Capital One 2011 Annual Report Download - page 197

Download and view the complete annual report

Please find page 197 of the 2011 Capital One annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

187 -

188

188 -

189

189 -

190

190 -

191

191 -

192

192 -

193

193 -

194

194 -

195

195 -

196

196 -

197

197 -

198

198 -

199

199 -

200

200 -

201

201 -

202

202 -

203

203 -

204

204 -

205

205 -

206

206 -

207

207 -

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

|

|

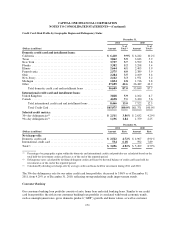

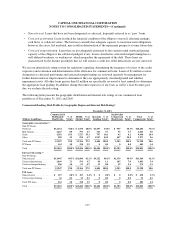

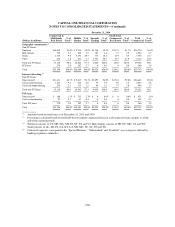

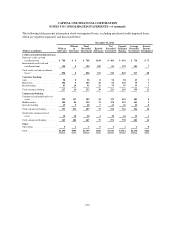

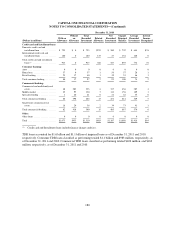

CAPITAL ONE FINANCIAL CORPORATION

NOTES TO CONSOLIDATED STATEMENTS—(Continued)

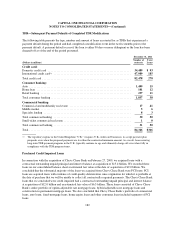

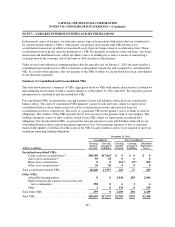

•Noncriticized: Loans that have not been designated as criticized, frequently referred to as “pass” loans.

•Criticized performing: Loans in which the financial condition of the obligor is stressed, affecting earnings,

cash flows or collateral values. The borrower currently has adequate capacity to meet near-term obligations;

however, the stress, left unabated, may result in deterioration of the repayment prospects at some future date.

•Criticized nonperforming: Loans that are not adequately protected by the current sound worth and paying

capacity of the obligor or the collateral pledged, if any. Loans classified as criticized nonperforming have a

well-defined weakness, or weaknesses, which jeopardize the repayment of the debt. These loans are

characterized by the distinct possibility that we will sustain a credit loss if the deficiencies are not corrected.

We use our internal risk-rating system for regulatory reporting, determining the frequency of review of the credit

exposures and evaluation and determination of the allowance for commercial loans. Loans of $1 million or more

designated as criticized performing and criticized nonperforming are reviewed quarterly by management for

further deterioration or improvement to determine if they are appropriately classified/graded and whether

impairment exists. All other loans greater than $1 million are specifically reviewed at least annually to determine

the appropriate loan grading. In addition, during the renewal process of any loan, as well if a loan becomes past

due, we evaluate the risk rating.

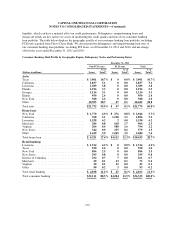

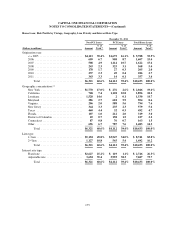

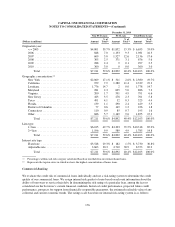

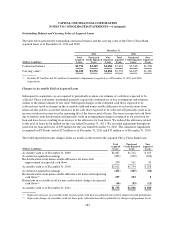

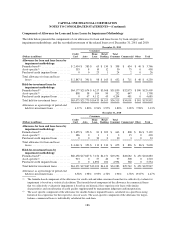

The following table presents the geographic distribution and internal risk ratings of our commercial loan

portfolio as of December 31, 2011 and 2010.

Commercial Banking: Risk Profile by Geographic Region and Internal Risk Rating(1)

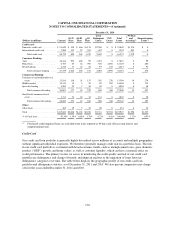

December 31, 2011

(Dollars in millions)

Commercial &

Multifamily

Real Estate

% of

Total(2)

Middle

Market

% of

Total(2)

Specialty

Lending

% of

Total(2)

Small-ticket

Commercial

Real Estate

% of

Total(2)

Total

Commercial

% of

Total(2)

Geographic concentration:(3)

Non-PCI loans:

Northeast ................ $12,152 78.8% $ 3,650 28.8% $1,497 34.0% $ 907 60.3% $18,206 53.6%

Mid-Atlantic .............. 1,225 8.0 599 4.7 163 3.7 56 3.7 2,043 6.0

South ................... 1,581 10.3 7,527 59.3 797 18.1 93 6.2 9,998 29.4

Other ................... 289 1.9 590 4.7 1,947 44.2 447 29.8 3,273 9.6

Total non-PCI loans ........ 15,247 99.0 12,366 97.5 4,404 100.0 1,503 100.0 33,520 98.6

PCI loans ................ 163 1.0 318 2.5 0 0.0 0 0.0 481 1.4

Total .................... $15,410 100.0% $12,684 100.0% $4,404 100.0% $1,503 100.0% $34,001 100.0%

Internal risk rating:(4)

Non-PCI loans:

Noncriticized ............. $13,945 90.5% $11,680 92.1% $4,322 98.1% $1,359 90.4% $31,306 92.1%

Criticized performing ....... 1,096 7.1 593 4.7 49 1.1 105 7.0 1,843 5.4

Criticized nonperforming .... 206 1.4 93 0.7 33 0.8 39 2.6 371 1.1

Total non-PCI loans ........ 15,247 99.0 12,366 97.5 4,404 100.0 1,503 100.0 33,520 98.6

PCI loans:

Noncriticized ............. $ 127 0.8% $ 303 2.4% $ 0 0.0% $ 0 0.0% $ 430 1.3%

Criticized performing ....... 36 0.2 15 0.1 0 0.0 0 0.0 51 0.1

Total PCI loans ........... 163 1.0 318 2.5 0 0.0 0 0.0 481 1.4

Total .................... $15,410 100.0% $12,684 100.0% $4,404 100.0% $1,503 100.0% $34,001 100.0%

177