Capital One 2013 Annual Report Download - page 273

Download and view the complete annual report

Please find page 273 of the 2013 Capital One annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

263 -

264

264 -

265

265 -

266

266 -

267

267 -

268

268 -

269

269 -

270

270 -

271

271 -

272

272 -

273

273 -

274

274 -

275

275 -

276

276 -

277

277 -

278

278 -

279

279 -

280

280 -

281

281 -

282

282 -

283

283 -

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

|

|

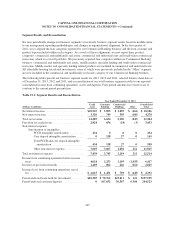

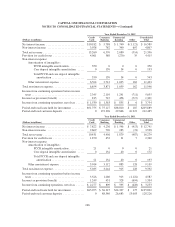

CAPITAL ONE FINANCIAL CORPORATION

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS—(Continued)

In estimating reasonably possible future losses in excess of our current reserves, we assume a portion of the

inactive securitizations become active and for all Insured Securitizations, we assume loss rates on the high end of

those observed in monoline settlements or court rulings. For our remaining GSE exposures, Uninsured

Securitizations and whole loan exposures, our reasonably possible risk estimates assume lifetime loss rates and

claims rates at the highest levels of our past experience and also consider the limited instances of observed

settlements. We do not assume claim rates or loss rates for these risk categories will be as high as those assumed

for the Active Insured Securitizations, however, based on industry precedent. Should the number of claims or the

loss rates on these claims increase significantly, our estimate of reasonably possible risk would increase

materially. We also assume that we will resolve any loan repurchase requests relating to loans originated more

than six years ago at a discount as compared to those originated within six years of a repurchase claim because of

the pending legal arguments in various matters around the applicable statute of limitations.

Notwithstanding our ongoing attempts to estimate a reasonably possible amount of future losses beyond our

current accrual levels based on current information, it is possible that actual future losses will exceed both the

current accrual level and our current estimate of the amount of reasonably possible losses. Our reserve and

reasonably possible estimates involve considerable judgment and reflect that there is still significant uncertainty

regarding numerous factors that may impact the ultimate loss levels, including, but not limited to: litigation

outcomes; court rulings; governmental enforcement decisions; future repurchase and indemnification claim

levels; securitization trustees pursuing mortgage repurchase litigation unilaterally or in coordination with

investors; investors successfully pursuing repurchase litigation independently and without the involvement of the

trustee as a party; ultimate repurchase and indemnification rates; future mortgage loan performance levels; actual

recoveries on the collateral; and macroeconomic conditions (including unemployment levels and housing prices).

In light of the significant uncertainty as to the ultimate liability our subsidiaries may incur from these matters, an

adverse outcome in one or more of these matters could be material to our results of operations or cash flows for

any particular reporting period.

Litigation

In accordance with the current accounting standards for loss contingencies, we establish reserves for litigation

related matters when it is probable that a loss associated with a claim or proceeding has been incurred and the

amount of the loss can be reasonably estimated. Litigation claims and proceedings of all types are subject to

many uncertain factors that generally cannot be predicted with assurance. Below we provide a description of

material legal proceedings and claims.

For some of the matters disclosed below, we are able to determine estimates of potential future outcomes that are

not probable and reasonably estimable outcomes justifying either the establishment of a reserve or an incremental

reserve build, but which are reasonably possible outcomes. For other disclosed matters, such an estimate is not

possible at this time. For those matters below where an estimate is possible (excluding the reasonably possible

future losses relating to the U.S. Bank Litigation, the DBSP Litigation, the Ambac Litigation, the FHFA

Litigation, the LXS Trust Litigation and the FHLB of Boston Litigation, because reasonably possible losses with

respect to those litigations are included within the reasonably possible representation and warranty liabilities

discussed above) management currently estimates the reasonably possible future losses could be approximately

$250 million. Notwithstanding our attempt to estimate a reasonably possible range of loss beyond our current

accrual levels for some litigation matters based on current information, it is possible that actual future losses will

exceed both the current accrual level and the range of reasonably possible losses disclosed here. Given the

inherent uncertainties involved in these matters, and the very large or indeterminate damages sought in some of

these matters, there is significant uncertainty as to the ultimate liability we may incur from these litigation

matters and an adverse outcome in one or more of these matters could be material to our results of operations or

cash flows for any particular reporting period.

253