Wells Fargo 2015 Annual Report Download - page 108

Download and view the complete annual report

Please find page 108 of the 2015 Wells Fargo annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

|

|

Capital Management (continued)

SUPPLEMENTARY LEVERAGE RATIO In April 2014, federal

banking regulators finalized a rule that enhances the SLR

requirements for BHCs, like Wells Fargo, and their insured

depository institutions. The SLR consists of Tier 1 capital under

Basel III divided by the Company’s total leverage exposure. Total

leverage exposure consists of the total average on-balance sheet

assets, plus off-balance sheet exposures, such as undrawn

commitments and derivative exposures, less amounts permitted

to be deducted from Tier 1 capital. The rule, which becomes

effective on January 1, 2018, will require a covered BHC to

maintain a SLR of at least 5.0% (comprised of the 3.0%

minimum requirement and a supplementary leverage buffer of

2.0%) to avoid restrictions on capital distributions and

discretionary bonus payments. The rule will also require that all

of our insured depository institutions maintain a SLR of 6.0%

under applicable regulatory capital adequacy guidelines. In

September 2014, federal banking regulators finalized additional

changes to the SLR requirements to implement revisions to the

Basel III leverage framework finalized by the BCBS in January

2014. These additional changes, among other things, modify the

methodology for including off- balance sheet items, including

credit derivatives, repo-style transactions and lines of credit, in

the denominator of the SLR, and will become effective on

January 1, 2018. At December 31, 2015, our SLR for the

Company was 7.7% assuming full phase-in of the Basel III

Advanced Approach capital framework. Based on our review, our

current leverage levels would exceed the applicable requirements

for each of our insured depository institutions as well. The fully

phased-in SLR is considered a non-GAAP financial measure that

is used by management, bank regulatory agencies, investors and

analysts to assess and monitor the Company’s leverage exposure.

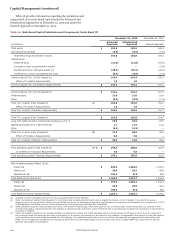

See Table 59 for information regarding the calculation and

components of the SLR.

Table 59: Basel III Fully Phased-In SLR

(in billions) December 31, 2015

Tier 1 capital $ 162.8

Total average assets 1,787.3

Less: deductions from Tier 1 capital 29.6

Total adjusted average assets 1,757.7

Adjustments:

Derivative exposures 63.2

Repo-style transactions 3.3

Other off-balance sheet exposures 292.3

Total adjustments 358.8

Total leverage exposure $ 2,116.5

Supplementary leverage ratio 7.7%

OTHER REGULATORY CAPITAL MATTERS In October 2015,

the FRB proposed rules to address the amount of equity and

unsecured long-term debt a U.S. G-SIB must hold to improve its

resolvability and resiliency, often referred to as Total Loss

Absorbing Capacity (TLAC). Under the proposed rules, U.S. G-

SIBs would be required to have a minimum TLAC amount

(consisting of CET1 capital and additional tier 1 capital issued

directly by the top-tier or covered BHC plus eligible external

long-term debt) equal to the greater of (i) 18% of RWAs and (ii)

9.5% of total leverage exposure (the denominator of the SLR

calculation). Additionally, U.S. G-SIBs would be required to

maintain a TLAC buffer equal to 2.5% of RWAs plus the firm’s

applicable G-SIB capital surcharge calculated under method one

plus any applicable countercyclical buffer that would be added to

the 18% minimum in order to avoid restrictions on capital

distributions and discretionary bonus payments. The proposed

rules would also require U.S. G-SIBs to have a minimum amount

of eligible unsecured long-term debt equal to the greater of (i)

6.0% of RWAs plus the firm’s applicable G-SIB capital surcharge

calculated under method two and (ii) 4.5% of the total leverage

exposure. In addition, the proposed rules would impose certain

restrictions on the operations and liabilities of the top-tier or

covered BHC in order to further facilitate an orderly resolution,

including prohibitions on the issuance of short-term debt to

external investors and on entering into derivatives and certain

other types of financial contracts with external counterparties.

The proposed rules were open for comments until

February 1, 2016. If the proposed rules are finalized as proposed,

we may be required to issue additional long-term debt. We

continue to evaluate the impact this proposal will have on our

consolidated financial statements.

In addition, as discussed in the “Risk Management –

Asset/Liability Management – Liquidity and Funding –

Liquidity Standards” section in this Report, a final rule

regarding the U.S. implementation of the Basel III LCR was

issued by the FRB, OCC and FDIC in September 2014.

Capital Planning and Stress Testing

Our planned long-term capital structure is designed to meet

regulatory and market expectations. We believe that our long-

term targeted capital structure enables us to invest in and grow

our business, satisfy our customers' financial needs in varying

environments, access markets, and maintain flexibility to return

capital to our shareholders. Our long-term targeted capital

structure also considers capital levels sufficient to exceed Basel

III capital requirements including the G-SIB surcharge.

Accordingly, based on the final Basel III capital rules under the

lower of the Standardized or Advanced Approaches CET1 capital

ratios, we currently target a long-term CET1 capital ratio at or in

excess of 10%, which assumes a 2% G-SIB surcharge. Our capital

targets are subject to change based on various factors, including

changes to the regulatory capital framework and expectations for

large banks promulgated by bank regulatory agencies, planned

capital actions, changes in our risk profile and other factors.

Under the FRB’s capital plan rule, large BHCs are required

to submit capital plans annually for review to determine if the

FRB has any objections before making any capital distributions.

The rule requires updates to capital plans in the event of

material changes in a BHC’s risk profile, including as a result of

any significant acquisitions. The FRB assesses the overall

financial condition, risk profile, and capital adequacy of BHCs

while considering both quantitative and qualitative factors when

evaluating capital plans.

Our 2015 CCAR, which was submitted on January 2, 2015,

included a comprehensive capital plan supported by an

assessment of expected sources and uses of capital over a given

planning horizon under a range of expected and stress scenarios,

similar to the process the FRB used to conduct the CCAR in

2014. As part of the 2015 CCAR, the FRB also generated a

supervisory stress test, which assumed a sharp decline in the

economy and significant decline in asset pricing using the

information provided by the Company to estimate performance.

The FRB reviewed the supervisory stress results both as required

under the Dodd-Frank Act using a common set of capital actions

for all large BHCs and by taking into account the Company’s

proposed capital actions. The FRB published its supervisory

stress test results as required under the Dodd-Frank Act on

March 5, 2015. On March 11, 2015, the FRB notified us that it did

not object to our capital plan included in the 2015 CCAR. The

Wells Fargo & Company

106