Capital One 2013 Annual Report Download - page 174

Download and view the complete annual report

Please find page 174 of the 2013 Capital One annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

164 -

165

165 -

166

166 -

167

167 -

168

168 -

169

169 -

170

170 -

171

171 -

172

172 -

173

173 -

174

174 -

175

175 -

176

176 -

177

177 -

178

178 -

179

179 -

180

180 -

181

181 -

182

182 -

183

183 -

184

184 -

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

|

|

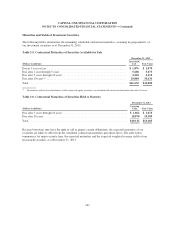

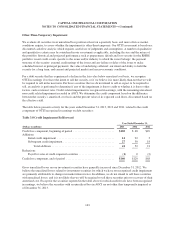

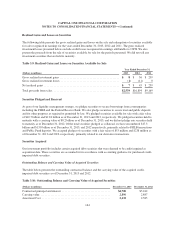

CAPITAL ONE FINANCIAL CORPORATION

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS—(Continued)

unobservable. Fair value measurement of a financial asset or liability is assigned to a level based on the lowest

level of any input that is significant to the fair value measurement in its entirety. The three levels of the fair value

hierarchy are described below:

Level 1: Quoted prices (unadjusted) in active markets for identical assets or liabilities

Level 2: Observable market-based inputs, other than quoted prices in active markets for identical assets or

liabilities

Level 3: Unobservable inputs

The accounting guidance for fair value requires that we maximize the use of observable inputs and minimize the

use of unobservable inputs in determining fair value. Accounting guidance provides for the irrevocable option to

elect, on a contract-by-contract basis, to measure certain financial assets and liabilities at fair value at inception

of the contract and record any subsequent changes in fair value into earnings. We have not made any material fair

value option elections as of and for the years ended December 31, 2013, 2012 and 2011. See “Note 18—Fair

Value of Financial Instruments” for additional information.

Accounting for Acquisitions

We account for business combinations under the acquisition method of accounting. Under the acquisition

method, tangible and intangible identifiable assets acquired, liabilities assumed and any noncontrolling interest in

the acquiree are recorded at fair value as of the acquisition date, with limited exceptions. Transaction costs and

costs to restructure the acquired company are expensed as incurred. Goodwill is recognized as the excess of the

acquisition price over the estimated fair value of the net assets acquired. Likewise, if the fair value of the net

assets acquired is greater than the acquisition price, a bargain purchase gain is recognized and recorded in non-

interest income.

If the acquired set of activities and assets does not meet the accounting definition of a business, the transaction is

accounted for as an asset acquisition. In an asset acquisition, the assets acquired are recorded at the purchase

price plus any transaction costs incurred and, therefore, no goodwill is recognized.

Accounting Standards Adopted in 2013

New Benchmark Interest Rate for Hedge Accounting Purposes

In July 2013, the Financial Accounting Standards Board (“FASB”) issued guidance permitting the use of the Fed

Funds Effective Swap Rate (or Overnight Index Swap Rate, “OIS”) as a benchmark interest rate for hedge

accounting purposes. The addition of OIS expands the number of benchmark interest rates to three, including the

US Treasury rate and London Interbank Offered Rate swap rate. The guidance also removes the previous

restriction on using different benchmark rates for similar hedges. The guidance is effective for qualifying new or

redesignated hedging relationships entered into on or after July 17, 2013. See “Note 10—Derivative Instruments

and Hedging Activities” for further details regarding the impact derivative contracts designated as qualifying

accounting hedges have on our financial condition and results of operations.

Comprehensive Income: Reporting of Amounts Reclassified Out of Accumulated Other Comprehensive

Income

In February 2013, the FASB issued new guidance requiring an entity to report the effect of significant

reclassifications out of accumulated other comprehensive income on the respective line items in net income if the

amount being reclassified is required under U.S. GAAP to be reclassified in its entirety to net income. The new

154