PNC Bank 2011 Annual Report Download - page 198

Download and view the complete annual report

Please find page 198 of the 2011 PNC Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

188 -

189

189 -

190

190 -

191

191 -

192

192 -

193

193 -

194

194 -

195

195 -

196

196 -

197

197 -

198

198 -

199

199 -

200

200 -

201

201 -

202

202 -

203

203 -

204

204 -

205

205 -

206

206 -

207

207 -

208

208 -

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

|

|

N

OTE

21 R

EGULATORY

M

ATTERS

We are subject to the regulations of certain federal, state, and

foreign agencies and undergo periodic examinations by such

regulatory authorities.

The ability to undertake new business initiatives (including

acquisitions), the access to and cost of funding for new

business initiatives, the ability to pay dividends or repurchase

shares, the level of deposit insurance costs, and the level and

nature of regulatory oversight depend, in large part, on a

financial institution’s capital strength. The minimum US

regulatory capital ratios under Basel I are 4% for Tier 1 risk-

based, 8% for total risk-based and 4% for leverage. To qualify

as “well capitalized,” regulators require banks to maintain

capital ratios of at least 6% for Tier 1 risk-based, 10% for total

risk-based and 5% for leverage. To be “well capitalized,” a

bank holding company must maintain capital ratios of at least

6% Tier 1 risk-based and 10% for total risk-based. At

December 31, 2011 and December 31, 2010, PNC and PNC

Bank, N.A. met the “well capitalized” capital ratio

requirements based on US regulatory capital ratio

requirements under Basel I.

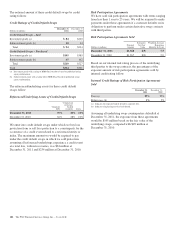

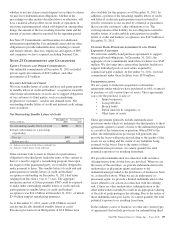

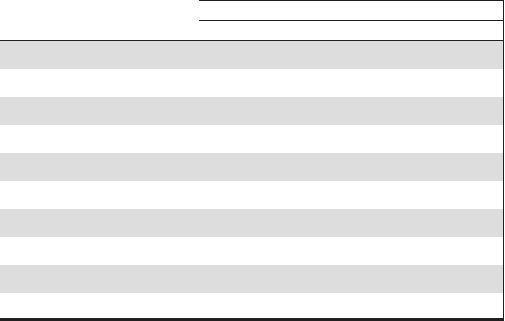

The following table sets forth regulatory capital ratios for

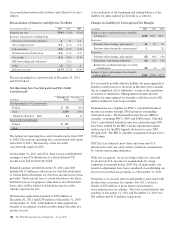

PNC and its bank subsidiary, PNC Bank, N.A.

Regulatory Capital

Amount Ratios

December 31 Dollars in millions 2011 2010 2011 2010

Risk-based capital

Tier 1

PNC $29,073 $26,092 12.6% 12.1%

PNC Bank, N.A. 25,536 24,722 11.4 11.8

Total

PNC 36,548 33,724 15.8 15.6

PNC Bank, N.A. 32,322 31,662 14.4 15.1

Leverage

PNC 29,073 26,092 11.1 10.2

PNC Bank, N.A. 25,536 24,722 10.0 10.0

The principal source of parent company cash flow is the

dividends it receives from its subsidiary bank, which may be

impacted by the following:

• Capital needs,

• Laws and regulations,

• Corporate policies,

• Contractual restrictions, and

• Other factors.

Also, there are statutory and regulatory limitations on the

ability of national banks to pay dividends or make other

capital distributions. The amount available for dividend

payments to the parent company by PNC Bank, N.A. without

prior regulatory approval was approximately $1.7 billion at

December 31, 2011.

Under federal law, a bank subsidiary generally may not extend

credit to the parent company or its non-bank subsidiaries on

terms and under circumstances that are not substantially the

same as comparable extensions of credit to nonaffiliates. No

extension of credit may be made to the parent company or a

non-bank subsidiary which is in excess of 10% of the capital

stock and surplus of such bank subsidiary or in excess of 20%

of the capital and surplus of such bank subsidiary as to

aggregate extensions of credit to the parent company and its

non-bank subsidiaries. Such extensions of credit, with limited

exceptions, must be fully collateralized by certain specified

assets. In certain circumstances, federal regulatory authorities

may impose more restrictive limitations.

Federal Reserve Board regulations require depository

institutions to maintain cash reserves with a Federal Reserve

Bank (FRB). At December 31, 2011, the balance outstanding

at the FRB was $407 million.

N

OTE

22 L

EGAL

P

ROCEEDINGS

We establish accruals for legal proceedings, including

litigation and regulatory and governmental investigations and

inquiries, when information related to the loss contingencies

represented by those matters indicates both that a loss is

probable and that the amount of loss can be reasonably

estimated. Any such accruals are adjusted thereafter as

appropriate to reflect changed circumstances. When we are

able to do so, we also determine estimates of possible losses

or ranges of possible losses, whether in excess of any related

accrued liability or where there is no accrued liability, for

disclosed legal proceedings (“Disclosed Matters,” which are

those matters disclosed in this Note 22). For Disclosed

Matters where we are able to estimate such possible losses or

ranges of possible losses, as of December 31, 2011, we

estimate that it is reasonably possible that we could incur

losses in an aggregate amount of up to approximately $550

million. The estimates included in this amount are based on

our analysis of currently available information and are subject

to significant judgment and a variety of assumptions and

uncertainties. As new information is obtained we may change

our estimates. Due to the inherent subjectivity of the

assessments and unpredictability of outcomes of legal

proceedings, any amounts accrued or included in this

aggregate amount may not represent the ultimate loss to us

from the legal proceedings in question. Thus, our exposure

and ultimate losses may be higher, and possibly significantly

so, than the amounts accrued or this aggregate amount.

The aggregate estimated amount provided above does not

include an estimate for every Disclosed Matter, as we are

unable, at this time, to estimate the losses that it is reasonably

possible that we could incur or ranges of such losses with

respect to some of the matters disclosed for one or more of the

following reasons. In our experience, legal proceedings are

inherently unpredictable. In many legal proceedings, various

factors exacerbate this inherent unpredictability, including,

The PNC Financial Services Group, Inc. – Form 10-K 189