Capital One 2009 Annual Report Download - page 174

Download and view the complete annual report

Please find page 174 of the 2009 Capital One annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

164 -

165

165 -

166

166 -

167

167 -

168

168 -

169

169 -

170

170 -

171

171 -

172

172 -

173

173 -

174

174 -

175

175 -

176

176 -

177

177 -

178

178 -

179

179 -

180

180 -

181

181 -

182

182 -

183

183 -

184

184 -

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

|

|

161

During 2009, the Company entered into interest rate swap agreements, also designated as fair value hedges that modify the

Company’s exposure to interest rate risk by effectively converting a portion of the Company’s brokered CD liabilities from fixed rate

to variable rates with maturities ranging from 2010 to 2018. The agreements involve the receipt of fixed rate amounts in exchange for

floating rate interest payments over the life of the agreement.

The Company has entered into forward exchange contracts to hedge foreign currency denominated investments against fluctuations in

exchange rates. The purpose of the Company’s foreign currency hedging activities is to protect the Company from the risk of adverse

effects of movements in exchange rates.

Cash Flow Hedges

The Company uses cash flow hedges to hedge the exposure to variability in the cash flows of a forecasted transaction. Changes in fair

value of derivatives designated as cash flow hedges are recognized in other comprehensive income, a separate component of

stockholders’ equity. The Company has entered into interest rate swap agreements, designated as cash flow hedges, that effectively

modify the Company’s exposure to interest rate risk by converting floating rate debt to a fixed rate debt with maturities ranging from

2010 to 2013. The agreements involve the receipt of floating rate amounts in exchange for fixed rate interest payments over the life of

the agreement.

The Company has also entered into interest rate swap agreements, designated as cash flow hedges, that effectively modify the

Company’s exposure to interest rate risk by converting floating rate assets to fixed rate assets, with maturities in 2013. The agreements

involve the receipt of fixed rate amounts in exchange for floating rate interest payments over the life of the agreements.

The Company has entered into forward exchange contracts to reduce the Company’s sensitivity to foreign currency exchange rate

changes on its foreign currency denominated loans. The forward rate agreements allow the Company to “lock-in” functional currency

equivalent cash flows associated with the foreign currency denominated loans.

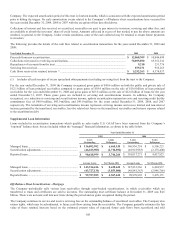

At December 31, 2009, the Company expects to reclassify $25.8 million of net losses, after tax, on derivative instruments from

accumulated other comprehensive income to earnings during the next 12 months terminated swaps are amortized and as interest

payments and receipts on derivative instruments occur. This amount could change in future periods if the Company decides to

terminate additional swaps in the context of managing its overall market risk profile.

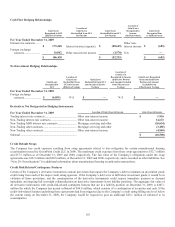

Hedge of Net Investment in Foreign Operations

The Company uses forward exchange contracts to protect the value of its investment in its foreign subsidiaries. Realized and

unrealized foreign currency gains and losses from these hedges are not included in the income statement, but are shown in the

translation adjustments in other comprehensive income. The purpose of these hedges is to protect against adverse movements in

exchange rates.

Trading Interest Rate Contracts

The Company enters into customer-oriented derivative financial instruments, including interest rate swaps, options, caps, floors, and

foreign exchange contracts. These customer-oriented positions may be matched with offsetting positions to minimize risk to the

Company.

These derivatives do not qualify as accounting hedges and are recorded on the balance sheet at fair value with changes in value

included in current earnings in non-interest income.

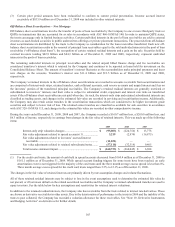

Non-Trading Interest Rate Contracts

The Company uses interest rate swaps to manage interest rate sensitivity related to the Company’s non-mortgage securitization

programs. The Company enters into interest rate swaps with its securitization trust and essentially offsets the derivative with separate

interest rate swaps with third parties. The Company is exposed to higher credit risk related to interest rate swaps with the trust, and has

charged a higher rate to offset this risk. The trust is unable to post collateral because of its QSPE status. At December 31, 2009, the

Company had a $22.3 million valuation allowance on the derivative receivable from the trust, representing counterparty credit risk.

Upon consolidation of the trust on January 1, 2010 due to the adoption of AU 2009-17 (ASC 810/SFAS 167), the interest rate swap

agreements between the Company and its credit card master trust will be considered intercompany agreements and any related

receivables and payables are eliminated in consolidation. On December 31, 2009, the interest rate swaps with third parties were

terminated and replaced with similar agreements at current fixed interest rates. The replacement interest rate swaps will be designated

as cash flow hedges converting floating rate debt of the trust to fixed rate debt in connection with the consolidation of the trust, and

the corresponding debt securities issued to third parties. See “Note 1- Significant Accounting Policies” for additional information.