Capital One 2013 Annual Report Download - page 175

Download and view the complete annual report

Please find page 175 of the 2013 Capital One annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

165 -

166

166 -

167

167 -

168

168 -

169

169 -

170

170 -

171

171 -

172

172 -

173

173 -

174

174 -

175

175 -

176

176 -

177

177 -

178

178 -

179

179 -

180

180 -

181

181 -

182

182 -

183

183 -

184

184 -

185

185 -

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

|

|

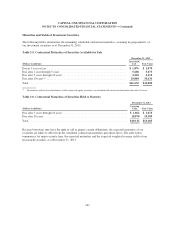

CAPITAL ONE FINANCIAL CORPORATION

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS—(Continued)

guidance does not change the items which must be reported in other comprehensive income, how such items are

measured or when they must be reclassified from other comprehensive income to net income. The guidance was

effective for reporting periods beginning after December 15, 2012. Our adoption of the guidance on January 1,

2013 had no impact on our financial condition, results of operations or liquidity as it only affects our disclosures.

See “Note 11—Stockholders’ Equity” for further details.

Offsetting Financial Assets and Liabilities

Effective January, 2013, we were required to disclose both gross and net information about instruments and

transactions eligible for offset on the balance sheet as well as instruments and transactions subject to an

agreement similar to a master netting arrangement. The disclosures are required irrespective of whether such

instruments are presented gross or net on the balance sheet. The guidance was effective for annual and interim

reporting periods beginning on or after January 1, 2013, with comparative retrospective disclosures required for

all periods presented. Our adoption of the guidance had no effect on our financial condition, results of operations

or liquidity as it only affects our disclosures. See “Note 10—Derivative Instruments and Hedging Activities” for

further details.

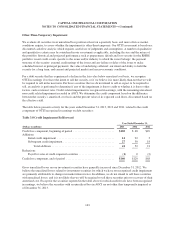

Recently Issued but Not Yet Adopted Accounting Standards

Obligations Resulting from Joint and Several Liability Arrangements

In February 2013, the FASB issued guidance for the recognition, measurement, and disclosure of obligations

resulting from joint and several liability arrangements for which the total amount of the obligation, within the

scope of this guidance, is fixed at the reporting date, except for obligations addressed within existing guidance in

U.S. GAAP. The guidance clarifies that an entity shall measure obligations as the sum of the amount the

reporting entity agreed to pay on the basis of its arrangement among its co-obligors and any additional amount

the reporting entity expects to pay on behalf of its co-obligors. The guidance also requires an entity to disclose

the nature and amount of the obligation as well as other information about those obligations. The guidance is

effective for annual and interim periods beginning after December 15, 2013, with early adoption permitted. We

do not expect our adoption of this guidance in the first quarter of 2014 to have a significant effect on our

financial condition, results of operations or liquidity as the guidance is consistent with our current practice.

Reclassification of Collateralized Mortgage Loan Upon Foreclosure

In January 2014, the FASB issued guidance clarifying when an entity should reclassify a consumer mortgage

loan collateralized by residential real estate to foreclosed property. Reclassification should occur when the

creditor obtains legal title to the residential real estate property or when the borrower conveys all interest in the

residential real estate property to the creditor to satisfy that loan through completion of a deed in lieu of

foreclosure or through a similar legal agreement. An entity should not wait until a redemption period, if any, has

expired to reclassify a consumer mortgage loan to foreclosed property. The guidance is effective for annual and

interim periods beginning after December 15, 2014, with early adoption permitted. We do not expect our

adoption of this guidance in the first quarter of 2015 to have a significant effect on our financial condition, results

of operations or liquidity as the guidance is materially consistent with our current practice.

Accounting for Investments in Qualified Affordable Housing Projects

In January 2014, the FASB issued guidance permitting an entity to account for investments in qualified

affordable housing projects using the proportional amortization method if certain criteria are met. The

155