Capital One 2013 Annual Report Download - page 261

Download and view the complete annual report

Please find page 261 of the 2013 Capital One annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

251 -

252

252 -

253

253 -

254

254 -

255

255 -

256

256 -

257

257 -

258

258 -

259

259 -

260

260 -

261

261 -

262

262 -

263

263 -

264

264 -

265

265 -

266

266 -

267

267 -

268

268 -

269

269 -

270

270 -

271

271 -

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

|

|

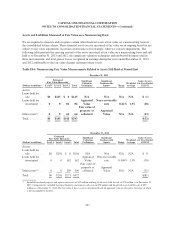

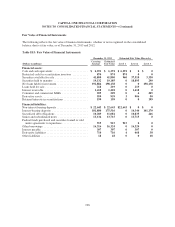

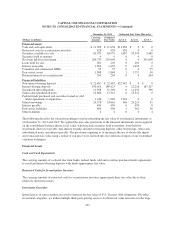

CAPITAL ONE FINANCIAL CORPORATION

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS—(Continued)

Net Loans Held For Investment

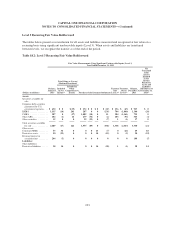

Loans held for investment that are individually impaired are carried at the lower of cost or fair value of the

underlying collateral, less the estimated cost to sell. The fair values of credit card loans, installment loans, auto

loans, home loans and commercial loans were estimated using a discounted cash flow method, a form of the

income approach. Discount rates were determined considering rates at which similar portfolios of loans would be

made under current conditions and considering liquidity spreads applicable to each loan portfolio based on the

secondary market. The fair value of credit card loans excluded any value related to customer account

relationships.

Due to the use of unobservable inputs, loans held for investment are classified as Level 3 under the fair value

hierarchy. Fair value adjustments for loans held for investment are recorded in provision for credit losses in the

consolidated statement of income. The fair value of these loans as of December 31, 2013 remained substantially

unchanged compared to the previous year as the impact of higher market rates was offset by improved credit

performance in our card, mortgage and commercial loan portfolios.

Interest Receivable

The carrying amount of interest receivable approximates the fair value of this asset due to its relatively

short-term nature.

Derivative Assets and Liabilities

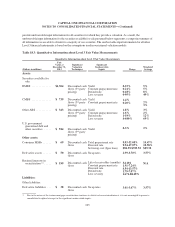

We use both exchange-traded derivatives and over-the-counter (“OTC”) derivatives to manage our interest rate

and foreign currency risk exposure. Quoted market prices are available and used for our exchange-traded

derivatives, which we classify as Level 1. However, substantially all of our derivatives are traded in OTC

markets where quoted market prices are not always readily available. Therefore, we value most OTC derivatives

using valuation techniques, which include internally-developed models. We primarily rely on market observable

inputs for our models, such as interest rate yield curves, credit curves, option volatility and currency rates, that

vary depending on the type of derivative and nature of the underlying rate, price or index upon which the

derivative’s value is based. Where model inputs can be observed in a liquid market and the model does not

require significant judgment, such derivatives are typically classified as Level 2 of the fair value hierarchy. When

instruments are traded in less liquid markets and significant inputs are unobservable, such as interest rate swaps

whose remaining terms do not correlate with market observable interest rate yield curves, the derivatives are

classified as Level 3.

The impact of counterparty non-performance risk is considered when measuring the fair value of derivative

assets. These derivatives are included in other assets on the balance sheet.

We validate the pricing obtained from the internal models through comparison of pricing to additional sources,

including external valuation agents and other internal sources. Pricing variances among different pricing sources

are analyzed and validated.

Mortgage Servicing Rights

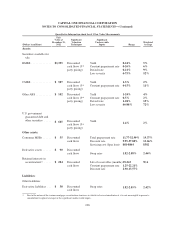

We record consumer MSRs at fair value on a recurring basis, while commercial MSRs are subsequently

measured at amortized cost with impairment recognized as a reduction in other non-interest income. MSRs do

not trade in an active market with readily observable prices. Accordingly, we determine the fair value of MSRs

using a valuation model that calculates the present value of estimated future net servicing income. The model

241