Capital One 2013 Annual Report Download - page 271

Download and view the complete annual report

Please find page 271 of the 2013 Capital One annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

261 -

262

262 -

263

263 -

264

264 -

265

265 -

266

266 -

267

267 -

268

268 -

269

269 -

270

270 -

271

271 -

272

272 -

273

273 -

274

274 -

275

275 -

276

276 -

277

277 -

278

278 -

279

279 -

280

280 -

281

281 -

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

|

|

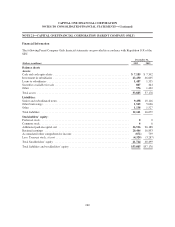

CAPITAL ONE FINANCIAL CORPORATION

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS—(Continued)

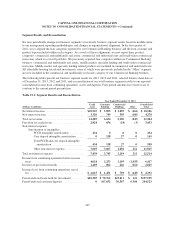

As indicated in the table below, most of the reserves relate to the $27 billion in original principal balance of

mortgage loans sold directly to the GSEs or to the Active Insured Securitizations.

Table 20.4: Allocation of Representation and Warranty Reserves

Reserve Liability

December 31, Loans Sold

2005 to 2008(1)

(Dollars in millions, except for loans sold) 2013 2012

Selected period-end data:

GSEs and Active Insured Securitizations ................................ $ 965 $817 $ 27

Inactive Insured Securitizations and Others .............................. 207 82 84

Total ............................................................ $1,172 $899 $111

(1) Reflects, in billions, the total original principal balance of mortgage loans originated by our subsidiaries and sold to third party investors

between 2005 and 2008.

In establishing reserves for the $11 billion original principal balance of GSE loans, we rely on the historical

relationship between GSE loan losses and repurchase outcomes for each GSE, adjusted for any settlements, to

estimate: (1) the percentage of current and future GSE loan defaults that we anticipate will result in repurchase

requests from the GSEs over the lifetime of the GSE loans; and, (2) the percentage of those repurchase requests

that we anticipate will result in actual repurchases. We rely on estimated collateral valuations and loss forecast

models to estimate our lifetime liability on GSE loans. This reserving approach to the GSE loans reflects the

historical interaction with the GSEs around repurchase requests, and also includes anticipated repurchases

resulting from mortgage insurance rescissions. Although our assumed future claims rate considers the most

recent claims experience and actual repurchases, an increase in GSE claims and/or repurchases could result in an

increase in our reserve. We have entered into and completed repurchase or settlement agreements with respect to

the majority of our exposure within this category.

Our reserves also could be impacted by any claims which may be brought by governmental agencies under the

Financial Institutions Reform, Recovery, and Enforcement Act (“FIRREA”), the False Claims Act, or other

federal or state statutes. For example, in 2013, GreenPoint and Capital One received requests for information

and/or subpoenas from various governmental regulators and law enforcement authorities, including members of

the RMBS Working Group, a federal and state law enforcement effort focused on investigating fraud and abuse

in the RMBS Market relating to the mortgage originations, mortgage loan sales, and the mortgage securitization

process. We are cooperating with these regulators and other authorities in responding to such requests.

For the $16 billion original principal balance in Active Insured Securitizations, our reserving approach reflects

our historical interaction with monoline bond insurers around repurchase requests. Typically, monoline bond

insurers allege a very high repurchase rate with respect to the mortgage loans in the Active Insured Securitization

category. In response to these repurchase requests, our subsidiaries typically request information from the

monoline bond insurers demonstrating that the contractual requirements around a valid repurchase request have

been satisfied. In response to these requests for supporting documentation, monoline bond insurers typically

initiate litigation. Accordingly, our reserves within the Active Insured Securitization segment are not based upon

the historical repurchase rate with monoline bond insurers, but rather upon the expected resolution of litigation

with the monoline bond insurers. Every bond insurer within this category is pursuing a substantially similar

litigation strategy either through active or probable litigation. Accordingly, our representation and warranty

reserves for this category are litigation reserves.

251