PNC Bank 2011 Annual Report Download - page 78

Download and view the complete annual report

Please find page 78 of the 2011 PNC Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

|

|

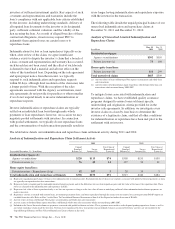

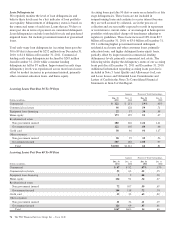

The table below reflects the estimated effects on pension

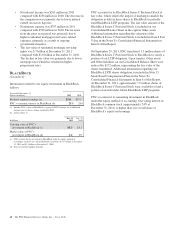

expense of certain changes in annual assumptions, using 2012

estimated expense as a baseline.

Change in Assumption (a)

Estimated

Increase to 2012

Pension

Expense

(In millions)

.5% decrease in discount rate $23

.5% decrease in expected long-term return on assets $18

.5% increase in compensation rate $ 2

(a) The impact is the effect of changing the specified assumption while holding all other

assumptions constant.

Our pension plan contribution requirements are not

particularly sensitive to actuarial assumptions. Investment

performance has the most impact on contribution requirements

and will drive the amount of permitted contributions in future

years. Also, current law, including the provisions of the

Pension Protection Act of 2006, sets limits as to both

minimum and maximum contributions to the plan. We do not

expect to be required by law to make any contributions to the

plan during 2012.

We maintain other defined benefit plans that have a less

significant effect on financial results, including various

nonqualified supplemental retirement plans for certain

employees.

R

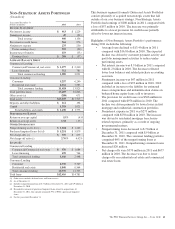

ECOURSE

A

ND

R

EPURCHASE

O

BLIGATIONS

As discussed in Note 3 Loan Sale and Servicing Activities and

Variable Interest Entities in the Notes To Consolidated

Financial Statements in Item 8 of this Report, PNC has sold

commercial mortgage and residential mortgage loans directly

or indirectly in securitizations and whole-loan sale

transactions with continuing involvement. One form of

continuing involvement includes certain recourse and loan

repurchase obligations associated with the transferred assets in

these transactions.

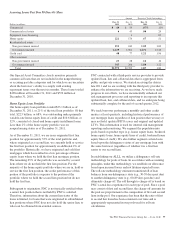

Commercial Mortgage Loan Recourse Obligations

We originate, close, and service certain multi-family

commercial mortgage loans which are sold to FNMA under

FNMA’s Delegated Underwriting and Servicing (DUS)

program. We participated in a similar program with the

FHLMC.

Under these programs, we generally assume up to a one-third

pari passu risk of loss on unpaid principal balances through a

loss share arrangement. At December 31, 2011 and

December 31, 2010, the unpaid principal balance outstanding

of loans sold as a participant in these programs was $13.0

billion and $13.2 billion, respectively. The potential maximum

exposure under the loss share arrangements was $4.0 billion at

both December 31, 2011 and December 31, 2010. We

maintain a reserve for estimated losses based on our exposure.

The reserve for losses under these programs totaled $47

million and $54 million as of December 31, 2011 and

December 31, 2010, respectively, and is included in Other

liabilities on our Consolidated Balance Sheet. If payment is

required under these programs, we would not have a

contractual interest in the collateral underlying the mortgage

loans on which losses occurred, although the value of the

collateral is taken into account in determining our share of

such losses. Our exposure and activity associated with these

recourse obligations are reported in the Corporate &

Institutional Banking segment.

Residential Mortgage Loan and Home Equity Repurchase

Obligations

While residential mortgage loans are sold on a non-recourse

basis, we assume certain loan repurchase obligations

associated with mortgage loans we have sold to investors.

These loan repurchase obligations primarily relate to

situations where PNC is alleged to have breached certain

origination covenants and representations and warranties

made to purchasers of the loans in the respective purchase and

sale agreements. Residential mortgage loans covered by these

loan repurchase obligations include first and second-lien

mortgage loans we have sold through Agency securitizations,

Non-Agency securitizations, and whole-loan sale transactions.

As discussed in Note 3 in the Notes To Consolidated Financial

Statements in Item 8 of this Report, Agency securitizations

consist of mortgage loans sale transactions with FNMA,

FHLMC, and the Government National Mortgage Association

(GNMA) program, while Non-Agency securitizations and

whole-loan sale transactions consist of mortgage loans sale

transactions with private investors. Our historical exposure

and activity associated with Agency securitization repurchase

obligations has primarily been related to transactions with

FNMA and FHLMC, as indemnification and repurchase losses

associated with Federal Housing Agency (FHA) and

Department of Veterans Affairs (VA)-insured and uninsured

loans pooled in GNMA securitizations historically have been

minimal. Repurchase obligation activity associated with

residential mortgages is reported in the Residential Mortgage

Banking segment.

PNC’s repurchase obligations also include certain brokered

home equity loans/lines that were sold to a limited number of

private investors in the financial services industry by National

City prior to our acquisition. PNC is no longer engaged in the

brokered home equity lending business, and our exposure

under these loan repurchase obligations is limited to

repurchases of the whole-loans sold in these transactions.

Repurchase activity associated with brokered home equity

lines/loans are reported in the Non-Strategic Assets Portfolio

segment.

Loan covenants and representations and warranties are

established through loan sale agreements with various

investors to provide assurance that PNC has sold loans to

The PNC Financial Services Group, Inc. – Form 10-K 69