Capital One 2011 Annual Report Download

Download and view the complete annual report

Please find the complete 2011 Capital One annual report below. You can navigate through the pages in the report by either clicking on the pages

listed below, or by using the keyword search tool below to find specific information within the annual report.

-

1

-

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

Table of contents

-

Page 1

-

Page 2

-

Page 3

... The purchase of ING Direct makes us the leader in direct banking in the United States, and the acquisition of the U.S. credit card business of HSBC will signiï¬cantly expand our card franchise. For more than 20 years, we have worked to build an enduringly great franchise in ï¬nancial services. We...

-

Page 4

..., investment, and retirement products that extend the winning ING Direct customer experience beyond savings and direct banking. HSBC's U.S. credit card business will be an excellent complement to ING Direct. Where ING Direct signiï¬cantly expands our deposits, we expect the HSBC acquisition to...

-

Page 5

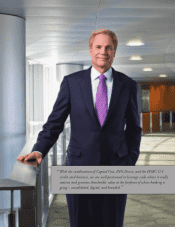

" With the combination of Capital One, ING Direct, and the HSBC U.S.

credit card business, we are well positioned to leverage scale where it really matters and generate shareholder value at the forefront of where banking is going - consolidated, digital, and branded."

3

-

Page 6

... delivered these returns with a charge-off rate of 4.7% which was below the industry average. The strong performance of our credit card business through good times and bad is clear evidence of the power of Capital One's information-based strategy. We have increasing momentum in credit cards, and the...

-

Page 7

... 20 senior retail banking executives, all highly talented and with successful track records. We believe we are now well on our way toward becoming a great sales and service organization. Capital One Auto Finance had an outstanding year, with strong proï¬tability and returns. Losses have risen...

-

Page 8

... to become one of the few enduring, high-quality franchises in auto ï¬nance.

From nearly 1,000 branches in carefully selected local markets, we're serving customers in New York, New Jersey, Connecticut, Delaware, Virginia, the District of Columbia, Maryland, Louisiana, and Texas.

In Home Loans, we...

-

Page 9

..., real-time opportunity for us to engage our customers and get anecdotal feedback that we can use to quickly ï¬ne-tune our products and services. Fortune® magazine named Capital One to its list of "Nine Social Media Stars" in 2011.

Capital One is the Ofï¬cial Bank and Credit Card of the

Capital...

-

Page 10

... we're best equipped to address: affordable housing, ï¬nancial literacy, education, small business development, and workforce training.

Over the past six years, Capital One/Junior Achievement Finance Park has helped teach more than 100,000 students, supported by over 9,000 Capital One volunteers in...

-

Page 11

...We have worked for years to get here

Since our founding days, we have worked to build the "bone structure" to be enduringly successful in an industry with powerful scale economies and transformational change. With the combination of Capital One, ING Direct, and the HSBC U.S. credit card business, we...

-

Page 12

... interest rates and a ï¬,at yield curve. Regulatory scrutiny of banking continues to increase, and we expect higher capital requirements and higher compliance and risk-management costs. And we must do an efï¬cient, effective job of integrating our latest acquisitions. As we execute our integrations...

-

Page 13

...55

$6.68

$7.03

$2.28* $0.98 2007 2008 2009 2010 2011

Diluted Earnings Per Share

$6.01 $3.97

$6.80

($0.21) 2007 2008

$0.74 2009 2010 2011

Deposits ($ In Billions)

$109 $83

$116

$122

$128

2007

2008

2009

2010

2011

* 2008 data excludes goodwill impairment charge of $811 million.

11

-

Page 14

... Total assets Interest-bearing deposits Total deposits Borrowings Stockholders' equity $ $

Credit Quality Metrics:

Allowance for loan and lease losses Allowance as a % of loans held for investment Net charge-offs Net charge-off rate 30+ day performing delinquency rate 30+ day total delinquency rate...

-

Page 15

...and Direct Banking

Mayo A. Shattuck, III C, F

Executive Chairman Exelon Corporation

Sanjiv Yajnik

President, Financial Services

Bradford H. Warner A, F

Former Head of Premier and Small Business Banking Bank of America Corporation

A C

Audit and Risk Committee Compensation Committee F Finance and...

-

Page 16

14

-

Page 17

... Capital One Drive, McLean, Virginia

(Address of Principal Executive Offices)

22102

(Zip Code)

Registrant's telephone number, including area code: (703) 720-1000 Securities registered pursuant to section 12(b) of the act:

Title of Each Class Name of Each Exchange on Which Registered

Common Stock...

-

Page 18

... ...Business Segment Financial Performance ...Consolidated Balance Sheet Analysis ...Off-Balance Sheet Arrangements and Variable Interest Entities ...Capital Management ...Risk Management ...Credit Risk Profile ...Liquidity Risk Profile ...Market Risk Profile ...Accounting Changes and Developments...

-

Page 19

...-Deposits and Borrowings ...Note 11-Derivative Instruments and Hedging Activities ...Note 12-Stockholders' Equity ...Note 13-Regulatory and Capital Adequacy ...Note 14-Earnings Per Common Share ...Note 15-Other Non-Interest Expense ...Note 16-Stock-Based Compensation Plan ...Note 17-Employee Benefit...

-

Page 20

... Unsecured Debt Credit Ratings ...Interest Rate Sensitivity Analysis ...Supplemental Tables: Loan Portfolio Composition ...Performing Delinquencies ...Nonperforming Assets ...Net Charge-Offs ...Summary of Allowance for Loan And Lease Losses ...Reconciliation of Non-GAAP Measures and Calculation...

-

Page 21

... ("Chevy Chase Bank"), strengthening the Capital One brand in the Washington, D.C. region. In addition to bank lending, treasury management and depository services, we offer credit and debit card products, auto loans and mortgage banking in markets across the United States. As of December 31, 2011...

-

Page 22

... lines of businesses. We may issue equity or debt in connection with acquisitions, including public offerings, to fund such acquisitions. Recent completed or pending acquisitions are discussed below. Hudson's Bay Company-Credit Card Portfolio On January 7, 2011, we acquired the existing credit card...

-

Page 23

... consumer home loan lending and servicing activities. Commercial Banking: Consists of our lending, deposit gathering and treasury management services to commercial real estate and middle market customers. Our middle market customers typically include commercial and industrial companies with annual...

-

Page 24

...bank holding companies. The Banks are national associations chartered under the laws of the United States, the deposits of which are insured by the Deposit Insurance Fund (the "DIF") of the Federal Deposit Insurance Corporation (the "FDIC") up to applicable limits. ING Bank is a federal savings bank...

-

Page 25

...-existing balances of a customer whose risk of default increases are restricted. Payments above the minimum payment must be allocated first to balances with the highest interest rate. The amount of fees charged to credit card accounts with lower credit lines is limited. A consumer's ability to pay...

-

Page 26

... rules is to ensure that large bank holding companies have robust, forward-looking capital planning processes that account for their unique risks and capital needs to continue operations through times of economic and financial stress. As part of its evaluation of a capital plan, the Federal Reserve...

-

Page 27

... Rule"). It is also possible that CONA will be designated as a "swap dealer" under the Dodd-Frank Act due to its derivative activities associated with commercial lending, which would result in oversight by the Commodity Futures Trading Commission and more requirements for our current and future...

-

Page 28

... recent insurance losses and future loss projections, which resulted in several rules that generally increased deposit insurance rates and purported to improve risk differentiation so that riskier institutions bear a greater share of insurance premiums. The Dodd-Frank Act reformed the management of...

-

Page 29

... finalized rules to implement this change that significantly modified how deposit insurance assessment rates are calculated for those banks with assets of $10 billion or greater. Banks may accept brokered deposits as part of their funding. Under the Federal Deposit Insurance Corporation Improvement...

-

Page 30

... any one or more of these requirements could subject us to enforcement action or litigation. Like other financial institutions, the Banks and ING Bank rely upon consumer reports for prescreen marketing, underwriting new loans and for reviewing and managing risks associated with existing accounts. In...

-

Page 31

..., or making any public offer to acquire, control of a Virginia financial institution or its holding company without making application to, and receiving prior approval from, the Virginia Bureau of Financial Institutions. Because ING Bank is a federal savings bank located in Delaware, acquisitions of...

-

Page 32

...") under the Payment Services Regulations 2009. COEP is a member of the Lending Code, which sets standards of good lending practice in relation to loans, credit cards and current account overdrafts. COEP is not a retail deposit-taker. COEP's indirect parent, Capital One Global Corporation, is wholly...

-

Page 33

... launched a market investigation into the supply of Payment Protection Insurance ("PPI") in the United Kingdom. The scope included PPI on mortgages, credit cards, unsecured loans (personal loans, motor loans and hire purchase) and secured loans. In October 2010, the CC published its final report on...

-

Page 34

... of price, credit limit and other product features, and customer loyalty is often limited. Our Consumer Banking and Commercial Banking businesses compete with national and state banks and direct banks for deposits, auto loans, mortgages and trust accounts and with savings and loan associations and...

-

Page 35

... to): Total System Services Inc. ("TSYS") for processing services for our North American and United Kingdom portfolios of consumer and small business credit card accounts, Fidelity National Information Services ("Fidelity") for the Capital One banking systems and IBM Corporation for management of...

-

Page 36

... per share or other financial measures for us; future financial and operating results; our plans, objectives, expectations and intentions; the projected impact and benefits of the acquisition of ING Direct (the "ING Direct Transaction") and the pending acquisition of HSBC's U.S. credit card business...

-

Page 37

... as our business develops or changes or as it expands into new market areas; our ability to execute on our strategic and operational plans; any significant disruption of, or loss of public confidence in, the United States Mail service affecting our response rates and consumer payments; our ability...

-

Page 38

...condition and results of operations as customers default on their loans or maintain lower deposit levels or, in the case of credit card accounts, carry lower balances and reduce credit card purchase activity. In particular, we may face the following risks in connection with these events: • Adverse...

-

Page 39

... in the capital markets or other events, including actions by rating agencies and deteriorating investor expectations, which could limit our access to funding. The interest rates that we pay on our securities are also influenced by, among other things, applicable credit ratings from recognized...

-

Page 40

... increasing our cost of funding, our cost of capital or our cost of complying with applicable laws and regulations.

•

•

The Credit CARD Act (amending the Truth-in-Lending Act) and related changes to Regulation Z impose a number of restrictions on credit card practices impacting rates and fees...

-

Page 41

... under which a card issuer can raise the interest rate on pre-existing balances of a customer whose risk of default increases are restricted. As a result, the rules implementing the Credit CARD Act could make the card business generally less resilient in future economic downturns. Under the...

-

Page 42

... balance from our customers. Particularly with respect to our commercial lending and home loan activities, decreases in real estate values adversely affect the value of property used as collateral for our loans and investments. Thus, the recovery of such property could be insufficient to compensate...

-

Page 43

... rules is to ensure that large bank holding companies have robust, forward-looking capital planning processes that account for their unique risks and capital needs to continue operations through times of economic and financial stress. As part of its evaluation of a capital plan, the Federal Reserve...

-

Page 44

...our Retail Banking and Commercial Banking businesses. We anticipate making additional infrastructure changes and upgrades in connection with the integration of ING Direct and the pending acquisition of HSBC's U.S. credit card business. Our pending acquisition of the HSBC U.S. credit card business in...

-

Page 45

... ING Direct and HSBC's U.S. credit card business and establish scalable operations, may increase our expenses. Further, as our business develops, changes or expands, additional expenses can arise as a result of a reevaluation of business strategies, management of outsourced services, asset purchases...

-

Page 46

... HSBC's U.S. credit card business in August 2011. In addition, we entered into credit card partnership agreements with, Kohl's Corp., Sony Corporation and Hudson's Bay Company during the past two years, including the acquisition of the related credit card loan portfolios, and we acquired Chevy Chase...

-

Page 47

... face the following risks in connection with any merger, acquisition or strategic partnership, including the ING Direct acquisition and the pending acquisition of HSBC's U.S. credit card businesses: • New Businesses and Geographic or Other Markets. Our merger, acquisition or strategic partnership...

-

Page 48

... unemployment rate, housing prices, the interest rate environment, the shape of the yield curve, inflation and other economic indicators; and other financial and strategic risks associated with any merger or acquisition.

- - -

-

•

Target Specific Risk. Assets and companies that we acquire will...

-

Page 49

...in borrowing activity, including credit card use, payment patterns and the rate of defaults by accountholders and borrowers domestically and internationally. These social factors include changes in consumer confidence levels, the public's perception regarding consumer debt, including credit card use...

-

Page 50

... rate movement and the performance of the capital markets. Changes in interest rates or in valuations in the debt or equity markets could directly impact us. For example, we borrow money from other institutions and depositors, which we use to make loans to customers and invest in debt securities...

-

Page 51

... are interrelated as a result of trading, clearing, servicing, counterparty and other relationships. With our recent acquisition of ING Direct and our pending acquisition of HSBC's U.S. credit card businesses, we have exposure to increasing numbers of financial institutions and counterparties. These...

-

Page 52

..., New Jersey, Maryland, New York, Texas and Virginia for office and branch operations. Our corporate real estate portfolio also includes leased or owned space totaling, in the aggregate, 3.4 million square feet in Richmond, Toronto, Melville, New York City and various other locations. Item 3. Legal...

-

Page 53

... of Equity Securities Market Information Our common stock is listed on the NYSE and is traded under the symbol "COF." As of January 31, 2012, there were 15,242 holders of record of our common stock. The table below presents the high and low closing sales prices of our common stock as reported by...

-

Page 54

... any sales of unregistered equity securities in 2011. On June 16, 2011, we entered into a purchase and sale agreement with the ING Sellers to acquire ING Direct. On February 17, 2012, in connection with the closing of the acquisition, we issued 54,028,086 shares of common stock to ING Bank N.V. as...

-

Page 55

... related to repurchases of shares of our common stock during the fourth quarter of 2011.

Total Number of Shares Purchased(1) Total Number of Shares Purchased as Part of Publicly Announced Plans Maximum Amount That May Yet be Purchased Under the Plan or Program

Average Price Paid per Share...

-

Page 56

...in our income statement, net income on a managed basis was the same as reported net income. Effective January 1, 2010, we prospectively adopted two new accounting standards related to the transfer and servicing of financial assets and consolidations that changed how we account for our securitization...

-

Page 57

...Common dividend payout ratio ...2.92% 3.32% 66.80% 722.06% 2.68% (40)bps 6,348bps Stock price per common share at period end ...$ 42.29 $ 42.56 $ 38.34 $ 31.89 $ 47.26 (1)% 11% Book value per common share at period end ...64.51 58.62 59.04 68.38 65.18 10 (1) Total market capitalization at period end...

-

Page 58

2011

Year Ended December 31, 2010 2009(1) 2008

2007

Change 2011 vs. 2010 vs. 2010 2009

Average balances Loans held for investment ...Interest-earning assets ...Total assets ...Interest-bearing deposits ...Total deposits ...Borrowings ...Stockholders' equity ...

$128,424 $128,526 $ 99,787 $ 98,...

-

Page 59

... assets for the period. Calculated based on net charge-offs for the period divided by average loans held for investment for the period. Average loans held for investment include purchased credit-impaired loans acquired as part of the Chevy Chase Bank acquisition Calculated based on income from...

-

Page 60

...16)

(17)

Total risk-based capital ratio is a regulatory measure calculated based on total risk-based capital divided by risk-weighted assets. See "MD&A-Capital Management" and "MD&A-Supplemental Tables-Table F: Reconciliation of Non-GAAP Measures and Calculation of Regulatory Capital Measures" for...

-

Page 61

... consumer home loan lending and servicing activities. Commercial Banking: Consists of our lending, deposit gathering and treasury management services to commercial real estate and middle market customers. Our middle market customers typically include commercial and industrial companies with annual...

-

Page 62

...Income Total Net Income Revenue(1) (Loss)(2) Revenue(1) (Loss)(2) Revenue(1) (Loss)(2) % of % of % of % of % of % of Amount Total Amount Total Amount Total Amount Total Amount Total Amount Total 2011

(Dollars in millions)

Credit Card ...$10,431 Consumer Banking ...4,956 Commercial Banking ...1,647...

-

Page 63

... and HSBC acquisitions below. We took several actions during the year to manage the anticipated impact of the ING Direct acquisition on our market risk exposure and regulatory capital requirements. From the date we entered into the agreement to acquire ING Direct to early August 2011, interest rates...

-

Page 64

... Total Loans: Period-end loans held for investment increased by $10.0 billion, or 8%, in 2011, to $135.9 billion as of December 31, 2011, from $125.9 billion as of December 31, 2010. The increase was primarily attributable to growth in our Credit Card, Commercial Banking, and Auto Finance businesses...

-

Page 65

the credit card loan portfolios of Sony, HBC and Kohl's and increased marketing expenditures. New account originations have continued to grow in our Credit Card business, due in part to these acquisitions. • Consumer Banking: Our Consumer Banking business generated net income from continuing ...

-

Page 66

... current expectations regarding our total company performance and the performance of each of our business segments over the near-term based on market conditions, the regulatory environment and our business strategies as of the time we filed this Annual Report on Form 10-K. The statements contained...

-

Page 67

... will increase significantly as a result of integration and direct operating costs associated with the acquisition of ING Direct and the pending acquisition of HSBC's U.S. credit card business. We believe our marketing investments in 2011 were in equilibrium with current market opportunities. We...

-

Page 68

... limited to, historical loss and recovery experience, recent trends in delinquencies and charge-offs, risk ratings, the impact of bankruptcy filings, the value of collateral underlying secured loans, account seasoning, changes in our credit evaluation, underwriting and collection management policies...

-

Page 69

... losses on our credit card loan receivables. Accordingly, the estimation process is subject to similar risks and uncertainties, including a reliance on historical loss and trend information that may not be representative of current conditions and indicative of future performance. Changes in key...

-

Page 70

... belongs; the payment structure of the security; external credit ratings; the value of underlying collateral and current market conditions. Quantitative criteria include assessing whether there has been an adverse change in expected future cash flows. For equity securities, our evaluation criteria...

-

Page 71

... test for 2011, we determined the fair value of our reporting units using a discounted cash flow analysis, a form of the income approach. Our discounted cash flow analysis required management to make judgments about future loan and deposit growth, revenue growth, credit losses, and capital rates. We...

-

Page 72

..., such as reduced liquidity in the capital markets or changes in secondary market activities, may reduce the availability and reliability of quoted prices or observable data used to determine fair value. We have developed policies and procedures to determine when markets for our financial assets and...

-

Page 73

... from business areas, our Enterprise Risk Oversight division and our Finance division. Our Valuations Group performs monthly independent verification of fair value measurements by comparing the methodology driven price to other market source data (to the extent available), and uses independent...

-

Page 74

... to January 1, 2010 as a result of our adoption of the new consolidation accounting standards. Our reported results subsequent to January 1, 2010 are more comparable to our managed results because we assumed for our managed based reporting that our securitized loans had not been sold and that the...

-

Page 75

... from loans in our off-balance sheet securitization trusts or the interest expense on third-party debt issued by these securitization trusts. Beginning January 1, 2010, servicing fees, finance charges, other fees, net charge-offs and interest paid to third party investors related to consolidated...

-

Page 76

...32 Total consumer loans(4) ...Commercial loans(4) ...Total loans held for investment ...Investment securities ...Other interest-earning assets: Domestic ...International ...Total other interest earning assets ...Cash and due from banks ...Allowance for loan and lease losses ...Premises and equipment...

-

Page 77

... from small business credit cards also is included in consumer loans. In the first quarter of 2011, we revised previously reported interest income on interest-earning assets and average yield on loans held for investment for 2010 to conform to the internal management accounting methodology used in...

-

Page 78

...405 1,149 13.67 Total consumer loans(4) ...Commercial loans(4) ...Investment securities ...Other interest-earning assets: Domestic ...International ...Total other interest earning assets ...Cash and due from banks ...Allowance for loan and lease losses ...Premises and equipment, net ...Other assets...

-

Page 79

... from small business credit cards also is included in consumer loans. In the first quarter of 2011, we revised previously reported interest income on interest-earning assets and average yield on loans held for investment for 2010 to conform to the internal management accounting methodology used in...

-

Page 80

...recognize a gain or loss or record retained interests when we transfer loans into securitization trusts. The servicing fees, finance charges, other fees, net of charge-offs and interest paid to third party investors related to our consolidated securitization trusts are now reported as a component of...

-

Page 81

... a mark-to-market derivative loss of $277 million related to interest-rate swaps we entered into in 2011 to partially hedge the interest rate risk of the net assets associated with the ING Direct acquisition and a gain of $259 million recognized on the sale of investment securities.

Non-interest...

-

Page 82

...consolidated statements of income and the charge-offs recorded against our allowance for loan and lease losses in 2011, 2010 and 2009. Non-Interest Expense Non-interest expense consists of ongoing operating costs, such as salaries and associated employee benefits, communications and other technology...

-

Page 83

...products and services provided, or the type of customer served: Credit Card, Consumer Banking and Commercial Banking. The operations of acquired businesses have been integrated into our existing business segments. Certain activities that are not part of a segment, such as management of our corporate...

-

Page 84

...results related to the HBC loan portfolio, which totaled approximately $1.4 billion at acquisition on January 7, 2011, are included in our International Card business. Under the terms of the partnership agreement with Kohl's, we share a fixed percentage of revenues, consisting of finance charges and...

-

Page 85

Table 7: Credit Card Business Results

Change 2011 vs. 2010 vs. 2010 2009

(Dollars in millions)

Year Ended December 31, 2011 2010 2009

Selected income statement data: Net interest income ...$ Non-interest income ...Total revenue ...Provision for loan and lease losses ...Non-interest expense ......

-

Page 86

..., we recorded $40 million in relation to regulatory requirements pertaining to PPI in our U.K. business. We have expanded our marketing efforts to drive new business volume through a variety of channels. Total Loans: Period-end loans in our Credit Card business increased by $3.7 billion, or 6%, in...

-

Page 87

... customer accounts and targeted cost savings across our Credit Card business. As the economy gradually improved, we increased our marketing expenditures during 2010 from suppressed levels in 2009 to attract and support new business volume through a variety of channels. Total Loans: Period-end loans...

-

Page 88

Table 7.1: Domestic Card Business Results

Change 2011 vs. 2010 vs. 2010 2009

(Dollars in millions)

Year Ended December 31, 2011 2010 2009

Selected income statement data: Net interest income ...Non-interest income ...Total revenue ...Provision for loan and lease losses ...Non-interest expense ......

-

Page 89

...in 2009.

Table 7.2: International Card Business Results

Change 2011 vs. 2010 vs. 2010 2009

Year Ended December 31, (Dollars in millions) 2011 2010 2009

Selected income statement data: Net interest income ...Non-interest income ...Total revenue ...Provision for loan and lease losses ...Non-interest...

-

Page 90

...30+ day performing delinquency rate is the same as the 30+ day delinquency rate for our Credit Card business, as credit card loans remain on accrual status until the loan is charged-off.

Our International Card business generated a net loss from continuing operations of $51 million in 2011, compared...

-

Page 91

...689

(2)

Average loans held for investment used in the denominator in calculating net charge-off, delinquency and nonperforming loan and nonperforming asset rates includes the impact of loans acquired as part of the Chevy Chase Bank acquisition, which were considered purchased credit-impaired ("PCI...

-

Page 92

...our auto loan portfolio and an increase in the allowance for home equity loans we acquired from Chevy Chase Bank. Non-Interest Expense: Non-interest expense increased by $294 million, or 10%, in 2011. The increase was largely attributable to the recognition of expense for contingent payments related...

-

Page 93

... credit performance trends and the higher credit quality of our more recent auto loan vintages, as well as current favorable benefits from elevated auction prices. Our home loan credit performance remained stable during 2011.

Key factors affecting the results of our Consumer Banking business...

-

Page 94

... lending ...Total commercial lending ...Small-ticket commercial real estate ...Total commercial banking ...Average yield on loans held for investment ...Average deposits ...Average deposit interest rate ...Core deposit intangible amortization ...Net charge-off rate(1)(2) ...(Dollars in millions...

-

Page 95

... one percent. Average loans held for investment used in the denominator in calculating net charge-off, delinquency and nonperforming loan and nonperforming asset rates includes the impact of loans acquired as part of the Chevy Chase Bank acquisition, which were considered purchased credit-impaired...

-

Page 96

... and losses related to REO, combined with increases in core deposit intangible amortization expense, integration costs related to the Chevy Chase Bank acquisition and expenditures related to risk management activities and enhancing our infrastructure. Total Loans: Period-end loans increased by...

-

Page 97

... securities collateralized primarily by credit card loans, auto loans, student loans, auto dealer floor plan inventory loans, equipment loans and home equity lines of credit; municipal securities; and limited Community Reinvestment Act ("CRA") equity securities. Our investment securities portfolio...

-

Page 98

...78 % credit card loans, 7% student loans, 7% auto loans, 6% auto dealer floor plan inventory loans and leases, and 2% equipment loans as of December 31, 2010. Approximately 86% of the securities in our asset-backed security portfolio were rated AAA or its equivalent as of December 31, 2011, compared...

-

Page 99

... quarter of 2011 and the $1.4 billion credit card loan portfolio of HBC in the first quarter of 2011, as well as growth in our Auto Finance, commercial and revolving domestic card balances. Excluding the impact of the addition of the Kohl's and HBC portfolios, total loans increased by $4.9 billion...

-

Page 100

... purchasers, including purchasers who created securitization trusts. These subsidiaries are Capital One Home Loans, which was acquired in February 2005; GreenPoint Mortgage Funding, Inc. ("GreenPoint"), which was acquired in December 2006 as part of the North Fork acquisition; and Chevy Chase Bank...

-

Page 101

... Balance of Mortgage Loans Originated and Sold to Third Parties Based on Category of Purchaser

Unpaid Principal Balance December 31, 2011 2010

(Dollars in billions)

Total

Original Unpaid Principal Balance 2008 2007 2006 2005

Government sponsored enterprises ("GSEs")(1) ...Insured Securitizations...

-

Page 102

...31, 2011, approximately $15 billion in losses have been realized and approximately $11 billion in unpaid principal balance is at least 90 days delinquent. Because we do not service most of the loans we sold to others, we do not have complete information about the underlying credit performance levels...

-

Page 103

... and warranty reserves through the provision for repurchase losses, which we report in our consolidated statements of income as a component of non-interest income for loans originated and sold by Chevy Chase Bank and Capital One Home Loans and as a component of discontinued operations for...

-

Page 104

... the year ended December 31, 2011, primarily driven by increased repurchase activity from Uninsured Securitizations and other whole loan investors. During 2011, we had settlements of repurchase requests totaling $85 million that were charged against the reserve. The table below summarizes changes in...

-

Page 105

... can take many forms, including securitization and servicing activities, the purchase or sale of mortgage-backed or other asset-backed securities in connection with our home loan portfolio and loans to VIEs that hold debt, equity, real estate or other assets. Under previous accounting guidance...

-

Page 106

... measures widely used by investors, analysts, rating agencies and bank regulatory agencies to assess the capital position of financial services companies. There is currently no mandated minimum or "well capitalized" standard for Tier 1 common equity; instead the risk-based capital rules state that...

-

Page 107

... 1 common equity ...Plus: Tier 1 restricted core capital items(4) ...Tier 1 risk-based capital ...Plus: Long-term debt qualifying as Tier 2 capital ...Qualifying allowance for loan and lease losses ...Other Tier 2 components ...Tier 2 risk-based capital ...Total risk-based capital ...Risk-weighted...

-

Page 108

... rules is to ensure that large bank holding companies have robust, forward-looking capital planning processes that account for their unique risks and capital needs to continue operations through times of economic and financial stress. As part of its evaluation of a capital plan, the Federal Reserve...

-

Page 109

... funds at a reasonable price within a reasonable time period. Market Risk: Market risk is the risk that our earnings and/or economic value of equity may be adversely affected by changes in market conditions, including changes in interest rates and foreign currency exchange rates, changes in credit...

-

Page 110

... services industry due to changing regulatory environments and ongoing economic uncertainty. First, we seek to mitigate liquidity risk strategically and tactically. From a strategic perspective, we have acquired and built deposit gathering businesses and significantly reduced our loan to deposit...

-

Page 111

..., our Chief Executive Officer and executive team manage both tactical and strategic reputation issues and build our relationships with the government, media and other constituencies to help strengthen the reputations of both our company and industry. Our actions include taking public positions in...

-

Page 112

... channels to inform associates of their responsibilities, alert them to issues or changes that might affect their activities, and to enable an open flow of information up, down, and across our company. Robust risk management also requires management information to enable controls to work...

-

Page 113

...Risk Management The Chief Risk Officer, in conjunction with the Consumer and Commercial Chief Credit Officers, is responsible for establishing credit risk policies and procedures, including underwriting and hold guidelines and credit approval authority, and monitoring credit exposure and performance...

-

Page 114

...activities, including loans, deposits, securities, shortterm borrowings, long-term debt and derivatives. The market risk positions of our banking entities and the company are calculated separately and in total and are reported in comparison to pre-established limits to the Asset/Liability Management...

-

Page 115

...guidance to the enterprise and business areas. This evaluation and guidance is based on an assessment of the type and degree of legal risk associated with the internal business area practices and activities and of the controls the business has in place to mitigate legal risks. Legal risk is governed...

-

Page 116

... "Consolidated Balance Sheet Analysis-Investment Securities" and credit risk related to derivative transactions in "Note 11-Derivative Instruments and Hedging Activities." Loan Portfolio Composition We provide a variety of lending products. Our primary products include credit cards, auto loans, home...

-

Page 117

... and home equity loans and lines of credit. We currently restrict non-conforming loans to properties within our retail branch footprint. Our underwriting policy limits for these loans include (1) a maximum loan-to-value ratio of 80% for loans without mortgage insurance; (2) a maximum loan-to-value...

-

Page 118

... loans: Domestic installment loans ...International installment loans ...Total installment loans ...Total credit card ...Consumer Banking business: Auto ...Home loan ...Other retail ...Total consumer banking ...Commercial Banking business:(1) Commercial and multifamily real estate ...Middle market...

-

Page 119

... within one to three years. Includes installment loans of $1.9 billion.

We market our credit card products on a national basis throughout the United States, Canada and the United Kingdom. The Credit Card segment accounted for $65.1 billion, or 48% of our total loan portfolio as of December 31, 2011...

-

Page 120

...21: Credit Card Concentrations

December 31, 2011 (Dollars in millions) Loans % of Total 2010 Loans % of Total

Domestic card: California ...Texas ...New York ...Florida ...Illinois ...Pennsylvania ...Ohio ...New Jersey ...Michigan ...Other ...Total domestic card ...International card: United Kingdom...

-

Page 121

... % of Total

Auto: Texas ...California ...Louisiana ...Florida ...Georgia ...Illinois ...New York ...Other ...Total auto ...Home loan: New York ...California ...Louisiana ...Maryland ...Virginia ...New Jersey ...Other ...Total home loan ...Retail banking: Louisiana ...Texas ...New York ...New Jersey...

-

Page 122

... ...Pennsylvania ...Virginia ...California ...Other ...Total commercial lending ...Small-ticket commercial real estate: New York ...California ...Massachusetts ...New Jersey ...Florida ...Other ...Total small-ticket commercial real estate ...Total commercial banking ...Credit Risk Measurement

$13...

-

Page 123

... International credit card and installment Total credit card ...Consumer Banking business: Auto ...Home loan(2) ...Retail banking(2) ...Total consumer banking(2) ...Commercial Banking business: Commercial and multifamily real estate(2) Middle market(2) ...Specialty lending ...Small-ticket commercial...

-

Page 124

... of the end of the period by period-end loans held for investment for the specified loan category. Includes credit card loans that continue to accrue finance charges and fees until charged-off at 180 days. The amounts reported for credit card loans are net of billed finance charges and fees that we...

-

Page 125

...months of consecutive payments, under the modified terms of the loan. Purchased credit-impaired loans: PCI loans primarily include loans acquired from Chevy Chase Bank, which we recorded at fair value at acquisition. Because the initial fair value of these loans included an estimate of credit losses...

-

Page 126

...

(Dollars in millions)

Nonperforming loans held for investment: Consumer Banking business: Auto ...Home loan ...Retail banking ...Total consumer banking ...Commercial Banking business: Commercial and multifamily real estate ...Middle market ...Specialty lending ...Total commercial lending ...Small...

-

Page 127

... date when the account is a specified number of days past due or upon repossession of the underlying collateral. Our charge-off time frame is 180 days for home loans and unsecured small business lines of credit and 120 days for auto and other non-credit card consumer loans. We calculate the charge...

-

Page 128

...." The average loans held for investment used in calculating net charge-off rates includes the impact of loans acquired as part of the Chevy Chase Bank acquisition. Our total net charge-off rate, excluding the impact of acquired Chevy Chase Bank loans, was 3.06%, 5.44% and 6.09% for 2011, 2010 and...

-

Page 129

... Modifications and Restructurings(1)

(Dollars in millions) December 31, 2011 2010(2)

Modified and restructured loans: Credit card(3) ...Auto(4) ...Home loan ...Retail banking ...Commercial ...Total ...Status of modified and restructured loans: Performing ...Nonperforming ...Total ...(1)

$ 898 58...

-

Page 130

... the PCI loans acquired from Chevy Chase Bank in "Note 5-Loans." Allowance for Loan and Lease Losses Our allowance for loan and lease losses represents management's best estimate of incurred loan and lease credit losses inherent in our held-for-investment portfolio as of each balance sheet date. We...

-

Page 131

... lending ...Small-ticket commercial real estate ...Total commercial banking ...Other loans ...Total charge-offs ...Recoveries: Credit Card business: Domestic credit card and installment ...International credit card and installment ...Total credit card ...Consumer Banking business: Auto ...Home loan...

-

Page 132

... business: Commercial and multifamily real estate ...Middle market ...Specialty lending ...Total commercial lending ...Small-ticket commercial real estate ...Total commercial banking ...Other loans ...Total recoveries ...Net charge-offs ...Impact from acquisitions, sales and other changes ...Balance...

-

Page 133

...(2) ...International credit card and installment ...Total credit card(2) ...Consumer Banking: Auto ...Home loan ...Retail banking ...Total consumer banking ...Commercial Banking: Commercial and multifamily real estate ...Middle market ...Specialty lending ...Total commercial lending ...Small-ticket...

-

Page 134

... 31, 2011 2010

(Dollars in millions)

Non-interest bearing ...NOW accounts ...Money market deposit accounts ...Savings accounts ...Other consumer time deposits ...Total core deposits ...Public fund certificates of deposit $100,000 or more ...Certificates of deposit $100,000 or more ...Foreign time...

-

Page 135

...31, 2011 Period End Balance Average Balance Interest Expense % of Average Deposits Average Deposit Rate

(Dollars in millions)

Non-interest bearing ...NOW accounts ...Money market deposit accounts ...Savings accounts ...Other consumer time deposits ...Total core deposits ...Public fund certificates...

-

Page 136

... End Balance Average Balance Interest Expense % of Average Deposits Average Deposit Rate

(Dollars in millions)

Non-interest bearing ...NOW accounts ...Money market deposit accounts ...Savings accounts ...Other consumer time deposits ...Total core deposits ...Public fund certificates of deposit...

-

Page 137

... to access the federal funds market in a time of need. We expect monthly fluctuations in our borrowings, as borrowing amounts are highly dependent on our counterparties' cash positions. Our FHLB membership is secured by our investment in FHLB stock, which totaled $362 million as of December 31, 2011...

-

Page 138

... 17-Employee Benefit Plans."

Table 38: Contractual Obligations

December 31, 2011 > 1 Year > 3 Years to 3 Years to 5 Years > 5 Years

(Dollars in millions)

Up to 1 Year

Total

Interest-bearing time deposits(1) ...Senior and subordinated notes ...Other borrowings(2) ...Operating leases ...Purchase...

-

Page 139

...unsecured funding as part of our overall financing programs. Table 39 provides a summary of the credit ratings for the senior unsecured debt of Capital One Financial Corporation, COBNA and CONA as of December 31, 2011, and as of the date of this Report.

Table 39: Senior Unsecured Debt Credit Ratings...

-

Page 140

... Exchange Risk Foreign exchange risk represents exposure to changes in the values of current holdings and future cash flows denominated in other currencies. The types of instruments exposed to this risk include investments in foreign subsidiaries, foreign currency-denominated loans and securities...

-

Page 141

... policy also includes the use of derivatives to hedge material foreign currency denominated transactions to limit our earnings exposure to foreign exchange risk. Table 40 shows the estimated percentage impact on our adjusted projected net interest income and economic value of equity, calculated...

-

Page 142

... asset/liability policy limits as of December 31, 2011 and 2010. As noted above, in conjunction with our close of the ING Direct acquisition on February 17, 2012, we terminated the ING Direct related swap transactions in February 2012. The interest rate risk models that we use in deriving these...

-

Page 143

... ...Small-ticket commercial real estate ...Total commercial banking business ...Other: Other loans(1) ...Total reported loans held for investment ...Securitization adjustments: Credit Card business: Credit card loans: Domestic credit card loans ...International credit card loans ...Total credit card...

-

Page 144

... loans ...International installment loans ...Total installment loans ...Total credit card business ...Consumer Banking business: Auto ...Home loan ...Retail banking ...Total consumer banking business ...Total consumer loans ...Commercial Banking business: Commercial and multifamily real estate...

-

Page 145

... and $1.1 billion in 2011, 2010, 2009, 2008 and 2007, respectively. The Chevy Chase Bank acquired loan portfolio is included in loans held for investment, but excluded from delinquent loans as these loans are considered performing in accordance with our expectations as of the purchase date, as we...

-

Page 146

...

(Dollars in millions)

2011

2010

2008

2007

Nonperforming loans held for investment:(1)(2) Consumer Banking business: Auto ...Home loan ...Retail banking(3) ...Total consumer banking business ...Commercial Banking business: Commercial and multifamily real estate ...Middle market ...Specialty...

-

Page 147

...average balances of the acquired Chevy Chase Bank loan portfolio, which are included in the total average loans held for investment used in calculating the net charge-off rates, were $5.0 billion , $6.3 billion and $6.8 billion for 2011, 2010 and 2009, respectively. Calculated for each loan category...

-

Page 148

...Domestic credit card and installment ...International credit card and installment ...Consumer banking ...Commercial banking ...Other loans ...Total recoveries ...Net charge-offs Impact from acquisitions, sales and other changes(4) ...Balance as of end of period ...Allowance for loan and lease losses...

-

Page 149

...Other ...Tier 1 common equity ...Plus: Tier 1 restricted core capital items(5) ...Tier 1 capital ...Plus: Long-term debt qualifying as Tier 2 capital ...Qualifying allowance for loan and lease losses ...Other Tier 2 components ...Tier 2 capital ...Total risk-based capital(6) ...Risk-weighted assets...

-

Page 150

Item 7A. Quantitative and Qualitative Disclosures about Market Risk For a discussion of the quantitative and qualitative disclosures about market risk, see "MD&A-Risk Management-Market Risk Management" and "MD&A-Market Risk Profile."

130

-

Page 151

... the risk that controls may become inadequate because of changes in conditions, or that the degree of compliance with the policies or procedures may deteriorate. Management completed an assessment of the effectiveness of the Company's internal control over financial reporting as of December 31, 2011...

-

Page 152

...Company Accounting Oversight Board (United States), the consolidated balance sheets of Capital One Financial Corporation as of December 31, 2011 and 2010, and the related consolidated statements of income, changes in stockholders' equity and cash flows for each of the three years in the period ended...

-

Page 153

... Capital One Financial Corporation as of December 31, 2011 and 2010, and the related consolidated statements of income, changes in stockholders' equity, and cash flows for each of the three years in the period ended December 31, 2011. These financial statements are the responsibility of the Company...

-

Page 154

... Supplementary Data CAPITAL ONE FINANCIAL CORPORATION CONSOLIDATED STATEMENTS OF INCOME

(Dollars in millions, except per share-related data) Year Ended December 31, 2011 2010 2009

Interest income: Loans held for investment, including past-due fees ...Investment securities ...Other ...Total interest...

-

Page 155

CAPITAL ONE FINANCIAL CORPORATION CONSOLIDATED BALANCE SHEETS

(Dollars in millions, except per share data) December 31, 2011 2010

Assets: Cash and due from banks ...Interest-bearing deposits with banks ...Federal funds sold and securities purchased under agreements to resell ...Cash and cash ...

-

Page 156

... preferred stock ...Compensation expense for restricted stock awards and stock options ...Issuance of common stock for acquisition ...2,560,601 Allocation of ESOP shares ...Balance as of December 31, 2009 ...502,394,396 Cumulative effect from January 1, 2010 adoption of new consolidation accounting...

-

Page 157

CAPITAL ONE FINANCIAL CORPORATION CONSOLIDATED STATEMENTS OF CHANGES IN STOCKHOLDERS' EQUITY

Accumulated Other Comprehensive Total Common Stock Preferred Additional Paid-In Retained Income Treasury Stockholders' Shares Amount Stock Capital Earnings (Loss) Stock Equity 3,147 (39) (39) (14) (13) 26 (...

-

Page 158

...Principal recoveries of loans previously charged off ...Additions of premises and equipment ...Net cash provided by (payment for) companies acquired ...Net cash provided by (used in) investing activities ...Financing activities: Net increase (decrease) in deposits ...Net decrease in securitized debt...

-

Page 159

...largest banks in the United States based on deposits, we serve banking customers through branch locations primarily in New York, New Jersey, Texas, Louisiana, Maryland, Virginia and the District of Columbia. In addition to bank lending and depository services, we offer credit and debit card products...

-

Page 160

... except marketable equity securities, which we carry at fair value with changes in fair value included in accumulated other comprehensive income. We typically report investments accounted for under the equity or cost method in other assets on our consolidated balance sheets, and include our share of...

-

Page 161

... loans consist of auto, home, and retail banking loans. Commercial loans consist of commercial and multifamily real estate, middle market, specialty lending and small-ticket commercial real estate loans. We historically have securitized credit card loans, auto loans, home loans and installment loans...

-

Page 162

... investment, loans held for sale and purchased-credit impaired loans are described below. Loans Held for Investment Loans that we have the ability and intent to hold for the foreseeable future and loans associated with on-balance sheet securitization transactions accounted for as secured borrowings...

-

Page 163

... status, current loan-to-value ratio, the geographic location of the borrower or collateral and internal risk ratings. In connection with the acquisition of Chevy Chase Bank on February 27, 2009, we concluded that the substantial majority of loans we acquired from Chevy Chase Bank were PCI loans...

-

Page 164

... canceling the customer's available line of credit on the credit card, reducing the interest rate on the card, and placing the customer on a fixed payment plan not exceeding 60 months. These modifications may result in our receiving the full amount due, or certain installments due, under the loan...

-

Page 165

... becomes 90 days past due for auto, home loans, and unsecured small business revolving lines of credit and 120 days past due for all other non-credit card consumer loans, including installment loans. Commercial loans: We classify commercial loans as nonperforming as of the date we determine that the...

-

Page 166

..., based on applicable accounting guidance, include larger balance nonperforming loans and TDR loans. Our policies for identifying loans as individually impaired, by loan category, are as follows Credit card loans: Credit card loans that have been modified in a troubled debt restructuring are...

-

Page 167

... date when the account is a specified number of days past due or upon repossession of the underlying collateral. Our charge-off time frame is 180 days for home loans and unsecured small business lines of credit and 120 days for auto and other non-credit card consumer loans. We calculate the charge...

-

Page 168

... losses ("the allowance") that represents management's best estimate of incurred loan and lease credit losses inherent in our held-for-investment portfolio as of each balance sheet date. We do not maintain an allowance for held-for-sale loans or purchased-credit impaired loans that are performing...

-

Page 169

... loss experience for loans with similar risk characteristics and consideration of the current credit quality of the portfolio, supplemented by management judgment and interpretation. We apply internal risk ratings to commercial loans, which we use to assess credit quality and derive a total loss...

-

Page 170

... by Chevy Chase Bank. Prior to January 1, 2010, transfers of our credit card receivables, installment loans and certain option-adjustable rate mortgage loans to our securitization trusts were accounted for as sales and treated as off-balance sheet. At the adoption of these new accounting standards...

-

Page 171

... of mortgage loans and related debt securities issued to third party investors were consolidated and the retained interests and mortgage servicing rights related to these newly consolidated trusts were eliminated in consolidation. See "Note 1-Summary of Significant Accounting Policies" and "Note...

-

Page 172

... in current earnings. We did not make any material fair value option elections as of and for the years ended December 31, 2011 and 2010. See "Note 19-Fair Value of Financial Instruments" for additional information. Representation and Warranty Reserve In connection with their sales of mortgage loans...

-

Page 173

... foreign exchange risks. As part of this process, we consider the customers' suitability for the risk involved, and the business purpose for the transaction. These derivatives do not qualify for hedge accounting and are considered trading derivatives with changes in fair value recognized in current...

-

Page 174

... International Inc. ("MasterCard") and Visa U.S.A. Inc. ("Visa") and are based on cardholder purchase volumes. We recognize interchange income as earned. Annual membership fees and direct loan origination costs specific to credit card loans are deferred and amortized over one year on a straight-line...

-

Page 175

... 2011 with early adoption permitted. The adoption of this amended accounting guidance in the third quarter of 2011 resulted in a net increase in loan modifications considered to be TDRs of $56 million for consumer loans and $77 million for commercial loans. The allowance for credit losses associated...

-

Page 176

...is effective for public entities during interim and annual periods beginning after December 15, 2011, with early adoption prohibited. The new guidance requires prospective application and disclosure in the period of adoption of the change, if any, in valuation techniques and related inputs resulting...

-

Page 177

... on our consolidated financial statements. NOTE 2-ACQUISITIONS AND RESTRUCTURING ACTIVITIES We regularly explore opportunities to enter into strategic partnership agreements or acquire financial services companies and businesses to expand our distribution channels and grow our customer base. We...

-

Page 178

...number of customer accounts, and provides an additional distribution channel. The acquisition included outstanding credit card loan receivables with a fair value of approximately $1.4 billion, and a transfer of approximately 400 employees directly involved in managing the HBC portfolio. We accounted...

-

Page 179

CAPITAL ONE FINANCIAL CORPORATION NOTES TO CONSOLIDATED STATEMENTS-(Continued) losses in our consolidated statements of income. We also report the related allowance for loan and lease losses attributable to the Kohl's portfolio in our consolidated balance sheets net of the loss sharing amount due ...

-

Page 180

... securities collateralized primarily by credit card loans, auto loans and leases, student loans, auto dealer floor plan inventory loans and leases, equipment loans, and other; municipal securities and limited Community Reinvestment Act ("CRA") equity securities. Our investment securities portfolio...

-

Page 181

CAPITAL ONE FINANCIAL CORPORATION NOTES TO CONSOLIDATED STATEMENTS-(Continued) Securities Amortized Cost and Fair Value All of our investment securities were classified as available-for-sale as of December 31, 2011 and 2010, and are reported in our consolidated balance sheet at fair value. The ...

-

Page 182

... The book value of Fannie Mae, Freddie Mac and Ginnie Mae investments exceeded 10% of our stockholders' equity as of December 31, 2011. Consists of securities collateralized by credit card loans, auto loans, auto dealer floor plan inventory loans and leases, student loans, equipment loans, and other...

-

Page 183

... ONE FINANCIAL CORPORATION NOTES TO CONSOLIDATED STATEMENTS-(Continued)

Less than 12 Months Gross Unrealized Fair Value Losses December 31, 2010 12 Months or Longer Gross Unrealized Fair Value Losses Total Gross Unrealized Losses

(Dollars in millions)

Fair Value

Securities available for sale...

-

Page 184

...the security; external credit ratings and the failure of the issuer to make scheduled interest or principal payments; the value of underlying collateral; our intent and ability to hold the security; and current market conditions. We assess measure and recognize OTTI in accordance with the accounting...

-

Page 185

... purchase yield. The non-credit component represents the difference between the security's fair value and the present value of expected future cash flows. The following table summarizes other-than-temporary impairment losses on debt securities recognized in earnings in 2011, 2010 and 2009:

(Dollars...

-

Page 186

CAPITAL ONE FINANCIAL CORPORATION NOTES TO CONSOLIDATED STATEMENTS-(Continued) The table below presents activity for the years ended December 31, 2011, 2010 and 2009, related to the credit component of OTTI recognized in earnings on investment debt securities for which a portion of the OTTI losses, ...

-

Page 187

...losses ...Net realized gains ...Total proceeds from sales ...Securities Pledged

$ 259 0 $ 259 $9,169

$ $

141 0 141

$ $

231 (13) 218

$12,466

$13,410

As part of our liquidity management strategy, we pledge securities to secure borrowings from the Federal Home Loan Bank ("FHLB") and the Federal...

-

Page 188

... real estate, middle market, specialty lending and small-ticket commercial real estate loans.

(Dollars in millions) December 31, 2011 2010

Credit card business: Domestic credit card loans ...International credit card loans ...Total credit card loans ...Domestic installment loans ...International...

-

Page 189

...,536 International credit card ...8,028 Total credit card ...Consumer Banking: Auto ...Home loan ...Retail banking ...Total consumer banking ...Commercial Banking: Commercial and multifamily real estate ...Middle market ...Specialty lending ...Total commercial lending ...Small-ticket commercial real...

-

Page 190

... $1,176 International credit card ...7,090 132 97 203 Total credit card ...Consumer Banking: Auto ...Home loan ...Retail banking ...Total consumer banking ...Commercial Banking: Commercial and multifamily real estate ...Middle market ...Specialty lending ...Total commercial lending ...Small-ticket...

-

Page 191

... ONE FINANCIAL CORPORATION NOTES TO CONSOLIDATED STATEMENTS-(Continued)

Credit Card: Risk Profile by Geographic Region and Delinquency Status

December 31, 2011 (Dollars in millions) Amount % of Total(1) 2010 Amount % of Total(1)

Domestic credit card and installment loans: California ...Texas ...New...

-

Page 192

...-charge offs for the years ended December 31, 2011 and 2010.

Consumer Banking: Risk Profile by Geographic Region, Delinquency Status and Performing Status

December 31, 2011 PCI Loans % of Loans Total(1)

(Dollars in millions)

Non-PCI Loans % of Loans Total(1)

Total Loans % of Total(1)

Auto: Texas...

-

Page 193

CAPITAL ONE FINANCIAL CORPORATION NOTES TO CONSOLIDATED STATEMENTS-(Continued)

December 31, 2011 Auto Amount Rate Home Loan Amount Rate Retail Banking Amount Rate Total Consumer Banking Amount Rate

(Dollars in millions)

Credit performance:(2) 30+ day delinquencies ...90+ day delinquencies ......

-

Page 194

CAPITAL ONE FINANCIAL CORPORATION NOTES TO CONSOLIDATED STATEMENTS-(Continued)

December 31, 2010 Auto Amount Rate Home Loan Amount Rate Retail Banking Amount Rate Total Consumer Banking Amount Rate

(Dollars in millions)

Credit performance:(2) 30+ day delinquencies ...90+ day delinquencies ......

-

Page 195

CAPITAL ONE FINANCIAL CORPORATION NOTES TO CONSOLIDATED STATEMENTS-(Continued)

Home Loan: Risk Profile by Vintage, Geography, Lien Priority and Interest Rate Type

December 31, 2011 PCI Loans % of Amount Total(1)

(Dollars in millions)

Non-PCI Loans % of Amount Total(1)

Total Home Loans % of Amount...

-

Page 196

...

Percentages within each risk category calculated based on total held-for-investment home loans. Represents the top ten states in which we have the highest concentration of home loans.

Commercial Banking We evaluate the credit risk of commercial loans individually and use a risk-rating system to...

-

Page 197

... ratings of our commercial loan portfolio as of December 31, 2011 and 2010.

Commercial Banking: Risk Profile by Geographic Region and Internal Risk Rating(1)

December 31, 2011 Small-ticket Specialty % of Commercial % of Total % of Lending Total(2) Real Estate Total(2) Commercial Total(2)

(Dollars...

-

Page 198

...Market Total(2) Lending Total(2) Real Estate Total(2) Commercial Total(2)

(Dollars in millions) Geographic concentration:(3) Non-PCI loans: Northeast ...Mid-Atlantic ...South ...Other ...Total non-PCI loans ...PCI loans ...Total ...Internal risk Non-PCI loans: Noncriticized ...Criticized performing...

-

Page 199

...Domestic credit card and installment loan ...International credit card and installment loans ...Total credit card and installment loans(1) ...Consumer banking: Auto ...Home loan ...Retail banking ...Total consumer banking ...Commercial banking: Commercial and multifamily real estate ...Middle market...

-

Page 200

...Domestic credit card and installment loan ...International credit card and installment loans ...Total credit card and installment loans(1) ...Consumer banking: Auto ...Home loan ...Retail banking ...Total consumer banking ...Commercial banking: Commercial and multifamily real estate ...Middle market...

-

Page 201

... Balance Activity(4)(8) (Months)(5) Activity(6)(8) Reduction(7)

(Dollars in millions)

Credit card: Domestic credit card ...$ 321 International credit card ...253 Total credit card ...Consumer banking: Auto ...Home loan ...Retail banking ...Total consumer banking ...Commercial banking: Commercial...

-

Page 202

... the end of the period presented.

December 31, 2011 Number of Total contracts Loans

(Dollars in millions)

Credit card: Domestic credit card ...International credit card(1) ...Total credit card ...Consumer banking: Auto ...Home loan ...Retail banking ...Total consumer banking ...Commercial banking...

-

Page 203

...and losses of $33 million for the year ended December 31, 2010. The cumulative impairment recognized on PCI loans totaled $27 million as of December 31, 2011 and $33 million as of December 31, 2010. The following table presents changes in the accretable yield related to the acquired Chevy Chase Bank...

-

Page 204

... losses ("the allowance") that represents management's best estimate of incurred loan and lease credit losses inherent in our held-for-investment portfolio as of each balance sheet date. We do not maintain an allowance for held for sale loans or purchased credit-impaired loans that are performing...

-

Page 205

..., by portfolio segment, for 2011 and 2010:

Combined Unfunded Allowance Consumer Lending & Credit Home Retail Total Total Commitments Unfunded Card Auto Loan Banking Consumer Commercial Other(1) Allowance Reserve Reserve $ 236 $1,076 $ 785 $ 140 $ 4,127 $103 $ 4,230

(Dollars in millions)

Balance as...

-

Page 206

... methodology, and the recorded investment of the related loans as of December 31, 2011 and 2010:

December 31, 2011 Consumer Home Retail Total Auto Loan Banking Consumer Commercial Other

(Dollars in millions)

Credit Card

Total

Allowance for loan and lease losses by impairment methodology: Formula...

-

Page 207

... securitized credit card loans, auto loans, home loans and installment loans, which provided a source of funding for us and as a means of transferring a certain portion of the economic risk of the loans or debt securities to third parties. Under revised consolidation accounting guidance that...

-

Page 208

... Related VIEs We historically have securitized credit card loans, auto loans, home loans and installment loans. In a securitization transaction, assets from our balance sheet are transferred to a trust we establish, which typically meets the definition of a VIE. The trust then issues various forms...

-

Page 209

...securitization-related VIEs in which we had continuing involvement as of December 31, 2011 and 2010:

Non-Mortgage Credit Card Auto Loan Other Loan Option Arm Mortgage GreenPoint HELOCs GreenPoint Manufactured Housing

(Dollars in millions)

December 31, 2011: Securities held by third-party investors...

-

Page 210

... transactions and servicing were transferred to a third party in the sale transaction. We do not consolidate the trusts used for the securitization of manufactured housing loans because we do not have the power to direct the activities that most significantly impact the economic performance of the...

-

Page 211

... result of changes in the fair value of retained interests are presented below:

(Dollars in millions) Year Ended December 31, 2011 2010(1) 2009

Interest only strip valuation changes ...Fair value adjustments related to spread accounts ...Fair value adjustments related to investors' accrued interest...

-

Page 212

CAPITAL ONE FINANCIAL CORPORATION NOTES TO CONSOLIDATED STATEMENTS-(Continued) The changes in the fair value of retained interests are primarily driven by rate assumption changes and volume fluctuations. All of these retained residual interests are subject to loss in the event assumptions used to ...

-

Page 213

... affordable housing tax credits for these investments. The activities of these entities are financed with a combination of invested equity capital and debt. For those investment funds considered to be VIEs, we are not required to consolidate if we do not have the power to direct the activities that...

-

Page 214

... of the Investor Entities are financed with a combination of invested equity capital and debt. The activities of the CDEs are financed solely with invested equity capital. We receive federal and state tax credits for these investments. We consolidate the VIEs in which we have the power to direct the...

-

Page 215

...in order to maintain each reporting unit's equity capital requirements. Our discounted cash flow analysis required management to make judgments about future loan and deposit growth, revenue growth, credit losses, and capital rates. The cash flows were discounted to present value using reporting unit...

-

Page 216

... current lease contracts and the fair market value of the lease contracts at the acquisition date. The other intangible items relate to customer lists and brokerage relationships. In connection with the acquisition of the credit card loan portfolios of Sony, HBC and Kohl's, we recognized purchased...

-

Page 217

... and the Kohl's private-label credit card portfolio in the second quarter of 2011. Relates to the acquisition of the existing HBC credit card portfolio in the first quarter of 2011.

Intangible assets, which are reported in other assets on our consolidated balance sheets, are amortized over their...

-

Page 218

... based on certain risk characteristics, including loan type, note rate and investor servicing requirements. The following table sets forth the changes in the fair value of MSRs during the year ended December 31, 2011 and 2010:

(Dollars in millions) December 31, 2011 2010

Balance at beginning of...

-

Page 219

CAPITAL ONE FINANCIAL CORPORATION NOTES TO CONSOLIDATED STATEMENTS-(Continued) As of December 31, 2011, our mortgage loan servicing portfolio consisted of mortgage loans with an aggregate unpaid principal balance of $27 billion, of which $18 billion was serviced for other investors. As of December ...

-

Page 220

... We also access the capital markets to meet our funding needs through loan securitization transactions and the issuance of senior and subordinated debt. As of December 31, 2011, we had an effective shelf registration statement filed with the U.S. Securities & Exchange Commission ("SEC") under which...

-

Page 221

... investment securities, residential home loan portfolio, multifamily loans, commercial real-estate loans and home equity lines of credit, totaling $6.9 billion and $1.1 billion as of December 31, 2011 and 2010, respectively. Composition of Customer Deposits, Short-term Borrowings and Long-term Debt...

-

Page 222

... ONE FINANCIAL CORPORATION NOTES TO CONSOLIDATED STATEMENTS-(Continued)

December 31, 2011 Weighted Average Interest Rate Interest Rate 2010

(Dollars in millions)

Maturity Date

Long-term debt: Securitized debt obligations ...2012 - 2026 0.20% - 6.40% Senior and subordinated notes: Fixed unsecured...

-

Page 223