Capital One 2011 Annual Report Download - page 212

Download and view the complete annual report

Please find page 212 of the 2011 Capital One annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

202 -

203

203 -

204

204 -

205

205 -

206

206 -

207

207 -

208

208 -

209

209 -

210

210 -

211

211 -

212

212 -

213

213 -

214

214 -

215

215 -

216

216 -

217

217 -

218

218 -

219

219 -

220

220 -

221

221 -

222

222 -

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

|

|

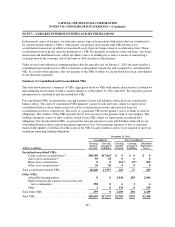

CAPITAL ONE FINANCIAL CORPORATION

NOTES TO CONSOLIDATED STATEMENTS—(Continued)

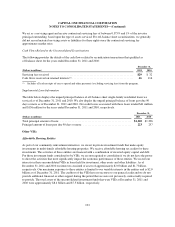

The changes in the fair value of retained interests are primarily driven by rate assumption changes and volume

fluctuations. All of these retained residual interests are subject to loss in the event assumptions used to determine

the estimated fair value do not prevail, or if borrowers default on the related securitized receivables and our

retained subordinated tranches are used to repay investors. See the table below for key assumptions and

sensitivities for retained interest valuations.

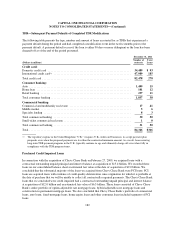

Key Assumptions and Sensitivities for Retained Interest Valuations

The key assumptions used in determining the fair value of the interest-only strip and other retained residual

interests include the weighted average ranges for principal payment rates, lives of receivables and discount rates,

all of which are included in the following table. The principal repayment rate assumptions were determined using

actual and forecast trust principal payment rates based on the collateral. The lives of receivables were determined

as the number of months necessary to repay the investors given the principal payment rate assumptions. The

discount rates were determined using primarily trust specific statistics and forward rate curves, and were

reflective of what market participants would use in a similar valuation. Additionally, accrued interest receivable,

cash reserve and spread accounts were discounted over the estimated life of the assets.

If these assumptions are not met, or if they change, the interest-only strip, retained interests and related servicing

and securitizations income would be affected. The following adverse changes to the key assumptions and

estimates are hypothetical and should be used with caution. As the figures indicate, any change in fair value

based on a 10% or 20% variation in assumptions cannot be extrapolated because the relationship of a change in

assumption to the change in fair value may not be linear. Also, the effect of a variation in a particular assumption

on the fair value of the interest-only strip is calculated independently from any change in another assumption.

However, changes in one factor may result in changes in other factors, which might magnify or counteract the

sensitivities.

For the periods ending December 31, 2011 and 2010, the assumptions and sensitivities shown below include all

off-balance sheet securitizations:

December 31,

(Dollars in millions) 2011 2010

Interest-only strip retained interests ..................................... $ 110(1) $ 136(1)

Weighted average life for receivables (months) ............................ 70 60

Principal repayment rate (weighted average rate) .......................... 12.2 - 17.1% 16.3 - 18.1%

Impact on fair value of 10% adverse change .............................. $ 15 $2

Impact on fair value of 20% adverse change .............................. (5) (6)

Discount rate (weighted average rate) ................................... 25.0 - 42.2% 25.2 - 42.2%

Impact on fair value of 10% adverse change .............................. $ (7) $ (7)

Impact on fair value of 20% adverse change .............................. (13) (14)

(1) Does not include liquidity swap related to the negative amortization bonds of $(16) million and $(19) million as of

December 31, 2011 and 2010, respectively.

Static pool credit losses were calculated by summing the actual and projected future credit losses and dividing

them by the original balance of each pool of assets. Due to the short-term revolving nature of the loan

receivables, the weighted average percentage of static pool credit losses was not considered materially different

from the assumed charge-off rates used to determine the fair value of the retained interests.

192