Capital One 2009 Annual Report Download - page 189

Download and view the complete annual report

Please find page 189 of the 2009 Capital One annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

179 -

180

180 -

181

181 -

182

182 -

183

183 -

184

184 -

185

185 -

186

186 -

187

187 -

188

188 -

189

189 -

190

190 -

191

191 -

192

192 -

193

193 -

194

194 -

195

195 -

196

196 -

197

197 -

198

198 -

199

199 -

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

|

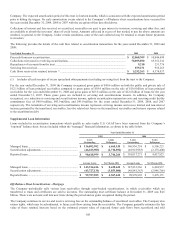

|

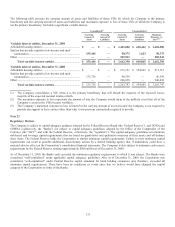

176

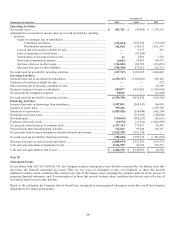

Regulatory

Filing

Basis

Ratios

Applying

Subprime

Guidance

Ratios Minimum for Capital

Adequacy Purposes

To Be “Well Capitalized”

Under

Prompt Corrective Action

Provisions

December 31, 2009

Capital One Financial Corp.(1)

Tier 1 Capital .......................................................

.

13.75% 13.04% 4.00% N/A

Total Capital ........................................................

.

17.70 16.85 8.00 N/A

Tier 1 Leverage ....................................................

.

10.28 10.28 4.00 N/A

Capital One Bank (USA) N.A.

Tier 1 Capital .......................................................

.

18.27% 14.67% 4.00% 6.00%

Total Capital ........................................................

.

26.40 21.41 8.00 10.00

Tier 1 Leverage ....................................................

.

13.03 13.03 4.00 5.00

Capital One, N.A.

Tier 1 Capital .......................................................

.

10.22% N/A 4.00% 6.00%

Total Capital ........................................................

.

11.46 N/A 8.00 10.00

Tier 1 Leverage ....................................................

.

7.42 N/A 4.00 5.00

December 31, 2008

Capital One Financial Corp.(1)

Tier 1 Capital .......................................................

.

13.81% 12.81% 4.00% N/A

Total Capital ........................................................

.

16.65 15.53 8.00 N/A

Tier 1 Leverage ....................................................

.

11.17 11.17 4.00 N/A

Capital One Bank (USA) N.A.

Tier 1 Capital .......................................................

.

13.02% 9.99% 4.00% 6.00%

Total Capital ........................................................

.

15.65 12.26 8.00 10.00

Tier 1 Leverage ....................................................

.

11.79 11.79 4.00 5.00

Capital One, N.A.

Tier 1 Capital .......................................................

.

10.50% N/A 4.00% 6.00%

Total Capital ........................................................

.

11.82 N/A 8.00 10.00

Tier 1 Leverage ....................................................

.

7.81 N/A 4.00 5.00

(1) The regulatory framework for prompt corrective action is not applicable for bank holding companies.

COBNA treats a portion of its loans as “subprime” under the Guidelines issued by the four federal banking agencies that comprise the

Federal Financial Institutions Examination Council (“FFIEC”), and has assessed its capital and allowance for loan and lease losses

accordingly. Under the Guidelines, COBNA exceeds the minimum capital adequacy guidelines as of December 31, 2009.

For purposes of the Guidelines, the Corporation has treated as subprime all loans in COBNA’s targeted “subprime” programs to

customers either with a FICO score of 660 or below or with no FICO score. COBNA holds on average 200% of the total risk-based

capital charge that would otherwise apply to such assets. This results in higher levels of regulatory capital at COBNA.

Additionally, regulatory restrictions exist that limit the ability of COBNA and CONA to transfer funds to the Corporation. As of

December 31, 2009, funds available for dividend payments from COBNA and CONA were $798.0 million and zero, respectively. The

funds of COBNA are available for payment as dividends to the Corporation without prior approval of the OCC while a dividend

payment by CONA would require prior approval of the OCC.

In December 2009, the OCC and the Federal Reserve announced a proposed rule regarding capital requirements related to the

adoption of ASU 2009-16 and ASU 2009-17. Under the proposal, the Company and its subsidiary banks will be required to hold

additional capital in relation to the consolidated assets and any associated creation of loan loss reserves. The rule provides for a phase-

in of the capital requirements in the form of an optional two-quarter delay in implementation, followed by an optional two-quarter

partial implementation. A final rule was ratified on January 21, 2010, with only minor amendments to the December proposal. See

“Note 1- Significant Accounting Policies” for the pro forma financial statement impacts.