Capital One 2013 Annual Report Download - page 73

Download and view the complete annual report

Please find page 73 of the 2013 Capital One annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

|

|

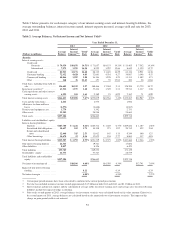

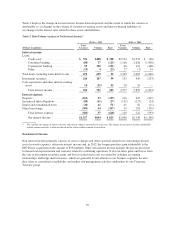

We discuss changes in the valuation inputs and assumptions used in determining the fair value of our financial

instruments, including the extent to which we have relied on significant unobservable inputs to estimate fair

value and our process for corroborating these inputs, in “Note 18—Fair Value of Financial Instruments.”

Key Controls Over Fair Value Measurement

We have a governance framework and a number of key controls that are intended to ensure that our fair value

measurements are appropriate and reliable. Our governance framework provides for independent oversight and

segregation of duties. Our control processes include review and approval of new transaction types, price

verification and review of valuation judgments, methods, models, process controls and results. Groups

independent from our trading and investing functions, including our Corporate Valuations Group (“CVG”), Fair

Value Committee and Model Validation Group, participate in the review and validation process. The fair

valuation governance process is set up in a manner that allows the Chairperson of the Fair Value Committee

(“FVC”) to escalate valuation disputes that cannot be resolved at the FVC to a more senior committee called the

Valuations Advisory Committee for resolution. The Valuations Advisory Committee (“VAC”) is chaired by the

Chief Financial Officer and includes other senior management. The VAC is only convened to review escalated

valuation disputes and did not meet during 2013.

The CVG performs periodic independent verification of fair value measurements to determine if assigned fair

values are reasonable. For example, in cases where we rely on third party pricing services to obtain fair value

measures, we analyze pricing variances among different pricing sources and validate the final price used by

comparing the information to additional sources, including dealer pricing indications in transaction results and

other internal sources, where necessary. Additional validation procedures performed by the CVG include

reviewing (either directly or indirectly through the reasonableness of assigned fair values) valuation inputs and

assumptions, and monitoring acceptable variances between recommended prices and validation prices. The CVG

and the Trade Analytics and Valuation team perform due diligence reviews of the third party pricing services by

comparing their prices with prices from other sources and reviewing other control documentation. Additionally,

when necessary, the CVG and Trade Analytics and Valuation Team (“TAV”) challenge prices from third party

vendors to ensure reasonableness of prices through a pricing challenge process. This may include a request for a

transparency of the assumptions used by the third party.

The FVC, which includes representation from business areas, our Risk Management division and our Finance

division, is a forum for discussing fair market valuations, inputs, assumptions, methodologies, variance

thresholds, valuation control environment and material risks or concerns related to fair market valuations.

Additionally, the FVC is empowered to resolve valuation disputes between the primary valuation providers and

the CVG. It provides guidance and oversight to ensure an appropriate valuation control environment. The FVC

regularly reviews and approves our valuation methodologies to ensure that our methodologies and practices are

consistent with industry standards and adhere to regulatory and accounting guidance. The Chief Financial Officer

determines when material issues or concerns regarding valuations shall be raised to the Audit Committee or other

delegated committee of the Board of Directors.

We have a model policy, established by an independent Model Risk Office, which governs the validation of

models and related supporting documentation to ensure the appropriate use of models for pricing. The Model

Validation Group is part of the Model Risk Office and validates all models and provides ongoing monitoring of

their performance, including the validation and monitoring of the performance of all valuation models.

Representation and Warranty Reserve

In connection with their sales of mortgage loans, certain subsidiaries entered into agreements containing varying

representations and warranties about, among other things, the ownership of the loan, the validity of the lien

securing the loan, the loan’s compliance with any applicable loan criteria established by the purchaser, including

underwriting guidelines and the ongoing existence of mortgage insurance, and the loan’s compliance with

applicable federal, state and local laws. We may be required to repurchase the mortgage loan, indemnify the

investor or insurer, or reimburse the investor for loan and lease losses incurred on the loan in the event of a

material breach of contractual representations or warranties.

53