Capital One 2013 Annual Report Download - page 7

Download and view the complete annual report

Please find page 7 of the 2013 Capital One annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

|

|

5

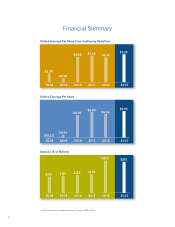

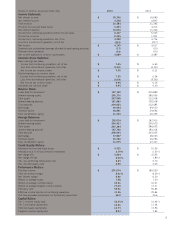

profitable growth and is now one of the four largest bank auto lenders in the

nation. New loan originations were about $17.4 billion in 2013 compared to

$16.0 billion in 2012. Credit losses increased modestly, as expected, but

remain low by historical standards. The charge-off rate in 2013 was 1.85%

compared to 1.66% in 2012. We expect that increased competition will

continue to have negative effects on margins, credit, and returns in

2014, but we still expect solid overall profitability and attractive returns

in the auto finance business.

Profitability in the home loans business improved in 2013,

driven by favorable credit trends. Actual credit losses are

trending better than the lifetime losses we estimated at the

time of the acquisitions. This outperformance flows into net

income over the life of the loans.

Planned run-off of acquired mortgage portfolios continues

as customers refinance or pay down their loans. The 2013

run-off was roughly $9 billion and we expect another $4 billion

in 2014. We continue to invest to ensure that our originations

and servicing businesses are well-managed.

Our combined retail and direct banking business made

tremendous progress in lowering costs and improving

profitability. While balance, mix, customer experience, and cost

trends are improving, low interest rates are likely to continue to

pressure the economics of our retail deposit businesses even

if rates begin to rise in 2014.

The strong growth and attractive returns in our commercial

banking business continued in 2013. Despite ongoing pressure

on loan and deposit margins, overall revenue rose by 10%,

while loan growth was 16%. Net income of $769 million was down

from 2012, when we recorded significant allowance releases.

Commercial credit performance was resilient throughout the

Great Recession and continued to improve in 2013. While the

year-end charge-off rate of 3 basis points is unsustainably low,

we continue to see low levels of non-performing and criticized

loan balances, so we expect credit performance to remain

strong. Our investments to build industry and product specialization

have paid off and position the commercial banking business for

continued success in 2014.

Vacation Ownership

Products and services offered by Capital One, N.A., member FDIC. © 2013 Capital One. All rights reserved.

When your vision needs financing, count on Capital One® to step up with

creative solutions. With over 100 years of combined experience, plus the

resources of a top-10 U.S. bank, our timeshare experts can help turn your

dream into reality with the expertise, insight, and financing you need.

James Casey

james.casey@capitalone.com

(860) 348-8861

capitalonecommercial.com

Michael Szwajkowski

michael.szwajkowski@capitalone.com

(21 2 ) 8 3 4 -1101

Capital One’s commercial

bankers are doing more for

their customers. They know

banking through and through,

and they’re also specialists in

the industries they serve. They

think long term. They care about

relationships. And they’re

focused on helping their

customers grow and stay

in excellent financial shape.