Capital One 2009 Annual Report Download - page 142

Download and view the complete annual report

Please find page 142 of the 2009 Capital One annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

151 -

152

152 -

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

|

|

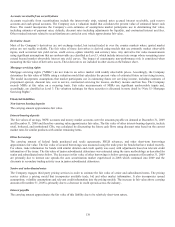

129

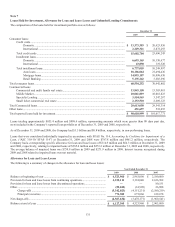

Cumulative other-than-temporary impairment related to credit losses recognized in earnings for available-for-sale securities is as

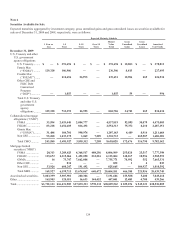

follows:

OTTI credit losses recognized for

AFS debt

securities

Beginning balance of

OTTI credit losses

recognized for

securities held at the

beginning of the

period for which a

portion of OTTI was

recognized in OCI

Additional increases

to the amount related

to credit loss for

which an OTTI was

previously recognized

Additions for the

amount related to

credit loss for which

OTTI was not

previously recognized

Reductions for

securities sold

during the

period

Ending balance of

the amount related

to credit losses

held at the end of

the period for

which a portion of

OTTI was

recognized in OCI

Year ended

December 31, 2009

CMO ........................ $ — $ — $ 15,159 $ — $ 15,159

MBS ......................... — — 15,612 — 15,612

Other-Home

equity ................... — — 817 — 817

Total................................... $ — $ — $ 31,588 $ — $ 31,588

Collateralized Mortgage Obligations The Company’s portfolio includes investments in GSE collateralized mortgage obligations and

prime non-agency collateralized mortgage obligations. The unrealized losses on the Company’s investment in collateralized mortgage

obligations were primarily caused by credit spreads and interest rates that are higher than levels existing at the date of purchase. As of

December 31, 2009, the majority of the unrealized losses in this category are due to prime non-agency collateralized mortgage

obligations, of which 2% are rated AAA, 24% are rated other investment grade and 74% are non-investment grade or not rated. As of

December 31, 2008, the majority of the unrealized losses in this category is due to prime non-agency collateralized mortgage

obligations, of which 61% are rated AAA, 35% are rated other investment grade and 4% are non-investment grade or not rated. The

decline in ratings reflects the continued deterioration in non-agency collateralized mortgage obligations due to the challenging

economic environment. While the ratings for this sub-category of CMO declined significantly from 2008 to 2009, these investments

represent only 4% and 8% of the Company’s total available-for-sale portfolio at December 31, 2009 and 2008, respectively.

The Company recognized credit-related other-than-temporary impairment of $15.2 million through earnings for the year ended

December 31, 2009, for thirteen prime non-agency collateralized mortgage obligations. For these impaired securities, unrealized

losses not related to credit and therefore recognized in other comprehensive income was $96.1 million (net of tax was $61.9 million)

as of December 31, 2009. While these securities experienced significant decreases in fair value in the second half of 2008 due to

deteriorating credit fundamentals and elevated liquidity premiums, there has been substantial improvement in fair value during 2009

as the market has stabilized and risk premiums have tightened despite interest rates increasing. The credit-related impairment was

calculated based on internal forecasts using security specific delinquencies, product specific delinquency roll rates and expected

severities, using industry standard third party modeling tools. The significant key assumptions used to measure the credit-related

component of securities deemed to be other-than-temporarily impaired in 2009 are as follows: a weighted average credit default rate

of 6.76% and a weighted average expected severity of 51%. See “Note 1- Significant Accounting Policies” for a discussion of the

2009 changes to key assumptions used to measure the credit-related component of securities deemed to be other-than-temporarily

impaired.

Based on its view of each prime non-agency security’s current credit performance along with the sufficiency of subordination to

protect cash flows and the implicit U.S. Government guarantee of FNMA/FHLMC securities and the explicit U.S. Government

guarantee of GNMA securities, the Company expects to recover the entire amortized cost basis of its remaining collateralized

mortgage obligations. Furthermore, since the Company does not have the intent to sell nor will it more likely than not be required to

sell before anticipated recovery, it does not consider any of its remaining collateralized mortgage obligations in unrealized loss

positions to be other-than-temporarily impaired at December 31, 2009 and 2008.

Mortgage-Backed Securities The Company’s portfolio includes investments in GSE mortgage-backed securities and prime non-

agency mortgage-backed securities. The unrealized losses on the Company’s investment in mortgage-backed securities were primarily

caused by credit spreads and interest rates that are higher than levels existing at the date of purchase. As of December 31, 2009 the

majority of unrealized losses is due to prime non-agency mortgage-backed securities of which 4% are rated AAA, 7% are rated other

investment grade and 89% are non-investment grade or not rated. As of December 31, 2008, the majority of unrealized losses is due to

prime non-agency mortgage-backed securities of which 67% are rated AAA, 23% are rated other investment grade and 10% are non-

investment grade or not rated. The decline noted in ratings for non-agency mortgage backed securities reflects the continued

deterioration the investments were subject to due to the continued economic challenges facing mortgage-related assets. While the

ratings for this sub-category of MBS declined significantly from 2008 to 2009, these investments represent only 3% and 4% of the

Company’s total available-for-sale portfolio at December 31, 2009 and 2008, respectively.