Wells Fargo 2015 Annual Report Download - page 88

Download and view the complete annual report

Please find page 88 of the 2015 Wells Fargo annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

|

|

Risk Management – Credit Risk Management (continued)

LIABILITY FOR MORTGAGE LOAN REPURCHASE LOSSES

We sell residential mortgage loans to various parties, including

(1) government-sponsored entities (GSEs) Federal Home Loan

Mortgage Corporation (FHLMC) and Federal National Mortgage

Association (FNMA) who include the mortgage loans in GSE-

guaranteed mortgage securitizations, (2) SPEs that issue private

label MBS, and (3) other financial institutions that purchase

mortgage loans for investment or private label securitization. In

addition, we pool FHA-insured and VA-guaranteed mortgage

loans that are then used to back securities guaranteed by the

Government National Mortgage Association (GNMA). We may

be required to repurchase these mortgage loans, indemnify the

securitization trust, investor or insurer, or reimburse the

securitization trust, investor or insurer for credit losses incurred

on loans (collectively, repurchase) in the event of a breach of

contractual representations or warranties that is not remedied

within a period (usually 90 days or less) after we receive notice

of the breach. The majority of repurchase demands are on loans

that default in the first 24 to 36 months following origination of

the mortgage loan.

In connection with our sales and securitization of residential

mortgage loans to various parties, we have established a

mortgage repurchase liability, initially at fair value, related to

various representations and warranties that reflect

management’s estimate of losses for loans for which we could

have a repurchase obligation, whether or not we currently

service those loans, based on a combination of factors. Our

mortgage repurchase liability estimation process also

incorporates a forecast of repurchase demands associated with

mortgage insurance rescission activity.

Because we retain the servicing for most of the mortgage

loans we sell or securitize, we believe the quality of our

residential mortgage loan servicing portfolio provides helpful

information in evaluating our repurchase liability. Of the

$1.6 trillion in the residential mortgage loan servicing portfolio

at December 31, 2015, 95% was current and less than 2% was

subprime at origination. Our combined delinquency and

foreclosure rate on this portfolio was 5.18% at December 31,

2015, compared with 5.79% at December 31, 2014. Three percent

of this portfolio is private label securitizations for which we

originated the loans and, therefore, have some repurchase risk.

The overall level of unresolved repurchase demands and

mortgage insurance rescissions outstanding at

December 31, 2015, was $62 million, representing 280 loans,

down from $183 million, or 839 loans, a year ago, as we

observed a decline in new demands and continued to work

through the outstanding demands and mortgage insurance

rescissions.

Customary with industry practice, we have the right of

recourse against correspondent lenders from whom we have

purchased loans with respect to representations and warranties.

Historical recovery rates as well as projected lender performance

are incorporated in the establishment of our mortgage

repurchase liability.

We do not typically receive repurchase requests from

GNMA, FHA and the Department of Housing and Urban

Development (HUD) or VA. As an originator of an FHA-insured

or VA-guaranteed loan, we are responsible for obtaining the

insurance with the FHA or the guarantee with the VA. To the

extent we are not able to obtain the insurance or the guarantee

we must request permission to repurchase the loan from the

GNMA pool. Such repurchases from GNMA pools typically

represent a self-initiated process upon discovery of the

uninsurable loan (usually within 180 days from funding of the

loan). Alternatively, in lieu of repurchasing loans from GNMA

pools, we may be asked by FHA/HUD or the VA to indemnify

them (as applicable) for defects found in the Post Endorsement

Technical Review process or audits performed by FHA/HUD or

the VA. The Post Endorsement Technical Review is a process

whereby HUD performs underwriting audits of closed/insured

FHA loans for potential deficiencies. Our liability for mortgage

loan repurchase losses incorporates probable losses associated

with such indemnification.

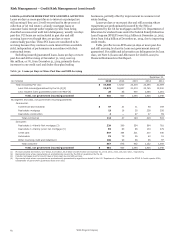

Table 39 summarizes the changes in our mortgage

repurchase liability. We incurred net losses on repurchased

loans and investor reimbursements totaling $78 million in 2015,

compared with $144 million in 2014.

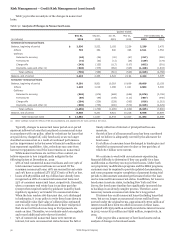

Table 39: Changes in Mortgage Repurchase Liability

Quarter ended

Dec 31, Sep 30, Jun 30, Mar 31, Year ended Dec. 31,

(in millions) 2015 2015 2015 2015 2015 2014 2013

Balance, beginning of period $ 538 557 586 615 615 899 2,206

Provision for repurchase losses:

Loan sales 9 11 13 10 43 44 143

Change in estimate (1) (128) (17) (31) (26) (202) (184) 285

Total additions (reductions) (119) (6) (18) (16) (159) (140) 428

Losses (2) (41) (13) (11) (13) (78) (144) (1,735)

Balance, end of period $ 378 538 557 586 378 615 899

(1) Results from changes in investor demand and mortgage insurer practices, credit deterioration and changes in the financial stability of correspondent lenders.

(2) Year ended December 31, 2013, reflects $746 million as a result of the agreement with FHLMC that resolves substantially all repurchase liabilities related to loans sold to

FHLMC prior to January 1, 2009. Year ended December 31, 2013, reflects $508 million as a result of the agreement with FNMA that resolves substantially all repurchase

liabilities related to loans sold to FNMA that were originated prior to January 1, 2009.

Wells Fargo & Company

86