Capital One 2013 Annual Report Download - page 102

Download and view the complete annual report

Please find page 102 of the 2013 Capital One annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

|

|

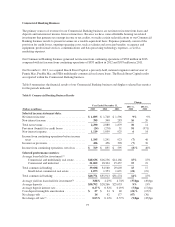

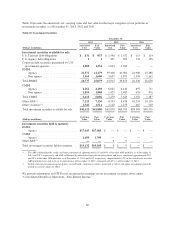

Period-end loans held for investment decreased by $8.7 billion, or 4%, in 2013, to $197.2 billion as of

December 31, 2013, from $205.9 billion as of December 31, 2012. The decrease was due in part to the transfer of

the Best Buy loan portfolio of $7 billion at the date of transfer to the loans held for sale in the first quarter of

2013, which were further sold in the third quarter of 2013. In addition to the Portfolio Sale, period-end loans held

for investment decreased due to expected run-off of certain other credit card loans acquired in the 2012 U.S. card

acquisition and continued expected run-off of installment loans in our Credit Card business and home loans in

our Consumer Banking business. The paydowns and run-off of card balances were partially offset by growth in

certain segments of our Credit Card business, higher period-end auto loan balances due to the continued high

volume of auto loan originations and strong loan originations in our commercial and industrial and commercial

real estate loan portfolios.

We provide additional information on the composition of our loan portfolio and credit quality below in “Credit

Risk Profile” and in “Note 4—Loans.”

Loans Held for Sale

Loans held for sale, which are carried at lower of cost or fair value, increased to $218 million as of December 31,

2013, from $201 million as of December 31, 2012. We provide additional information for loans held for sale in

“Note 4—Loans.”

Customer Deposits

Our customer deposits have become our largest source of funding for our operations, providing a sizable and

consistent source of low-cost funds. Total customer deposits decreased by $8.0 billion to $204.5 billion as of

December 31, 2013, from $212.5 billion as of December 31, 2012, reflecting our scaling back of deposit growth

in the current environment of relatively low overall loan growth. We provide information on the composition of

our deposits, average outstanding balances, interest expense and yield below in “Liquidity Risk Profile.”

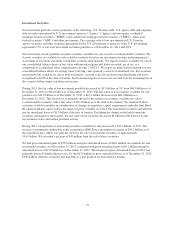

Securitized Debt Obligations

Securitization debt obligations decreased by $1.1 billion during 2013 to $10.3 billion as of December 31, 2013,

from $11.4 billion as of December 31, 2012. The decrease was driven by maturities and repurchases totaling

$3.3 billion, partially offset by the issuance of $2.2 billion of credit card securitization debt during 2013.

Other Debt

Other debt, which consists of federal funds purchased and securities loaned or sold under agreements to

repurchase, senior and subordinated notes and other borrowings, including Federal Home Loan Bank (“FHLB”)

advances, but excluding securitized debt obligations, totaled $30.4 billion as of December 31, 2013, of which

$16.2 billion represented short-term borrowings and $14.2 billion represented long-term debt. Other debt

decreased by $8.1 billion in 2013 from a total of $38.5 billion as of December 31, 2012, of which $21.1 billion

represented short-term borrowings and $17.4 billion represented long-term borrowings.

The decrease in other debt was primarily attributable to our redemption of $3.65 billion junior subordinated debt

in connection with our redemption of outstanding trust preferred securities in the first quarter of 2013, as well as

net maturities of FHLB advances of $4.6 billion during 2013. The above decreases were partially offset by the

issuance of $2.0 billion unsecured senior notes during 2013. We provide additional information on our

borrowings in “Note 9—Deposits and Borrowings.”

82