Capital One 2011 Annual Report Download - page 69

Download and view the complete annual report

Please find page 69 of the 2011 Capital One annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

|

|

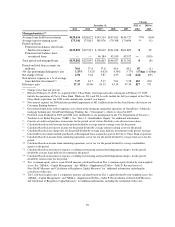

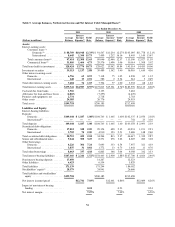

began to decrease and we recorded significant allowance releases of $1.4 billion in 2011 and $2.8 billion in 2010.

We provide additional information on the methodologies and key assumptions used in determining our allowance

for loan and lease losses for each of our loan portfolio segments in “Note 1—Summary of Significant Accounting

Policies.” We provide information on the components of our allowance, disaggregated by impairment

methodology, and changes in our allowance in “Note 6—Allowance for Loan and Lease Losses.”

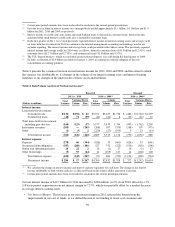

Finance Charge and Fee Reserve

We recognize finance charges and fees on credit card loans as revenue when the amounts are billed to the

customer and include these amounts in the loan balance, net of the estimated uncollectible amount of finance

charges and fees. We continue to accrue finance charges and fees on credit card loans until the account is

charged-off; however, when we do not expect full payment of billed finance charges and fees, we reduce the

balance of our credit card loan receivables by the amount of finance charges billed but not expected to be

collected and exclude this amount from revenue. Revenue was reduced by $371 million, $950 million and $2.1

billion in 2011, 2010 and 2009, respectively, for the estimated uncollectible amount of billed finance charges and

fees. The finance charge and fee reserve totaled $74 million as of December 31, 2011, compared with $211

million as of December 31, 2010.

Our methodology for estimating the uncollectible portion of billed finance charges and fees is consistent with the

methodology we use to estimate the allowance for incurred principal losses on our credit card loan receivables.

Accordingly, the estimation process is subject to similar risks and uncertainties, including a reliance on historical

loss and trend information that may not be representative of current conditions and indicative of future

performance. Changes in key assumptions may have a material impact on the amount of billed finance charges

and fees we estimate as uncollectible in each period.

We determine the adequacy of the uncollectible finance charge and fee reserve on a quarterly basis, primarily

based on the use of a roll-rate methodology. We refine our estimation process and key assumptions used in

determining our loss reserves as additional information becomes available. In the third quarter of 2011, we

revised the manner in which we estimate expected recoveries of finance charge and fee amounts previously

considered to be uncollectible. Our revised recovery assumptions better reflect the post-recession pattern of

relatively low delinquency roll-rates combined with increased recoveries of finance charges and fees previously

considered uncollectible. This change in assumptions resulted in reduction in our uncollectible finance charge

and fee reserves of approximately $83 million as of September 30, 2011, and in a corresponding increase in

revenues. We also applied these revised assumptions to the estimated recovery of principal charge-offs in

determining our allowance for loan and lease losses. The revision, however, had an insignificant impact on the

overall determination of our allowance for lease and loan losses.

Representation and Warranty Reserve

In connection with their sales of mortgage loans, certain subsidiaries entered into agreements containing varying

representations and warranties about, among other things, the ownership of the loan, the validity of the lien

securing the loan, the loan’s compliance with any applicable loan criteria established by the purchaser, including

underwriting guidelines and the ongoing existence of mortgage insurance, and the loan’s compliance with

applicable federal, state and local laws. We may be required to repurchase the mortgage loan, indemnify the

investor or insurer, or reimburse the investor for credit losses incurred on the loan in the event of a material

breach of contractual representations or warranties.

We have established representation and warranty reserves for losses that we consider to be both probable and

reasonably estimable associated with the mortgage loans sold by each subsidiary, including both litigation and

non-litigation liabilities. The reserve-setting process relies heavily on estimates, which are inherently uncertain,

and requires the application of judgment. In establishing the representation and warranty reserves, we consider a

variety of factors, depending on the category of purchaser and rely on historical data. We evaluate these

estimates on a quarterly basis.

49