Capital One 2011 Annual Report Download - page 86

Download and view the complete annual report

Please find page 86 of the 2011 Capital One annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

|

|

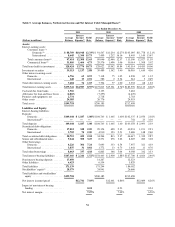

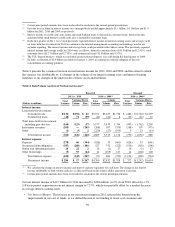

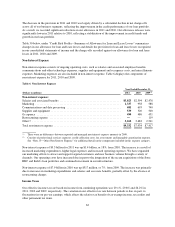

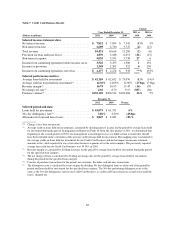

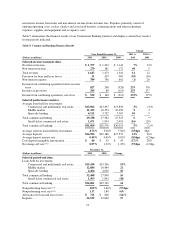

Key factors affecting the results of our Credit Card business for 2011, compared with 2010 included the

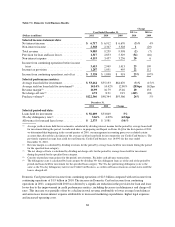

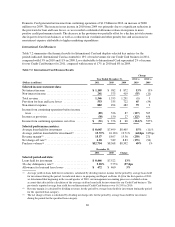

following:

•Net Interest Income: Net interest income decreased by $72 million, or 1%, in 2011, reflecting the impact of

a 1% decline in average loan balances. The expected run-off of the installment loan portfolio was the

primary driver of the decline in average loan balances in 2011, more than offsetting the additions of the

HBC and Kohl’s portfolios.

•Non-Interest Income: Non-interest income decreased by $111 million, or 4%, in 2011. The decrease reflects

the impact of contra-revenue amounts recorded in the second quarter and fourth quarters of 2011, including

a provision of $102 million for anticipated refunds to U.K. customers related to retrospective regulatory

requirements pertaining to payment protection insurance (“PPI”) in our U.K. business and the recognition of

expenses related to the periodic adjustment of our customer rewards points liability to reflect the estimated

cost of points earned to date that are ultimately expected to be redeemed. These decreases were partially

offset by higher net interchange fees during 2011, attributable to increased purchase volume.

•Provision for Loan and Lease Losses: The provision for loan and lease losses related to our Credit Card

business decreased by $1.3 billion in 2011, to $1.9 billion. The significant reduction in the provision was

primarily attributable to the continued improvement in credit performance, including reduced delinquency

rates and lower bankruptcy losses. As a result of the reduction in charge-offs and improvement in the net

charge-off rate, we recorded an allowance release for the Credit Card business of $1.2 billion in 2011

compared to $2.3 billion in 2010.

•Non-Interest Expense: Non-interest expense increased by $1.1 billion, or 27%, in 2011. The increase in

non-interest expense was attributable to increased marketing expenditures, higher legal expenses, and

increased operating cost. Additionally, we recorded $40 million in relation to regulatory requirements

pertaining to PPI in our U.K. business. We have expanded our marketing efforts to drive new business

volume through a variety of channels.

•Total Loans: Period-end loans in our Credit Card business increased by $3.7 billion, or 6%, in 2011, to

$65.1 billion as of December 31, 2011, from $61.4 billion as of December 31, 2010. The increase was

primarily attributable to the acquisitions of the Kohl’s credit card portfolio of $3.7 billion and the HBC

credit card portfolio of $1.4 billion, which were partially offset by the continued run-off of the installment

loan portfolio.

•Charge-off and Delinquency Statistics: Net charge-off and delinquency rates continued to improve in 2011.

The net charge-off rate decreased to 4.92% in 2011 from 8.79% in 2010. The 30+ day delinquency rate

decreased to 3.86% as of December 31, 2011, from 4.29% as of December 31, 2010. The improvement in

the net charge-off and delinquency rates reflects the impact of improved credit quality across our credit card

portfolio, tighter underwriting standards implemented over the last several years, and ongoing normalization

of credit performance in the portfolio.

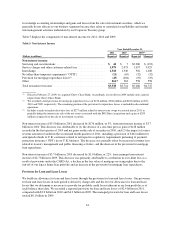

Key factors affecting the results of our Credit Card business for 2010, compared with 2009 included the

following:

•Net Interest Income: Our Credit Card business experienced an increase in net interest income of $352

million, or 5%, in 2010, which was primarily attributable to higher asset yields that more than offset a

decline in average loans held for investment. The increase in the average yield on our credit card loan

portfolio reflected the benefit of pricing changes that were implemented during 2009 and a reduction in the

level of loans with low introductory promotional rates. Net interest income also reflected the benefit of the

recognition into income of an increased amount of previously suppressed billed finance charges and fees as

a result of improving credit trends.

•Non-Interest Income: Non-interest income decreased by $1.0 billion, or 27%, in 2010. The decrease was

primarily attributable to a reduction in penalty fees resulting from the implementation of provisions of the

CARD Act and a reduction in customer accounts.

66