Wells Fargo 2015 Annual Report Download - page 58

Download and view the complete annual report

Please find page 58 of the 2015 Wells Fargo annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

|

|

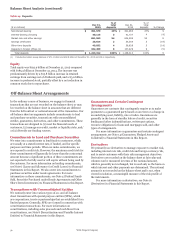

Balance Sheet Analysis (continued)

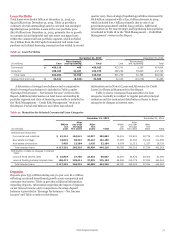

Table 14: Deposits

($ in millions)

Dec 31,

2015

% of

total

deposits

Dec 31,

2014

% of

total

deposits % Change

Noninterest-bearing

Interest-bearing checking

Market rate and other savings

Savings certificates

Other time deposits

Deposits in foreign offices (1)

$ 351,579

40,115

651,563

28,614

49,032

102,409

29%

3

54

2

4

8

$ 321,963

41,737

604,999

35,354

56,828

107,429

27%

4

52

3

5

9

9

(4)

8

(19)

(14)

(5)

Total deposits $ 1,223,312 100% $ 1,168,310 100% 5

(1) Includes Eurodollar sweep balances of $71.1 billion and $69.8 billion at December 31, 2015 and 2014, respectively.

Equity

Total equity was $193.9 billion at December 31, 2015 compared

with $185.3 billion at December 31, 2014. The increase was

predominantly driven by a $13.8 billion increase in retained

earnings from earnings net of dividends paid, and a $3.0 billion

increase in preferred stock, partially offset by a net reduction in

common stock due to repurchases.

Off-Balance Sheet Arrangements

In the ordinary course of business, we engage in financial

transactions that are not recorded on the balance sheet, or may

be recorded on the balance sheet in amounts that are different

from the full contract or notional amount of the transaction. Our

off-balance sheet arrangements include commitments to lend

and purchase securities, transactions with unconsolidated

entities, guarantees, derivatives, and other commitments. These

transactions are designed to (1) meet the financial needs of

customers, (2) manage our credit, market or liquidity risks, and/

or (3) diversify our funding sources.

Commitments to Lend and Purchase Securities

We enter into commitments to lend funds to customers, which

are usually at a stated interest rate, if funded, and for specific

purposes and time periods. When we make commitments, we

are exposed to credit risk. However, the maximum credit risk for

these commitments will generally be lower than the contractual

amount because a significant portion of these commitments are

not expected to be fully used or will expire without being used by

the customer. For more information on lending commitments,

see Note 6 (Loans and Allowance for Credit Losses) to Financial

Statements in this Report. We also enter into commitments to

purchase securities under resale agreements. For more

information on these commitments, see Note 4 (Federal Funds

Sold, Securities Purchased under Resale Agreements and Other

Short-Term Investments) to Financial Statements in this Report.

Transactions with Unconsolidated Entities

We routinely enter into various types of on- and off-balance

sheet transactions with special purpose entities (SPEs), which

are corporations, trusts or partnerships that are established for a

limited purpose. Generally, SPEs are formed in connection with

securitization transactions. For more information on

securitizations, including sales proceeds and cash flows from

securitizations, see Note 8 (Securitizations and Variable Interest

Entities) to Financial Statements in this Report.

Guarantees and Certain Contingent

Arrangements

Guarantees are contracts that contingently require us to make

payments to a guaranteed party based on an event or a change in

an underlying asset, liability, rate or index. Guarantees are

generally in the form of standby letters of credit, securities

lending and other indemnifications, written put options,

recourse obligations for loans and mortgages sold, and other

types of arrangements.

For more information on guarantees and certain contingent

arrangements, see Note 14 (Guarantees, Pledged Assets and

Collateral) to Financial Statements in this Report.

Derivatives

We primarily use derivatives to manage exposure to market risk,

including interest rate risk, credit risk and foreign currency risk,

and to assist customers with their risk management objectives.

Derivatives are recorded on the balance sheet at fair value and

volumes can be measured in terms of the notional amount,

which is generally not exchanged, but is used only as the basis on

which interest and other payments are determined. The notional

amount is not recorded on the balance sheet and is not, when

viewed in isolation, a meaningful measure of the risk profile of

the instruments.

For more information on derivatives, see Note 16

(Derivatives) to Financial Statements in this Report.

Wells Fargo & Company

56