Wells Fargo 2015 Annual Report Download - page 218

Download and view the complete annual report

Please find page 218 of the 2015 Wells Fargo annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

208 -

209

209 -

210

210 -

211

211 -

212

212 -

213

213 -

214

214 -

215

215 -

216

216 -

217

217 -

218

218 -

219

219 -

220

220 -

221

221 -

222

222 -

223

223 -

224

224 -

225

225 -

226

226 -

227

227 -

228

228 -

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

|

|

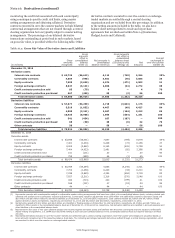

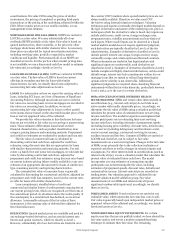

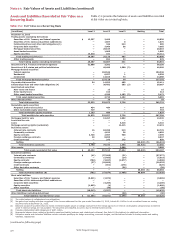

Note 17: Fair Values of Assets and Liabilities

We use fair value measurements to record fair value adjustments

to certain assets and liabilities and to determine fair value

disclosures. Assets and liabilities recorded at fair value on a

recurring basis are presented in the recurring table in this Note.

From time to time, we may be required to record at fair value

other assets on a nonrecurring basis, such as certain residential

and commercial MHFS, certain LHFS, loans held for investment,

nonmarketable equity investments and certain other assets.

These nonrecurring fair value adjustments typically involve

application of LOCOM accounting or write-downs of individual

assets.

Following is a discussion of the fair value hierarchy and the

valuation methodologies used for assets and liabilities recorded

at fair value on a recurring or nonrecurring basis and for

estimating fair value for financial instruments not recorded at

fair value.

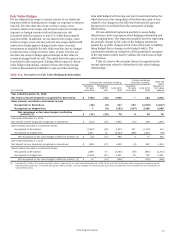

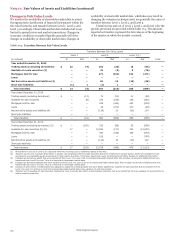

Fair Value Hierarchy

We group our assets and liabilities measured at fair value in

three levels based on the markets in which the assets and

liabilities are traded and the reliability of the assumptions used

to determine fair value. These levels are:

• Level 1 – Valuation is based upon quoted prices for identical

instruments traded in active markets.

• Level 2 – Valuation is based upon quoted prices for similar

instruments in active markets, quoted prices for identical or

similar instruments in markets that are not active, and

model-based valuation techniques for which all significant

assumptions are observable in the market.

• Level 3 – Valuation is generated from techniques that use

significant assumptions that are not observable in the

market. These unobservable assumptions reflect estimates

of assumptions that market participants would use in

pricing the asset or liability. Valuation techniques include

use of option pricing models, discounted cash flow models

and similar techniques.

In the determination of the classification of financial

instruments in Level 2 or Level 3 of the fair value hierarchy, we

consider all available information, including observable market

data, indications of market liquidity and orderliness, and our

understanding of the valuation techniques and significant inputs

used. For securities in inactive markets, we use a predetermined

percentage to evaluate the impact of fair value adjustments

derived from weighting both external and internal indications of

value to determine if the instrument is classified as Level 2 or

Level 3. Otherwise, the classification of Level 2 or Level 3 is

based upon the specific facts and circumstances of each

instrument or instrument category and judgments are made

regarding the significance of the Level 3 inputs to the

instruments’ fair value measurement in its entirety. If Level 3

inputs are considered significant, the instrument is classified as

Level 3.

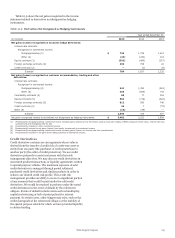

Assets

SHORT-TERM FINANCIAL ASSETS Short-term financial assets

include cash and due from banks, federal funds sold and

securities purchased under resale agreements and due from

customers on acceptances. These assets are carried at historical

cost. The carrying amount is a reasonable estimate of fair value

because of the relatively short time between the origination of

the instrument and its expected realization.

TRADING ASSETS (EXCLUDING DERIVATIVES) AND

INVESTMENT SECURITIES Trading assets and available-for-

sale securities are recorded at fair value on a recurring basis.

Other investment securities classified as held-to-maturity are

subject to impairment and fair value measurement if fair value

declines below amortized cost and we do not expect to recover

the entire amortized cost basis of the debt security. Fair value

measurement is based upon various sources of market pricing.

We use quoted prices in active markets, where available, and

classify such instruments within Level 1 of the fair value

hierarchy. Examples include exchange-traded equity securities

and some highly liquid government securities, such as U.S.

Treasuries. When instruments are traded in secondary markets

and quoted market prices do not exist for such securities, we

generally rely on internal valuation techniques or on prices

obtained from vendors (predominantly third-party pricing

services), and accordingly, we classify these instruments as Level

2 or 3.

Trading securities are mostly valued using internal trader

prices that are subject to price verification procedures performed

by separate internal personnel. The majority of fair values

derived using internal valuation techniques are verified against

multiple pricing sources, including prices obtained from third-

party vendors. Vendors compile prices from various sources and

often apply matrix pricing for similar securities when no price is

observable. We review pricing methodologies provided by the

vendors in order to determine if observable market information

is being used versus unobservable inputs. When evaluating the

appropriateness of an internal trader price compared with

vendor prices, considerations include the range and quality of

vendor prices. Vendor prices are used to ensure the

reasonableness of a trader price; however, valuing financial

instruments involves judgments acquired from knowledge of a

particular market. If a trader asserts that a vendor price is not

reflective of market value, justification for using the trader price,

including recent sales activity where possible, must be provided

to and approved by the appropriate levels of management.

Similarly, while investment securities traded in secondary

markets are typically valued using unadjusted vendor prices or

vendor prices adjusted by weighting them with internal

discounted cash flow techniques, these prices are reviewed and,

if deemed inappropriate by a trader who has the most knowledge

of a particular market, can be adjusted. These investment

securities, which include those measured using unadjusted

vendor prices, are generally classified as Level 2 and typically

involve using quoted market prices for the same or similar

securities, pricing models, discounted cash flow analyses using

significant inputs observable in the market where available or a

combination of multiple valuation techniques. Examples include

certain residential and commercial MBS, other asset-backed

securities municipal bonds, U.S. government and agency MBS,

and corporate debt securities.

Security fair value measurements using significant inputs

that are unobservable in the market due to limited activity or a

less liquid market are classified as Level 3 in the fair value

hierarchy. Such measurements include securities valued using

internal models or a combination of multiple valuation

techniques where the unobservable inputs are significant to the

overall fair value measurement. Securities classified as Level 3

include certain residential and commercial MBS, other asset-

backed securities, CDOs and certain CLOs, and certain residual

and retained interests in residential mortgage loan

Wells Fargo & Company

216