PNC Bank 2011 Annual Report Download - page 74

Download and view the complete annual report

Please find page 74 of the 2011 PNC Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

|

|

interest-earning assets including unearned income in the

accretion of fair value adjustments on discounts recognized on

acquired or purchased loans is recognized based on the

constant effective yield of the financial instrument.

The timing and amount of revenue that we recognize in any

period is dependent on estimates, judgments, assumptions, and

interpretation of contractual terms. Changes in these factors

can have a significant impact on revenue recognized in any

period due to changes in products, market conditions or

industry norms.

Residential And Commercial Mortgage Servicing Rights

We elect to measure our residential mortgage servicing rights

(MSRs) at fair value. This election was made to be consistent

with our risk management strategy to hedge changes in the

fair value of these assets as described below. The fair value of

residential MSRs is estimated by using a cash flow valuation

model which calculates the present value of estimated future

net servicing cash flows, taking into consideration actual and

expected mortgage loan prepayment rates, discount rates,

servicing costs, and other economic factors which are

determined based on current market conditions.

Assumptions incorporated into the residential MSRs valuation

model reflect management’s best estimate of factors that a

market participant would use in valuing the residential MSRs.

Although sales of residential MSRs do occur, residential

MSRs do not trade in an active market with readily observable

prices so the precise terms and conditions of sales are not

available. As a benchmark for the reasonableness of its

residential MSRs fair value, PNC obtains opinions of value

from independent parties (“brokers”). These brokers provided

a range (+/- 10 bps) based upon their own discounted cash

flow calculations of our portfolio that reflected conditions in

the secondary market, and any recently executed servicing

transactions. PNC compares its internally-developed

residential MSRs value to the ranges of values received from

the brokers. If our residential MSRs fair value falls outside of

the brokers’ ranges, management will assess whether a

valuation adjustment is warranted. For 2011 and 2010, PNC’s

residential MSRs value has not fallen outside of the brokers’

ranges. We consider our residential MSRs value to represent a

reasonable estimate of fair value.

Commercial MSRs are purchased or originated when loans are

sold with servicing retained. Commercial MSRs do not trade

in an active market with readily observable prices so the

precise terms and conditions of sales are not available.

Commercial MSRs are initially recorded at fair value and are

subsequently accounted for at the lower of amortized cost or

fair value. Commercial MSRs are periodically evaluated for

impairment. For purposes of impairment, the commercial

mortgage servicing rights are stratified based on asset type,

which characterizes the predominant risk of the underlying

financial asset. The fair value of commercial MSRs is

estimated by using an internal valuation model. The model

calculates the present value of estimated future net servicing

cash flows considering estimates of servicing revenue and

costs, discount rates and prepayment speeds.

PNC employs risk management strategies designed to protect

the value of MSRs from changes in interest rates and related

market factors. Residential MSRs values are economically

hedged with securities and derivatives, including interest-rate

swaps, options, and forward mortgage-backed and futures

contracts. As interest rates change, these financial instruments

are expected to have changes in fair value negatively

correlated to the change in fair value of the hedged residential

MSRs portfolio. The hedge relationships are actively managed

in response to changing market conditions over the life of the

residential MSRs assets. Commercial MSRs are economically

hedged at a macro level or with specific derivatives to protect

against a significant decline in interest rates. Selecting

appropriate financial instruments to economically hedge

residential or commercial MSRs requires significant

management judgment to assess how mortgage rates and

prepayment speeds could affect the future values of MSRs.

Hedging results can frequently be less predictable in the short

term, but over longer periods of time are expected to protect

the economic value of the MSRs.

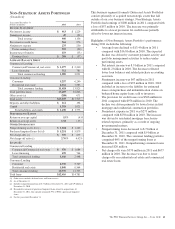

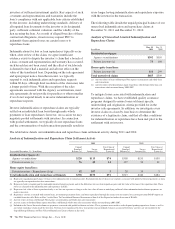

The fair value of residential and commercial MSRs and

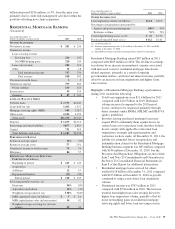

significant inputs to the valuation model as of December 31,

2011 are shown in the tables below. The expected and actual

rates of mortgage loan prepayments are significant factors

driving the fair value. Management uses a third-party model to

estimate future residential loan prepayments and internal

proprietary models to estimate future commercial loan

prepayments. These models have been refined based on

current market conditions. Future interest rates are another

important factor in the valuation of MSRs. Management

utilizes market implied forward interest rates to estimate the

future direction of mortgage and discount rates. The forward

rates utilized are derived from the current yield curve for U.S.

dollar interest rate swaps and are consistent with pricing of

capital markets instruments. Changes in the shape and slope of

the forward curve in future periods may result in volatility in

the fair value estimate.

Residential Mortgage Servicing Rights

Dollars in millions

December 31

2011

December 31

2010

Fair value $ 647 $1,033

Weighted-average life (in years) (a) 3.6 5.8

Weighted-average constant

prepayment rate (a) 22.10% 12.61%

Weighted-average option adjusted

spread 11.77% 12.18%

(a) Changes in weighted-average life and weighted-average constant prepayment rate

reflect the cumulative impact of changes in rates, prepayment expectations and

model changes.

The PNC Financial Services Group, Inc. – Form 10-K 65