit performance is increasingly driven by seasonal trends. We present

information in the section below on the credit performance of our loan portfolio, including the key metrics we

use in tracking changes in the credit quality of our loan portfolio. See “Note 5—Loans” for additional details.

Delinquency Rates

We consider the entire balance of an account to be delinquent if the minimum required payment is not received

by the first statement cycle date equal to or following the due date specified on the customer’s billing statement.

Table 24 compares 30+ day performing loan delinquency rates, by loan category, as of December 31, 2011 and

2010. We also present total 30+ day delinquent loans.

Our 30+ day delinquency metrics include all held for investment loans that are 30 or more days past due, whereas

our 30+ day performing delinquency metrics include loans that are 30 or more days past due and that are also

currently classified as performing and accruing interest. The 30+ day delinquency and 30+ day performing

102