Wells Fargo 2015 Annual Report Download - page 233

Download and view the complete annual report

Please find page 233 of the 2015 Wells Fargo annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

223 -

224

224 -

225

225 -

226

226 -

227

227 -

228

228 -

229

229 -

230

230 -

231

231 -

232

232 -

233

233 -

234

234 -

235

235 -

236

236 -

237

237 -

238

238 -

239

239 -

240

240 -

241

241 -

242

242 -

243

243 -

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

|

|

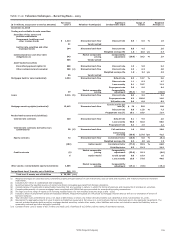

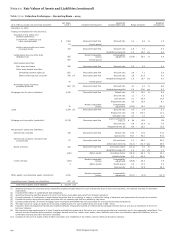

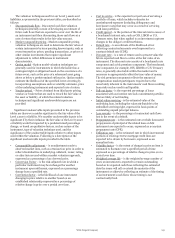

The valuation techniques used for our Level 3 assets and • Cost to service - is the expected cost per loan of servicing a

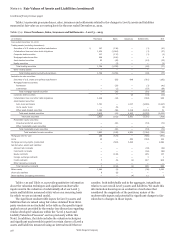

liabilities, as presented in the previous tables, are described as portfolio of loans, which includes estimates for

follows: unreimbursed expenses (including delinquency and

• Discounted cash flow - Discounted cash flow valuation foreclosure costs) that may occur as a result of servicing

techniques generally consist of developing an estimate of such loan portfolios.

future cash flows that are expected to occur over the life of • Credit spread – is the portion of the interest rate in excess of

an instrument and then discounting those cash flows at a a benchmark interest rate, such as OIS, LIBOR or U.S.

rate of return that results in the fair value amount. Treasury rates, that when applied to an investment captures

• Market comparable pricing - Market comparable pricing changes in the obligor’s creditworthiness.

valuation techniques are used to determine the fair value of • Default rate – is an estimate of the likelihood of not

certain instruments by incorporating known inputs, such as collecting contractual amounts owed expressed as a

recent transaction prices, pending transactions, or prices of constant default rate (CDR).

other similar investments that require significant • Discount rate – is a rate of return used to present value the

adjustment to reflect differences in instrument future expected cash flow to arrive at the fair value of an

characteristics. instrument. The discount rate consists of a benchmark rate

• Option model - Option model valuation techniques are component and a risk premium component. The benchmark

generally used for instruments in which the holder has a rate component, for example, OIS, LIBOR or U.S. Treasury

contingent right or obligation based on the occurrence of a rates, is generally observable within the market and is

future event, such as the price of a referenced asset going necessary to appropriately reflect the time value of money.

above or below a predetermined strike price. Option models The risk premium component reflects the amount of

estimate the likelihood of the specified event occurring by compensation market participants require due to the

incorporating assumptions such as volatility estimates, price uncertainty inherent in the instruments’ cash flows resulting

of the underlying instrument and expected rate of return. from risks such as credit and liquidity.

• Vendor-priced – Prices obtained from third party pricing • Fall-out factor - is the expected percentage of loans

vendors or brokers that are used to record the fair value of associated with our interest rate lock commitment portfolio

the asset or liability, of which the related valuation that are likely of not funding.

technique and significant unobservable inputs are not • Initial-value servicing - is the estimated value of the

provided. underlying loan, including the value attributable to the

embedded servicing right, expressed in basis points of

Significant unobservable inputs presented in the previous outstanding unpaid principal balance.

tables are those we consider significant to the fair value of the • Loss severity – is the percentage of contractual cash flows

Level 3 asset or liability. We consider unobservable inputs to be lost in the event of a default.

significant if by their exclusion the fair value of the Level 3 asset • Prepayment rate – is the estimated rate at which forecasted

or liability would be impacted by a predetermined percentage prepayments of principal of the related loan or debt

change, or based on qualitative factors, such as nature of the instrument are expected to occur, expressed as a constant

instrument, type of valuation technique used, and the prepayment rate (CPR).

significance of the unobservable inputs relative to other inputs • Utilization rate – is the estimated rate in which incremental

used within the valuation. Following is a description of the portions of existing reverse mortgage credit lines are

significant unobservable inputs provided in the table. expected to be drawn by borrowers, expressed as an

annualized rate.

• Comparability adjustment – is an adjustment made to • Volatility factor – is the extent of change in price an item is

observed market data, such as a transaction price in order to estimated to fluctuate over a specified period of time

reflect dissimilarities in underlying collateral, issuer, rating, expressed as a percentage of relative change in price over a

or other factors used within a market valuation approach, period over time.

expressed as a percentage of an observed price. • Weighted average life – is the weighted average number of

• Conversion Factor – is the risk-adjusted rate in which a years an investment is expected to remain outstanding

particular instrument may be exchanged for another based on its expected cash flows reflecting the estimated

instrument upon settlement, expressed as a percentage date the issuer will call or extend the maturity of the

change from a specified rate. instrument or otherwise reflecting an estimate of the timing

• Correlation factor - is the likelihood of one instrument of an instrument’s cash flows whose timing is not

changing in price relative to another based on an contractually fixed.

established relationship expressed as a percentage of

relative change in price over a period over time.

Wells Fargo & Company

231