Wells Fargo 2015 Annual Report Download - page 172

Download and view the complete annual report

Please find page 172 of the 2015 Wells Fargo annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

162 -

163

163 -

164

164 -

165

165 -

166

166 -

167

167 -

168

168 -

169

169 -

170

170 -

171

171 -

172

172 -

173

173 -

174

174 -

175

175 -

176

176 -

177

177 -

178

178 -

179

179 -

180

180 -

181

181 -

182

182 -

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

|

|

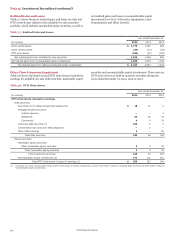

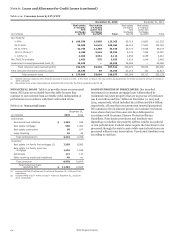

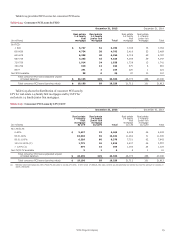

Note 6: Loans and Allowance for Credit Losses (continued)

Table 6.12: Consumer Loans by LTV/CLTV

December 31, 2015 December 31, 2014

Real estate Real estate Real estate Real estate

(in millions)

1-4 family

first

mortgage

by LTV

1-4 family

junior lien

mortgage

by CLTV Total

1-4 family

first

mortgage

by LTV

1-4 family

junior lien

mortgage

by CLTV Total

By LTV/CLTV:

0-60% $ 109,558 15,805 125,363 95,719 15,603 111,322

60.01-80% 92,005 16,579 108,584 86,112 17,651 103,763

80.01-100% 22,765 11,385 34,150 25,170 14,004 39,174

100.01-120% (1) 4,480 5,545 10,025 6,133 7,254 13,387

> 120% (1) 2,065 3,051 5,116 2,856 4,058 6,914

No LTV/CLTV available 1,453 570 2,023 1,416 1,046 2,462

Government insured/guaranteed loans (2) 22,353 — 22,353 26,268 — 26,268

Total consumer loans (excluding PCI) 254,679 52,935 307,614 243,674 59,616 303,290

Total consumer PCI loans (carrying value) 19,190 69 19,259 21,712 101 21,813

Total consumer loans $ 273,869 53,004 326,873 265,386 59,717 325,103

(1) Reflects total loan balances with LTV/CLTV amounts in excess of 100%. In the event of default, the loss content would generally be limited to only the amount in excess of

100% LTV/CLTV.

(2) Represents loans whose repayments are predominantly insured by the FHA or guaranteed by the VA.

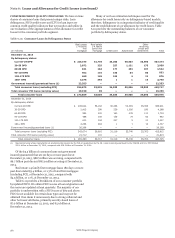

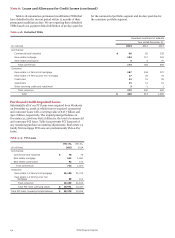

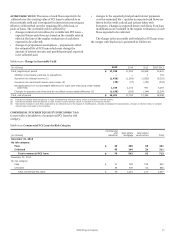

NONACCRUAL LOANS Table 6.13 provides loans on nonaccrual LOANS IN PROCESS OF FORECLOSURE Our recorded

status. PCI loans are excluded from this table because they investment in consumer mortgage loans collateralized by

continue to earn interest from accretable yield, independent of residential real estate property that are in process of foreclosure

performance in accordance with their contractual terms. was $11.0 billion and $12.7 billion at December 31, 2015 and

2014, respectively, which included $6.2 billion and $6.6 billion,

Table 6.13: Nonaccrual Loans respectively, of loans that are government insured/guaranteed.

We commence the foreclosure process on consumer real estate

December 31, loans when a borrower becomes 120 days delinquent in

(in millions) 2015 2014 accordance with Consumer Finance Protection Bureau

Commercial: Guidelines. Foreclosure procedures and timelines vary

Commercial and industrial $ 1,363 538 depending on whether the property address resides in a judicial

or non-judicial state. Judicial states require the foreclosure to be

Real estate mortgage 969 1,490 processed through the state's courts while non-judicial states are

Real estate construction 66 187 processed without court intervention. Foreclosure timelines vary

Lease financing 26 24 according to state law.

Total commercial (1) 2,424 2,239

Consumer:

Real estate 1-4 family first mortgage (2) 7,293 8,583

Real estate 1-4 family junior lien

mortgage 1,495 1,848

Automobile 121 137

Other revolving credit and installment 49 41

Total consumer 8,958 10,609

Total nonaccrual loans

(excluding PCI) $ 11,382 12,848

(1) Includes LHFS of $0 million and $1 million at December 31, 2015 and 2014,

respectively.

(2) Includes MHFS of $177 million and $177 million at December 31, 2015 and

2014, respectively.

Wells Fargo & Company

170