Capital One 2013 Annual Report Download - page 68

Download and view the complete annual report

Please find page 68 of the 2013 Capital One annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

|

|

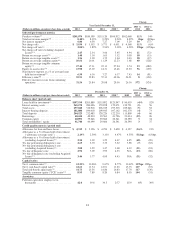

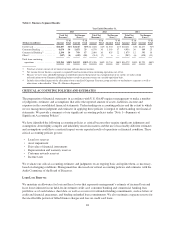

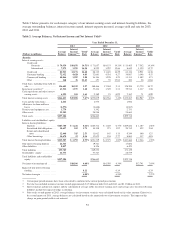

Table 1: Business Segment Results

Year Ended December 31,

2013 2012 2011

Total Net

Revenue(1)

Net Income

(Loss)(2)

Total Net

Revenue(1)

Net Income

(Loss)(2)

Total Net

Revenue(1)

Net Income

(Loss)(2)

(Dollars in millions) Amount

% of

Total Amount

% of

Total Amount

% of

Total Amount

% of

Total Amount

% of

Total Amount

% of

Total

Credit Card .................. $14,287 64% $2,615 60% $13,260 62% $1,530 41% $10,431 64% $2,277 70%

Consumer Banking ............ 6,654 30 1,451 33 6,570 30 1,363 37 4,956 30 809 25

Commercial Banking(3) ......... 2,290 10 769 17 2,080 10 835 22 1,879 12 595 18

Other(4) ..................... (847) (4) (443) (10) (514) (2) 6 — (987) (6) (428) (13)

Total from continuing

operations ................. $22,384 100% $4,392 100% $21,396 100% $3,734 100% $16,279 100% $3,253 100%

(1) Total net revenue consists of net interest income and non-interest income.

(2) Net income for our business segments is reported based on income from continuing operations, net of tax.

(3) Because we have some affordable housing tax-related investments that generate tax-exempt income or tax credits, we make certain

reclassifications to our Commercial Banking business results to present revenues on a taxable-equivalent basis.

(4) Includes the residual impact of the allocation of our centralized Corporate Treasury group activities to our business segments as well as

other items as described in “Note 19—Business Segments”.

CRITICAL ACCOUNTING POLICIES AND ESTIMATES

The preparation of financial statements in accordance with U.S. GAAP requires management to make a number

of judgments, estimates and assumptions that affect the reported amount of assets, liabilities, income and

expenses in the consolidated financial statements. Understanding our accounting policies and the extent to which

we use management judgment and estimates in applying these policies is integral to understanding our financial

statements. We provide a summary of our significant accounting policies under “Note 1—Summary of

Significant Accounting Policies”.

We have identified the following accounting policies as critical because they require significant judgments and

assumptions about highly complex and inherently uncertain matters and the use of reasonably different estimates

and assumptions could have a material impact on our reported results of operations or financial condition. These

critical accounting policies govern:

• Loan loss reserves

• Asset impairment

• Fair value of financial instruments

• Representation and warranty reserves

• Customer rewards reserves

• Income taxes

We evaluate our critical accounting estimates and judgments on an ongoing basis and update them, as necessary,

based on changing conditions. Management has discussed our critical accounting policies and estimates with the

Audit Committee of the Board of Directors.

Loan Loss Reserves

We maintain an allowance for loan and lease losses that represents management’s estimate of incurred loan and

lease losses inherent in our held-for-investment credit card, consumer banking and commercial banking loan

portfolios as of each balance sheet date, as well as a reserve for unfunded lending commitments, such as letters of

credit and financial guarantees, and binding unfunded loan commitments. We also maintain a separate reserve for

the uncollectible portion of billed finance charges and fees on credit card loans.

48