Capital One 2013 Annual Report Download - page 66

Download and view the complete annual report

Please find page 66 of the 2013 Capital One annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

|

|

income from continuing operations of $1.1 billion was driven by the absence in 2013 of the provision for

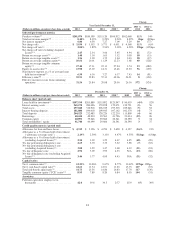

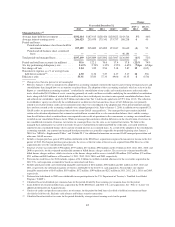

credit losses of $1.2 billion to establish an allowance for the credit card receivables acquired in the 2012

U.S. card acquisition and the absence in 2013 of the $174 million charge to establish a reserve for estimated

uncollectible billed finance charges and fees related to those loans, both of which were recorded in 2012.

The improvement also reflects higher revenue attributable to the 2012 U.S. card acquisition coupled with

increased purchase volume in our Credit Card business. The increase in net revenues was partially offset by

higher operating expenses resulting from the 2012 U.S. card acquisition. Period-end loans held for

investment in our Credit Card business decreased by $10.5 billion to $81.3 billion as of December 31, 2013

from $91.8 billion as of December 31, 2012. The decrease was largely due to the Portfolio Sale and

continued run-off of our installment loan portfolio and certain other credit card loans acquired in the 2012

U.S. card acquisition.

•Consumer Banking: Our Consumer Banking business generated net income from continuing operations of

$1.5 billion in 2013, compared with net income from continuing operations of $1.4 billion in 2012. The

modest increase in net income is due to higher interest income related to growth in average interest earning

assets in auto partially offset by the run-off of home loans. Period-end loans held for investment in our

Consumer Banking business decreased by $4.3 billion, or 6%, to $70.8 billion as of December 31, 2013,

from $75.1 billion as of December 31, 2012, due to the run-off of acquired home loans partially offset by

strong auto loan originations.

•Commercial Banking: Our Commercial Banking business generated net income from continuing operations

of $769 million in 2013, compared with net income from continuing operations of $835 million in 2012.

The decrease in net income of $66 million is due to a higher provision for credit losses. The higher

provision for credit losses was driven by lower allowance releases, which was partially offset by loan

growth in 2013 compared to the prior year. This was partially offset by higher revenues due to growth in

commercial real estate and commercial and industrial loans and higher deposit balances and fee-based

product and services revenue. Period-end loans held for investment in our Commercial Banking business

increased by $6.2 billion, or 16%, to $45.0 billion as of December 31, 2013, from $38.8 billion as of

December 31, 2012. The increase was driven by strong loan originations in the commercial and industrial

and commercial real estate businesses, which were partially offset by the continued run-off of the small-

ticket commercial real estate loan portfolio.

Business Outlook

We discuss below our current expectations regarding our total company performance and the performance of

each of our business segments over the near-term based on market conditions, the regulatory environment and

our business strategies as of the time we filed this Annual Report on Form 10-K. The statements contained in this

section are based on our current expectations regarding our outlook for our financial results and business

strategies. Our expectations take into account, and should be read in conjunction with, our expectations regarding

economic trends and analysis of our business as discussed in “Part I—Item 1. Business” and “Part II—Item 7.

MD&A” of this Report. Certain statements are forward-looking statements within the meaning of the Private

Securities Litigation Reform Act of 1995. Actual results could differ materially from those in our forward-

looking statements. Except as otherwise disclosed, forward-looking statements do not reflect: (i) any change in

current dividend or repurchase strategies, (ii) the effect of any acquisitions, divestitures or similar transactions

that have not been previously disclosed, or (iii) any changes in laws, regulations or regulatory interpretations, in

each case after the date as of which such statements are made. See “Part I—Item 1. Business—Forward-Looking

Statements” for more information on the forward-looking statements in this Report and “Part I—Item 1A. Risk

Factors” in this Report for factors that could materially influence our results.

Total Company Expectations

Our strategies and actions are designed to deliver and sustain strong returns and capital generation through the

acquisition and retention of franchise-enhancing customer relationships across our businesses. We believe that

46