Capital One 2013 Annual Report Download - page 104

Download and view the complete annual report

Please find page 104 of the 2013 Capital One annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

|

|

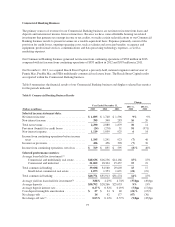

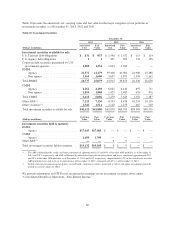

OFF-BALANCE SHEET ARRANGEMENTS AND VARIABLE INTEREST ENTITIES

In the ordinary course of business, we are involved in various types of arrangements with limited liability

companies, partnerships or trusts that often involve special purpose entities and variable interest entities (“VIE”).

Some of these arrangements are not recorded on our consolidated balance sheets or may be recorded in amounts

different from the full contract or notional amount of the arrangements, depending on the nature or structure of,

and accounting required to be applied to, the arrangement. These arrangements may expose us to potential losses

in excess of the amounts recorded in the consolidated balance sheets. Our involvement in these arrangements can

take many forms, including securitization and servicing activities, the purchase or sale of mortgage-backed or

other asset-backed securities in connection with our home loan portfolio and loans to VIEs that hold debt, equity,

real estate or other assets.

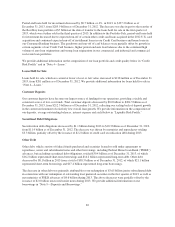

Our continuing involvement in unconsolidated VIEs primarily consists of certain mortgage loan trusts and

community reinvestment and development entities. The carrying amount of assets and liabilities of these

unconsolidated VIEs was $3.4 billion and $0.5 billion, respectively, as of December 31, 2013, and our maximum

exposure to loss was $3.9 billion as of December 31, 2013. We provide a discussion of our activities related to

these VIEs in “Note 6—Variable Interest Entities and Securitizations.”

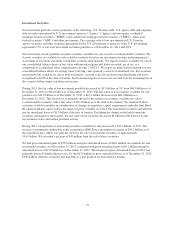

CAPITAL MANAGEMENT

The level and composition of our equity capital are determined by multiple factors, including our consolidated

regulatory capital requirements and an internal risk-based capital assessment, and may also be influenced by

rating agency guidelines, subsidiary capital requirements, the business environment, conditions in the financial

markets and assessments of potential future losses due to adverse changes in our business and market

environments.

Capital Standards and Prompt Corrective Action

Bank holding companies and national banks are subject to capital adequacy standards adopted by the Federal

Reserve and the OCC, respectively. The capital adequacy standards set forth minimum risk-based and leverage

capital requirements that are based on quantitative and qualitative measures of assets and off-balance sheet items.

Under the capital adequacy standards, bank holding companies and national banks currently are required to

maintain a total risk-based capital ratio of at least 8%, a Tier 1 risk-based capital ratio of at least 4% and a Tier 1

leverage capital ratio of at least 4% in order to be considered adequately capitalized.

National banks also are subject to prompt corrective action (“PCA”) capital regulations. Under PCA regulations,

a national bank is considered to be well capitalized if it maintains a total risk-based capital ratio of at least 10%

(200 basis points higher than the minimum capital standard above), a Tier 1 risk-based capital ratio of at least 6%

(200 basis points higher than the minimum capital standard above), a Tier 1 leverage capital ratio of at least 5%

(100 basis points higher than the minimum capital standard above) and is not subject to any supervisory

agreement, order or directive to meet and maintain a specific capital level for any capital measure. A bank is

considered to be adequately capitalized if it meets the above minimum capital standards and does not otherwise

meet the well capitalized definition. Currently, PCA capital requirements do not apply to bank holding

companies.

We also disclose a Tier 1 common ratio for our bank holding company, which is a regulatory capital measure

widely used by investors, analysts, rating agencies and bank regulatory agencies to assess the capital position of

financial services companies. While there is currently no mandated minimum or “well capitalized” standard for

the Tier 1 common ratio, the Federal Reserve, the OCC and the FDIC (collectively, the U.S. federal banking

agencies) recently finalized a new capital rule (the “Final Rule”) that implements the Basel III capital accord

84