Capital One 2013 Annual Report Download - page 186

Download and view the complete annual report

Please find page 186 of the 2013 Capital One annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

176 -

177

177 -

178

178 -

179

179 -

180

180 -

181

181 -

182

182 -

183

183 -

184

184 -

185

185 -

186

186 -

187

187 -

188

188 -

189

189 -

190

190 -

191

191 -

192

192 -

193

193 -

194

194 -

195

195 -

196

196 -

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

|

|

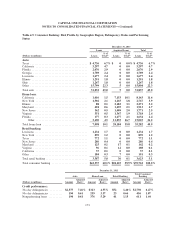

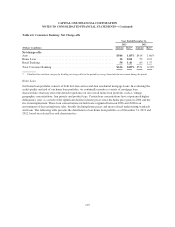

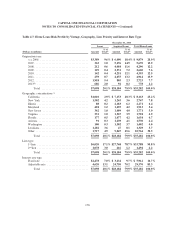

CAPITAL ONE FINANCIAL CORPORATION

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS—(Continued)

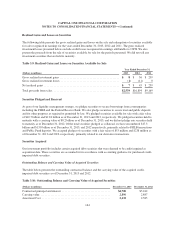

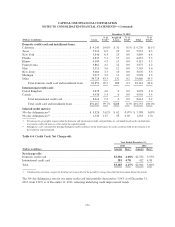

losses. Probable and significant increases in expected cash flows would first reverse any previously recorded

allowance for loan and lease losses established subsequent to acquisition, with any remaining increase in

expected cash flows recognized prospectively in interest income over the remaining estimated life of the

underlying loans. We reduced the allowance and provision for credit losses by $19 million for the year ended

December 31, 2013 and increased the allowance and provision for credit losses by $31 million for the year ended

December 31, 2012 related to certain pools of Acquired Loans. The allowance on Acquired Loans totaled $38

million and $57 million as of December 31, 2013 and 2012, respectively. The credit performance of the

remaining pools has generally been more favorable than expected, which has resulted in the reclassification of

amounts from the nonaccretable difference to the accretable yield.

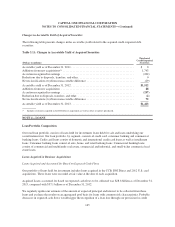

Loans Acquired and Accounted for Based on Contractual Cash Flows

Of the loans acquired in the 2012 U.S. card acquisition, at acquisition there were $26.2 billion of loans

designated as held for investment that had revolving privileges at acquisition and were, therefore, accounted for

based on contractual cash flows. These loans were recorded at a fair value of $26.9 billion, resulting in a net

premium of $705 million at acquisition. We are required to amortize the $705 million net premium as an

adjustment to interest income over the remaining life of the loans. Given the guidance applicable to purchased

revolving loans, it was necessary to record an allowance through provision for credit losses to properly recognize

an estimate of incurred losses on the existing principal balances. At acquisition, we recorded a provision for

credit losses of $1.2 billion to establish an initial allowance primarily related to these loans. The allowance was

calculated using the same methodology utilized for determining the allowance for our existing credit card

portfolio. The provision for credit losses of $1.2 billion is included in the total provision for credit losses of $4.4

billion recorded during 2012 as indicated in “Note 5—Allowance for Loan and Lease Losses”.

Excluded from the amounts above were purchased revolving loans from the 2012 U.S. card acquisition with a

fair value of $471 million that we designated as held for sale at acquisition. We closed on the sale of these

receivables in the third quarter of 2012.

166