MetLife 2008 Annual Report Download - page 62

Download and view the complete annual report

Please find page 62 of the 2008 MetLife annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

|

|

Liquidity and Capital

Liquidity and capital are managed to preserve stable, reliable and cost-effective sources of cash to meet all current and future financial

obligations and are provided by a variety of sources, including a portfolio of liquid assets, a diversified mix of short- and long-term funding

sources from the wholesale financial markets and the ability to borrow through committed credit facilities. The Holding Company is an

active participant in the global financial markets through which it obtains a significant amount of funding. These markets, which serve as

cost-effective sources of funds, are critical components of the Holding Company’s liquidity and capital management. Decisions to access

these markets are based upon relative costs, prospective views of balance sheet growth and a targeted liquidity profile and capital

structure. A disruption in the financial markets could limit the Holding Company’s access to liquidity. See “Extraordinary Market Conditions.”

The Holding Company’s ability to maintain regular access to competitively priced wholesale funds is fostered by its current high credit

ratings from the major credit rating agencies. Management views its capital ratios, credit quality, stable and diverse earnings streams,

diversity of liquidity sources and its liquidity monitoring procedures as critical to retaining high credit ratings. See “The Company —

Capital — Rating Agencies.”

Liquidity is monitored through the use of internal liquidity risk metrics, including the composition and level of the liquid asset portfolio,

timing differences in short-term cash flow obligations, access to the financial markets for capital and debt transactions and exposure to

contingent draws on the Holding Company’s liquidity.

Liquidity and Capital Sources

Dividends. The primary source of the Holding Company’s liquidity is dividends it receives from its insurance subsidiaries. The Holding

Company’s insurance subsidiaries are subject to regulatory restrictions on the payment of dividends imposed by the regulators of their

respective domiciles. The dividend limitation for U.S. insurance subsidiaries is generally based on the surplus to policyholders as of the

immediately preceding calendar year and statutory net gain from operations for the immediately preceding calendar year. Statutory

accounting practices, as prescribed by insurance regulators of various states in which the Company conducts business, differ in certain

respects from accounting principles used in financial statements prepared in conformity with GAAP. The significant differences relate to the

treatment of DAC, certain deferred income tax, required investment reserves, reserve calculation assumptions, goodwill and surplus notes.

Management of the Holding Company cannot provide assurances that the Holding Company’s insurance subsidiaries will have statutory

earnings to support payment of dividends to the Holding Company in an amount sufficient to fund its cash requirements and pay cash

dividends and that the applicable insurance departments will not disapprove any dividends that such insurance subsidiaries must submit

for approval.

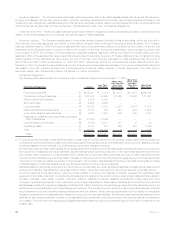

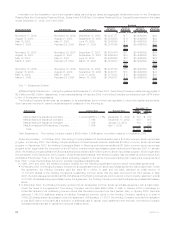

The table below sets forth the dividends permitted to be paid by the respective insurance subsidiary without insurance regulatory

approval and the respective dividends paid:

Company Permitted w/o

Approval(1) Paid(2) Permitted w/o

Approval(3) Paid(2) Permitted w/o

Approval(3)

2009 2008 2007

(In millions)

MetropolitanLifeInsuranceCompany .............. $552 $1,318(4) $1,299 $500 $919

MetLife Insurance Company of Connecticut . . . . . . . . . . $714 $ 500 $1,026 $690(6) $690

MetropolitanTowerLifeInsuranceCompany.......... $ 88 $ 277(5) $ 113 $ — $104

Metropolitan Property and Casualty Insurance Company . . $ 9 $ 300 $ — $400 $ 16

(1) Reflects dividend amounts that may be paid during 2009 without prior regulatory approval. However, if paid before a specified date during

2009, some or all of such dividends may require regulatory approval.

(2) Includes amounts paid including those requiring regulatory approval.

(3) Reflects dividend amounts that could have been paid during the relevant year without prior regulatory approval.

(4) Consists of shares of RGA stock distributed by Metropolitan Life Insurance Company to the Holding Company as an in-kind dividend of

$1,318 million.

(5) Includes shares of an affiliate distributed to the Holding Company as an in-kind dividend of $164 million.

(6) Includes a return of capital of $404 million as approved by the applicable insurance department, of which $350 million was paid to the

Holding Company.

In the fourth quarter of 2008, MICC declared and paid an ordinary dividend of $500 million to the Holding Company. In the third quarter

of 2008, MLIC used its otherwise ordinary dividend capacity through a non-cash dividend in conjunction with the RGA split-off as approved

by the New York Insurance Commissioner.

Under New York State Insurance Law, MLIC is permitted, without prior insurance regulatory clearance, to pay stockholder dividends to

the Holding Company as long as the aggregate amount of all such dividends in any calendar year does not exceed the lesser of: (i) 10% of

its surplus to policyholders as of the end of the immediately preceding calendar year; or (ii) its statutory net gain from operations for the

immediately preceding calendar year (excluding realized capital gains). MLIC will be permitted to pay a cash dividend to the Holding

Company in excess of the lesser of such two amounts only if it files notice of its intention to declare such a dividend and the amount thereof

with the Superintendent and the Superintendent does not disapprove the distribution within 30 days of its filing.

For the year ended December 31, 2008, $235 million in dividends from other subsidiaries were paid to the Holding Company. For the

year ended December 31, 2007, $190 million in dividends from other subsidiaries were paid, of which $176 million were returns of capital,

to the Holding Company.

Liquid Assets. An integral part of the Holding Company’s liquidity management is the amount of liquid assets it holds. Liquid assets

include cash, cash equivalents, short-term investments and publicly-traded securities. Liquid assets exclude cash collateral received

under the Company’s securities lending program that has been reinvested in cash, cash equivalents, short-term investments and publicly-

traded securities. At December 31, 2008 and 2007, the Holding Company had $2.7 billion and $2.3 billion in liquid assets, respectively. At

December 31, 2008, the Holding Company had pledged $0.8 billion of liquid assets under collateral support agreements as described in

59MetLife, Inc.