Wells Fargo 2015 Annual Report Download - page 43

Download and view the complete annual report

Please find page 43 of the 2015 Wells Fargo annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

|

|

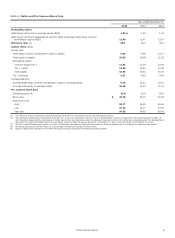

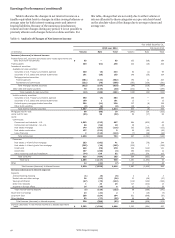

Noninterest Income

Table 7: Noninterest Income

(in millions)

Y

2015

ear ended Dec

2014

ember 31,

2013

Service charges on deposit accounts $ 5,168 5,050 5,023

Trust and investment fees:

Brokerage advisory, commissions

and other fees 9,435 9,183 8,395

Trust and investment management 3,394 3,387 3,289

Investment banking 1,639 1,710 1,746

Total trust and investment fees 14,468 14,280 13,430

Card fees 3,720 3,431 3,191

Other fees:

Charges and fees on loans 1,228 1,316 1,540

Merchant processing fees (1) 607 726 669

Cash network fees 522 507 493

Commercial real estate

brokerage commissions 618 469 338

Letters of credit fees 353 390 410

All other fees 996 941 890

Total other fees 4,324 4,349 4,340

Mortgage banking:

Servicing income, net 2,441 3,337 1,920

Net gains on mortgage loan

origination/sales activities 4,060 3,044 6,854

Total mortgage banking 6,501 6,381 8,774

Insurance 1,694 1,655 1,814

Net gains from trading activities 614 1,161 1,623

Net gains (losses) on debt securities 952 593 (29)

Net gains from equity investments 2,230 2,380 1,472

Lease income 621 526 663

Life insurance investment income 579 558 566

All other (1) (115) 456 113

Total $ 40,756 40,820 40,980

(1) Reflects deconsolidation of the Company's merchant services joint venture in

fourth quarter 2015. The Company's proportionate share of earnings is now

reflected in all other income.

Noninterest income of $40.8 billion represented 47% of revenue

for 2015, compared with $40.8 billion, or 48%, for 2014 and

$41.0 billion, or 49%, for 2013. The small decline in noninterest

income in 2015 was primarily driven by lower gains from trading

activity and all other income, mostly offset by growth in many of

our businesses, including credit and debit cards, mortgage,

commercial banking, commercial real estate brokerage, multi-

family capital, reinsurance, municipal products, and retail

brokerage. The decrease in noninterest income in 2014

compared with 2013 was primarily due to a decline in mortgage

banking, partially offset by growth in many of our other

businesses.

Service charges on deposit accounts were $5.2 billion in

2015, up from $5.1 billion in 2014 due to account growth, higher

commercial deposit product sales and commercial deposit

product re-pricing, partially offset by lower overdraft fees driven

by changes we implemented in early October 2014. Service

charges on deposits increased $27 million in 2014 from 2013 due

to account growth, new commercial deposit product sales and

commercial deposit product re-pricing, partially offset by lower

overdraft fees driven by changes we implemented in early

October 2014 designed to provide customers with more real time

information to manage their deposit accounts and avoid

overdrafts.

Brokerage advisory, commissions and other fees are

received for providing full-service and discount brokerage

services predominantly to retail brokerage clients. Income from

these brokerage-related activities include asset-based fees for

advisory accounts, which are based on the market value of the

client’s assets, and transactional commissions based on the

number and size of transactions executed at the client’s

direction. These fees increased to $9.4 billion in 2015, from

$9.2 billion and $8.4 billion in 2014 and 2013, respectively. The

increase in these fees for 2015 was primarily due to growth in

asset-based fees driven by higher average advisory account

assets in 2015 than 2014. The increase for 2014 was

predominantly due to higher asset-based fees as a result of

higher market values and growth in advisory account assets.

Retail brokerage client assets totaled $1.39 trillion at

December 31, 2015, compared with $1.42 trillion and

$1.36 trillion at December 31, 2014 and 2013, respectively, with

all retail brokerage services provided by our Wealth and

Investment Management (WIM) operating segment. For

additional information on retail brokerage client assets, see the

discussion and Tables 9d and 9e in the "Operating Segment

Results – Wealth and Investment Management – Retail

Brokerage Client Assets" section in this Report.

We earn trust and investment management fees from

managing and administering assets, including mutual funds,

institutional separate accounts, corporate trust, personal trust,

employee benefit trust and agency assets. Trust and investment

management fee income is predominantly from client assets

under management (AUM) for which the fees are determined

based on a tiered scale relative to the market value of the AUM.

AUM consists of assets for which we have investment

management discretion. Our AUM totaled $653.4 billion at

December 31, 2015, compared with $661.6 billion and

$647.2 billion at December 31, 2014 and 2013, respectively, with

substantially all of our AUM managed by our WIM operating

segment. Additional information regarding our WIM operating

segment AUM is provided in Table 9f and the related discussion

in the "Operating Segment Results – Wealth and Investment

Management – Trust and Investment Client Assets Under

Management" section in this Report. In addition to AUM we

have client assets under administration (AUA) that earn various

administrative fees which are generally based on the extent of

the services provided to administer the account. Our AUA

totaled $1.4 trillion at December 31, 2015, compared with

$1.5 trillion and $1.4 trillion at December 31, 2014 and 2013,

respectively. Trust and investment management fees of

$3.4 billion in 2015 remained stable compared with 2014, but

increased $98 million in 2014 compared with 2013, substantially

due to growth in AUM reflecting higher market values.

We earn investment banking fees from underwriting debt

and equity securities, arranging loan syndications, and

performing other related advisory services. Investment banking

fees decreased to $1.6 billion in 2015 from $1.7 billion in 2014,

driven by reductions in equity capital markets and loan

syndications partially offset by increased fees in advisory

services and investment-grade debt origination. Investment

banking fees remained unchanged at $1.7 billion in 2014

compared with 2013 as higher advisory services results were

offset by lower loan syndication and origination fees.

Card fees were $3.7 billion in 2015, compared with

$3.4 billion in 2014 and $3.2 billion in 2013. Card fees increased

in 2015 and 2014 primarily due to account growth and increased

purchase activity.

Other fees of $4.3 billion in 2015 were unchanged compared

with 2014 as increases in commercial real estate brokerage

commissions were offset by lower charges and fees on loans

primarily due to the phase out of the direct deposit advance

product during the first half of 2014, and lower merchant

processing fees. The decrease in merchant processing fees

reflected deconsolidation of our merchant services joint venture

in fourth quarter 2015, which resulted in our proportionate

Wells Fargo & Company

41