PNC Bank 2011 Annual Report Download - page 150

Download and view the complete annual report

Please find page 150 of the 2011 PNC Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

151 -

152

152 -

153

153 -

154

154 -

155

155 -

156

156 -

157

157 -

158

158 -

159

159 -

160

160 -

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

|

|

pool is then accounted for as a single asset with a single

composite interest rate and an aggregate expectation of cash

flows. With respect to the National City acquisition, we

aggregated homogeneous consumer and residential real estate

loans into pools with common risk characteristics. We account

for commercial and commercial real estate loans individually.

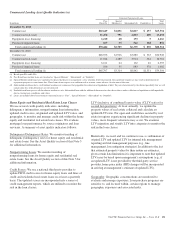

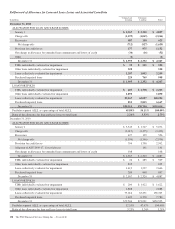

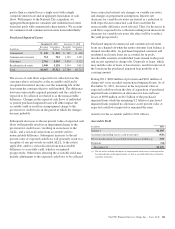

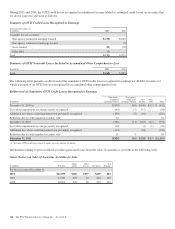

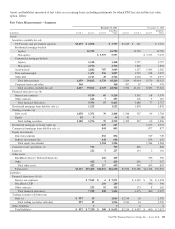

Purchased Impaired Loans

December 31, 2011 December 31, 2010

In millions

Recorded

Investment

Outstanding

Balance

Recorded

Investment

Outstanding

Balance

Commercial $ 140 $ 245 $ 249 $ 408

Commercial real estate 712 743 1,153 1,391

Consumer 2,766 3,405 3,024 4,121

Residential real estate 3,049 3,128 3,354 3,803

Total $6,667 $7,521 $7,780 $9,723

The excess of cash flows expected to be collected over the

carrying value is referred to as the accretable yield and is

recognized in interest income over the remaining life of the

loan using the constant effective yield method. The difference

between contractually required payments and the cash flows

expected to be collected is referred to as the nonaccretable

difference. Changes in the expected cash flows of individual

or pooled purchased impaired loans will either impact the

accretable yield or result in an impairment charge to the

provision for credit losses in the period in which the changes

become probable.

Subsequent decreases to the net present value of expected cash

flows will generally result in an impairment charge to the

provision for credit losses, resulting in an increase to the

ALLL, and a reclassification from accretable yield to

nonaccretable difference. Subsequent increases to the net

present value of expected cash flows will generally result in a

recapture of any previously recorded ALLL, to the extent

applicable, and/or a reclassification from nonaccretable

difference to accretable yield, which is recognized

prospectively. Other items affecting the accretable yield may

include adjustments to the expected cash flows to be collected

from contractual interest rate changes on variable rate notes,

and changes in prepayment assumptions. Interest rate

decreases for variable rate notes are treated as a reduction of

both expected and contractual cash flows such that the

nonaccretable difference is not affected. Thus, for decreases in

cash flows expected to be collected resulting from interest rate

decreases for variable rate notes, the effect will be to reduce

the yield prospectively.

Purchased impaired commercial and commercial real estate

loans are charged off when the entire customer loan balance is

deemed uncollectible. As purchased impaired consumer and

residential real estate loans are accounted for in pools,

uncollectible amounts on individual loans remain in the pools

and are not reported as charge-offs. Disposals of loans, which

may include sales of loans or foreclosures, result in removal of

the loan from the purchased impaired loan portfolio at its

carrying amount.

During 2011, $262 million of provision and $161 million of

charge-offs were recorded on purchased impaired loans. As of

December 31, 2011, decreases in the net present value of

expected cash flows from the date of acquisition of purchased

impaired loans resulted in an allowance for loan and lease

losses of $998 million on $6.5 billion of the purchased

impaired loans while the remaining $.2 billion of purchased

impaired loans required no allowance as net present value of

expected cash flows improved or remained the same.

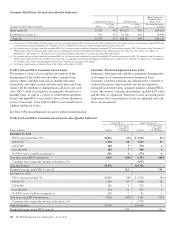

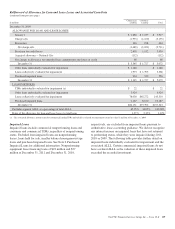

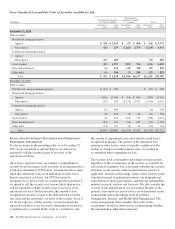

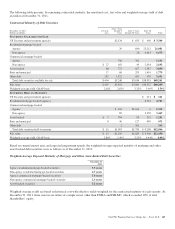

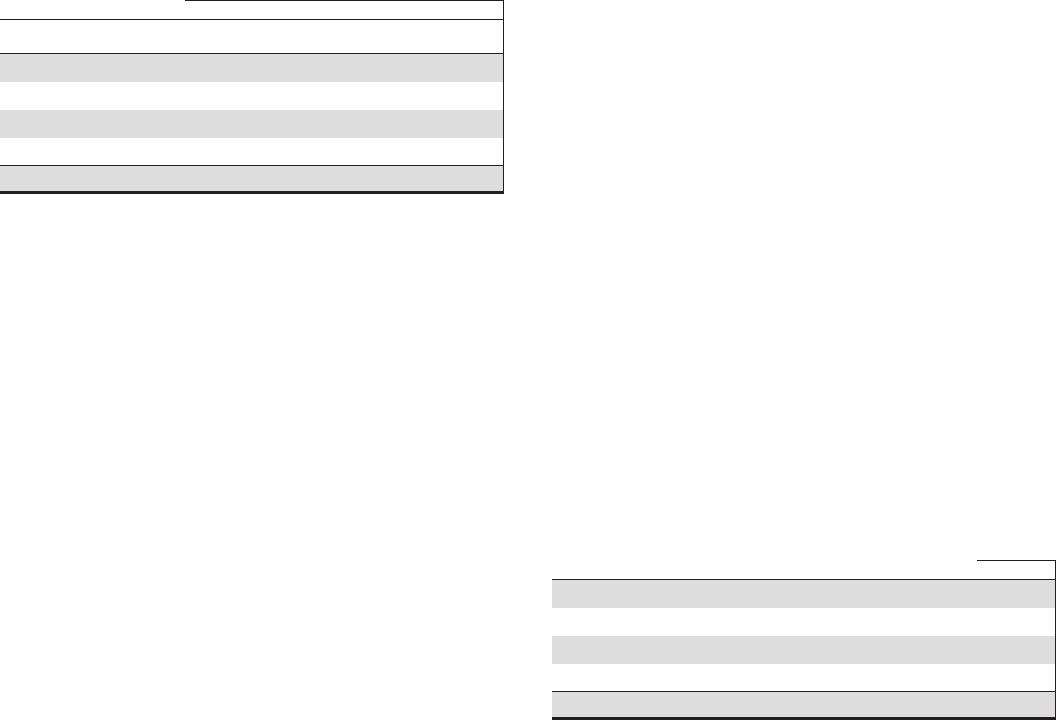

Activity for the accretable yield for 2011 follows.

Accretable Yield

In millions 2011

January 1 $2,185

Accretion (including excess cash recoveries) (920)

Net reclassifications to accretable from non-accretable (a) 908

Disposals (64)

December 31 $2,109

(a) The net reclass includes the impact of improvements in the excess cash expected to

be collected from credit improvements, as well as accretable differences related to

cash flow extensions.

The PNC Financial Services Group, Inc. – Form 10-K 141