Capital One 2009 Annual Report Download - page 122

Download and view the complete annual report

Please find page 122 of the 2009 Capital One annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

|

|

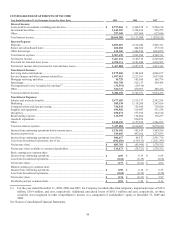

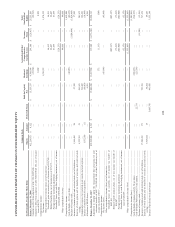

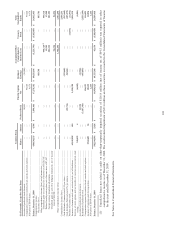

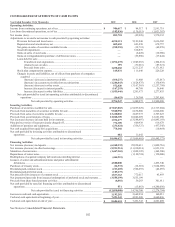

109

Significant Accounting Policies

Cash and Cash Equivalents

Cash and cash equivalents includes cash and due from banks, federal funds sold and resale agreements and interest-bearing deposits at

other banks, all of which, if applicable, have stated maturities of three months or less when acquired. Cash paid for interest for the

years ended December 31, 2009, 2008 and 2007 was $3.1 billion, $4.0 billion, and $4.5 billion, respectively. Cash paid for income

taxes for the years ended December 31, 2009, 2008 and 2007 was $0.4 billion, $1.2 billion and $1.5 billion, respectively.

Securities Available for Sale

The Company considers debt securities in its investment portfolio as available for sale. These securities are stated at fair value, with

the unrealized gains and losses, net of tax, reported as a component of accumulated other comprehensive income. The fair values of

securities is based on quoted market prices, or if quoted market prices are not available, then the fair value is estimated using the

quoted market prices for similar securities, pricing models or discounted cash flow, using observable market data where available. The

amortized cost of debt securities is adjusted for amortization of premiums and accretion of discounts to maturity. Such amortization or

accretion is included in interest income. Realized gains and losses on sales of securities are determined using the specific identification

method. The Company evaluates its unrealized loss positions for impairment in accordance with ASC 320-10/SFAS 115. The

Company also considers any intent to sell a security in an unrealized loss position and the likelihood it will be required to sell a

security before its anticipated recovery. As such, when there is other-than-temporary impairment and the Company does not intend to

sell and will more likely that not be required to sell the security, the Company will recognize credit-related impairments in earnings

while non credit-related impairments are recorded in other comprehensive income. See “Note 6- Securities Available for Sale” for

additional details.

Securities Held to Maturity

In connection with the acquisition of Chevy Chase Bank, certain investments are carried as held to maturity which is consistent with

their designation at the time of acquisition. These securities are stated at amortized cost and assessed for impairment in accordance

with ASC320-10/SFAS 115. If impaired and we intend to sell the security or will more likely than not be required to sell the security

before the recovery of its amortized cost less the current period credit loss, the other-than-temporary impairment would be recognized

in earnings. Otherwise it will be accounted for as described in the preceding Securities Available for Sale.

Loans Held for Sale

The Company classifies loans originated with the intent of selling in the secondary market as held for sale. Loans originated for sale

are primarily sold in the secondary market as whole loans. Whole loan sales are executed with either the servicing rights being

retained or released to the buyer. For sales where the loans are sold with the servicing released to the buyer, the gain or loss on the sale

is equal to the difference between the proceeds received and the carrying value of the loans sold. If the loans are sold with the

servicing rights retained, the gain or loss on the sale is also impacted by the fair value attributed to the servicing rights. In the third

quarter of 2007, the Company shut down the mortgage origination operations of its wholesale mortgage banking unit, GreenPoint. The

results of the mortgage origination operation of GreenPoint have been accounted for as discontinued operations and have been

removed from the Company’s results of continuing operations for all periods presented. The results of GreenPoint’s mortgage

servicing business continue to be reported as part of the Company’s continuing operations.

Loans held for sale are carried at the lower of aggregate cost, net of deferred fees, deferred origination costs and effects of hedge

accounting, or fair value. The fair value of loans held for sale is determined using current secondary market prices for loans with

similar coupons, maturities and credit quality. The fair value of loans held for sale is impacted by changes in market interest rates. The

exposure to changes in market interest rates is hedged primarily by selling forward contracts on agency securities. These derivative

instruments are considered non-trading derivatives, that do not qualify for hedge accounting and are recorded on the balance sheet at

fair value with changes in fair value being recorded in current period earnings and reflected in mortgage banking operations. Also,

changes in the fair value of loans held for sale are recorded as an adjustment to the loans’ carrying basis through mortgage banking

operations income in current earnings. During 2009, the Company classified $127.5 million of its small ticket commercial real estate

portfolio as available for sale and recognized a write-down of $79.5 million.

As of December 31, 2009 and 2008, the balance in loans held for sale was $268.3 million and $68.5 million, respectively.

Loan Securitizations

The Company primarily securitizes credit card loans, auto loans, mortgage loans and installment loans. Securitization currently

provides the Company with a significant source of liquidity and favorable regulatory capital treatment for securitizations accounted

for as off-balance sheet arrangements. See “Note 20- Securitizations” and “Note 15- Mortgage Servicing Rights” for additional

details.