Capital One 2013 Annual Report Download - page 232

Download and view the complete annual report

Please find page 232 of the 2013 Capital One annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

222 -

223

223 -

224

224 -

225

225 -

226

226 -

227

227 -

228

228 -

229

229 -

230

230 -

231

231 -

232

232 -

233

233 -

234

234 -

235

235 -

236

236 -

237

237 -

238

238 -

239

239 -

240

240 -

241

241 -

242

242 -

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

|

|

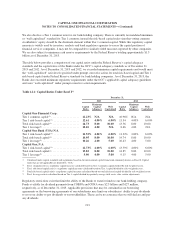

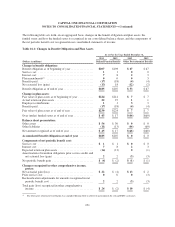

CAPITAL ONE FINANCIAL CORPORATION

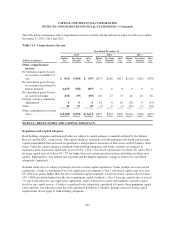

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS—(Continued)

The table below summarizes other comprehensive income activity and the related tax impact for the years ended

December 31, 2013, 2012 and 2011:

Table 11.3: Comprehensive Income

Year Ended December 31,

2013 2012 2011

(Dollars in millions)

Before

Tax

Provision

(Benefit)

After

Tax

Before

Tax

Provision

(Benefit)

After

Tax

Before

Tax

Provision

(Benefit)

After

Tax

Other comprehensive

income:

Net unrealized gains (losses)

on securities available for

sale ................... $ (961) $(364) $ (597) $673 $256 $417 $(119) $(41) $(78)

Net unrealized gains (losses)

on securities transferred to

held to maturity ......... (1,435) (538) (897) 0 0 00 0 0

Net unrealized gains (losses)

on cash flow hedges ...... (250) (95) (155) 120 47 73 44 18 26

Foreign currency translation

adjustments ............ 80 881 0 81 (13) 0 (13)

Other ................... 49 19 30 (1) 0 (1) (21) (7) (14)

Other comprehensive income

(loss) .................. $(2,589) $(978) $(1,611) $873 $303 $570 $(109) $(30) $(79)

NOTE 12—REGULATORY AND CAPITAL ADEQUACY

Regulation and Capital Adequacy

Bank holding companies and national banks are subject to capital adequacy standards adopted by the Federal

Reserve and the OCC, respectively. The capital adequacy standards set forth minimum risk-based and leverage

capital requirements that are based on quantitative and qualitative measures of their assets and off-balance sheet

items. Under the capital adequacy standards, bank holding companies and banks currently are required to

maintain a total risk-based capital ratio of at least 8%, a Tier 1 risk-based capital ratio of at least 4%, and a Tier 1

leverage capital ratio of at least 4% (3% for banks that meet certain specified criteria, including excellent asset

quality, high liquidity, low interest rate exposure and the highest regulatory rating) in order to be considered

adequately capitalized.

National banks also are subject to prompt corrective action capital regulations. Under prompt corrective action

regulations, a bank is considered to be well capitalized if it maintains a Tier 1 risk-based capital ratio of at least

6% (200 basis points higher than the above minimum capital standard), a total risk-based capital ratio of at least

10% (200 basis points higher than the above minimum capital standard), a Tier 1 leverage capital ratio of at least

5% and is not subject to any supervisory agreement, order or directive to meet and maintain a specific capital

level for any capital reserve. A bank is considered to be adequately capitalized if it meets these minimum capital

ratios and does not otherwise meet the well capitalized definition. Currently, prompt corrective action capital

requirements do not apply to bank holding companies.

212