Capital One 2013 Annual Report Download - page 114

Download and view the complete annual report

Please find page 114 of the 2013 Capital One annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

|

|

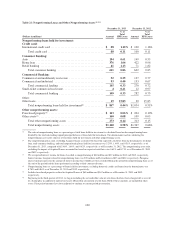

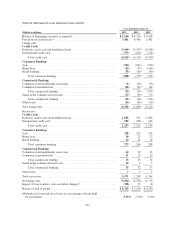

Primary Loan Products

We provide a variety of lending products. Our primary products include credit cards, auto loans, home loans and

commercial loans.

•Credit cards: We originate both prime and subprime credit cards through a variety of channels. Our credit

cards generally have variable interest rates. Credit card accounts are underwritten using an automated

underwriting system based on predictive models that we have developed. The underwriting criteria, which

are customized for individual products and marketing programs, are established based on an analysis of the

net present value of expected revenues, expenses and losses, subject to a further analysis using a variety of

stress conditions. Underwriting decisions are generally based on credit bureau information, including

payment history, debt burden and credit scores, such as FICO, and on other factors, such as applicant

income. We maintain a credit card securitization program and selectively sell charged-off credit card loans.

Prior to February 1, 2013, we had not securitized any credit card loans since 2009.

•Auto loans: We originate both prime and subprime auto loans. Customers are acquired through a network of

auto dealers and direct marketing. Our auto loans generally have fixed interest rates and loan terms of 72

months or less. Loan size limits are customized by program and are generally less than $75,000. Similar to

credit card accounts, the underwriting criteria are customized for individual products and marketing

programs and based on analysis of net present value of expected revenues, expenses and losses, subject to

maintaining resilience under a variety of stress conditions. Underwriting decisions are generally based on an

applicant’s income, estimated debt-to-income ratio, and credit bureau information, along with collateral

characteristics such as loan-to-value (“LTV”) ratio. We generally retain all of our auto loans, though we

have securitized auto loans and sold charged-off auto loans in the past and may do so in the future.

•Home loans: Most of the existing home loans in our loan portfolio were originated by banks we acquired.

The underwriting standards for these loans were less restrictive than our current underwriting standards.

Currently, we originate residential mortgage and home equity loans through our branches, direct marketing,

and dedicated home loan officers. Our home loan products include conforming and non-conforming fixed

rate and adjustable rate mortgage loans, as well as first and second lien home equity loans and lines of

credit. In general, our underwriting policy limits for these loans include: (1) a maximum LTV ratio of 80%

for loans without mortgage insurance; (2) a maximum LTV ratio of 95% for loans with mortgage insurance

or for home equity products; (3) a maximum debt-to-income ratio of 50%; and (4) a maximum loan amount

of $3.0 million. Our underwriting procedures are intended to verify the income of applicants and obtain

appraisals to determine home values. We may, in limited instances, use automated valuation models to

determine home values. Our underwriting standards for conforming loans are designed to meet the

underwriting standards required by the agencies at a minimum, and we sell most of our conforming loans to

the agencies. We generally retain non-conforming mortgages and home equity loans and lines of credit.

•Commercial loans. We offer a range of commercial lending products, including loans secured by

commercial real estate and loans to middle market industrial and service companies. Our commercial loans

may have a fixed or variable interest rate; however, the majority of our commercial loans have variable

rates. Our underwriting standards require an analysis of the borrower’s financial condition and prospects, as

well as an assessment of the industry in which the borrower operates. Where relevant, we evaluate and

appraise underlying collateral and guarantees. We maintain underwriting guidelines and limits for major

types of borrowers and loan products that specify, where applicable, guidelines for debt service coverage,

leverage, LTV ratio and standard covenants and conditions. We assign a risk rating and establish a

monitoring schedule for loans based on the risk profile of the borrower, industry segment, source of

repayment, the underlying collateral and guarantees (if any) and current market conditions. Although we

generally retain commercial loans, we may syndicate large positions for risk mitigation purposes. In

addition, we have sold impaired commercial loans in the past and may do so in the future.

94