Capital One 2013 Annual Report Download - page 116

Download and view the complete annual report

Please find page 116 of the 2013 Capital One annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

|

|

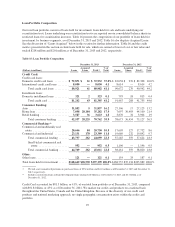

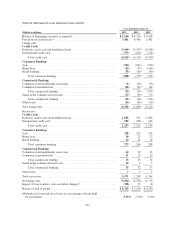

Consumer Banking accounted for $70.8 billion, or 36%, of our loan portfolio as of December 31, 2013,

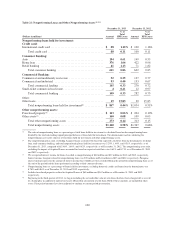

compared with $75.1 billion, or 37%, of our loan portfolio as of December 31, 2012. The auto portfolio is

originated primarily on a national basis, with additional originations through our retail branch network. The

home loan portfolio is concentrated in California, New York, Illinois, Maryland, New Jersey, Virginia, and

Florida which reflects the characteristics of the ING Direct portfolio that comprises the majority of our home

loans. Retail banking includes small business loans and other consumer lending products originated through our

branch network.

Commercial Banking represented $45.0 billion, or 23%, of our loan portfolio as of December 31, 2013,

compared with $38.8 billion, or 19%, as of December 31, 2012. We operate our Commercial Banking business

primarily in geographic regions where we maintain retail bank branches. Accordingly, the portfolio is

concentrated in New York, Louisiana and Texas, which represent our largest retail banking markets. Our small-

ticket commercial real estate portfolio, which was originated on a national basis through a broker network, is in a

run-off mode.

We provide additional information on the geographic concentration, by loan category, of our loan portfolio in

“Note 4—Loans.”

Loans Acquired in Business Acquisitions

As noted above, our portfolio of loans held for investment includes loans acquired in the CCB, ING Direct and

2012 U.S. card acquisitions. These loans were recorded at fair value as of the date of each acquisition. We elect

to account for purchased loans using the guidance for accounting for purchased credit-impaired loans, which is

based on expected cash flows, unless specifically scoped out of the guidance.

See “Note 1—Summary of Significant Accounting Policies—Loans” for additional information on our

accounting for loans, including purchased loans. See “Note 4—Loans” and “Note 5—Allowance for Loan and

Lease Losses” for additional information on the credit quality of our loan portfolio.

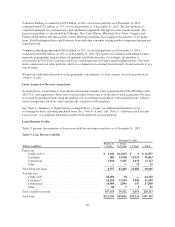

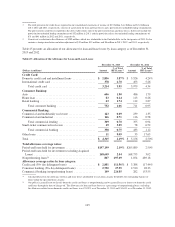

Loan Maturity Profile

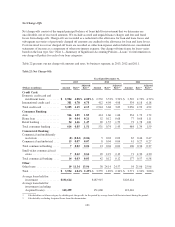

Table 17 presents the maturities of loans in our held-for-investment portfolio as of December 31, 2013.

Table 17: Loan Maturity Schedule

December 31, 2013

(Dollars in millions)

Due Up to

1 Year

> 1 Year

to 5 Years > 5 Years Total

Fixed rate:

Credit card(1)(2) ...................................... $ 2,841 $14,025 $ 9 $ 16,875

Consumer .......................................... 682 23,968 14,413 39,063

Commercial ........................................ 1,034 5,456 6,633 13,123

Other .............................................. — — 25 25

Total fixed-rate loans ..................................... 4,557 43,449 21,080 69,086

Variable rate:

Credit card(1) ........................................ 64,400 30 — 64,430

Consumer(3) ......................................... 14,260 13,539 3,900 31,699

Commercial ........................................ 28,885 2,856 147 31,888

Other .............................................. 80 7 9 96

Total variable-rate loans ................................... 107,625 16,432 4,056 128,113

Total loans ............................................. $112,182 $59,881 $25,136 $197,199

96