MetLife 2008 Annual Report Download - page 154

Download and view the complete annual report

Please find page 154 of the 2008 MetLife annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

151 -

152

152 -

153

153 -

154

154 -

155

155 -

156

156 -

157

157 -

158

158 -

159

159 -

160

160 -

161

161 -

162

162 -

163

163 -

164

164 -

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

|

|

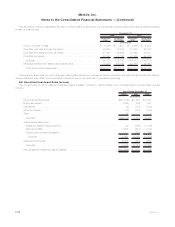

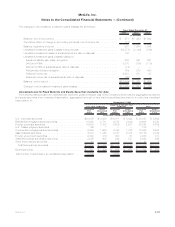

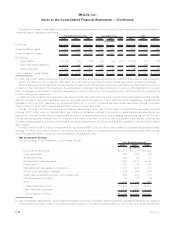

Concentrations of Credit Risk (Fixed Maturity Securities) — Residential Mortgage-Backed Securities. The Company’s residential

mortgage-backed securities consist of the following holdings at:

Estimated

Fair Value %of

Total Estimated

Fair Value %of

Total

2008 2007

December 31,

(In millions)

Residential mortgage-backed securities:

Collateralizedmortgageobligations............................ $26,025 72.2% $36,303 66.0%

Pass-throughsecurities ................................... 10,003 27.8 18,692 34.0

Total residential mortgage-backed securities . . . . . . . . . . . . . . . . . . . . . . . $36,028 100.0% $54,995 100.0%

Collateralized mortgage obligations are a type of mortgage-backed security that creates separate pools or tranches of pass-through

cash flows for different classes of bondholders with varying maturities. Pass-through mortgage-backed securities are a type of asset-

backed security that is secured by a mortgage or collection of mortgages. The monthly mortgage payments from homeowners pass from

the originating bank through an intermediary, such as a government agency or investment bank, which collects the payments, and for fee,

remits or passes these payments through to the holders of the pass-through securities.

At December 31, 2008, the exposures in the Company’s residential mortgage-backed securities portfolio consist of agency, prime, and

alternative residential mortgage loans (“Alt-A”) securities of 68%, 23%, and 9% of the total holdings, respectively. At December 31, 2008

and 2007, $33.3 billion and $54.7 billion, respectively, or 92% and 99% respectively of the residential mortgage-backed securities were

rated Aaa/AAA by Moody’s Investors Service (“Moody’s”), S&P, or Fitch Ratings (“Fitch”). The majority of the agency residential mortgage-

backed securities are guaranteed or otherwise supported by the Federal National Mortgage Association, the Federal Home Loan Mortgage

Corporation or the Government National Mortgage Association. Prime residential mortgage lending includes the origination of residential

mortgage loans to the most credit-worthy customers with high quality credit profiles. Alt-A residential mortgage loans are a classification of

mortgage loans where the risk profile of the borrower falls between prime and sub-prime. At December 31, 2008 and 2007, the Company’s

Alt-A residential mortgage-backed securities exposure was $3.4 billion and $6.3 billion, respectively, with an unrealized loss of $1,963 mil-

lion and $139 million, respectively. At December 31, 2008 and December 31, 2007, $2.1 billion and $6.3 billion, respectively, or 63% and

99%, respectively, of the Company’s Alt-A residential mortgage-backed securities were rated Aa/AA or better by Moody’s, S&P or Fitch. In

December 2008, certain Alt-A residential mortgage-backed securities experienced ratings downgrades from investment grade to below

investment grade, contributing to the decrease year over year cited above in those securities rated Aa/AA or better. At December 31, 2008

the Company’s Alt-A holdings are distributed as follows: 23% 2007 vintage year, 25% 2006 vintage year; and 52% in the 2005 and prior

vintage years. In January 2009, Moody’s revised its loss projections for Alt-A residential mortgage-backed securities, and the Company

anticipates that Moody’s will be downgrading virtually all 2006 and 2007 vintage year Alt-A securities to below investment grade, which will

increase the percentage of our Alt-A residential mortgage-backed securities portfolio that will be rated below investment grade. Vintage

year refers to the year of origination and not to the year of purchase.

Concentrations of Credit Risk (Fixed Maturity Securities) — Commercial Mortgage-Backed Securities. At December 31, 2008 and

2007, the Company’s holdings in commercial mortgage-backed securities was $12.6 billion and $17.0 billion, respectively, at estimated

fair value. At December 31, 2008 and 2007, $11.8 billion and $14.9 billion, respectively, of the estimated fair value, or 93% and 88%,

respectively, of the commercial mortgage-backed securities were rated Aaa/AAA by Moody’s, S&P, or Fitch. At December 31, 2008, the

rating distribution of the Company’s commercial mortgage-backed securities holdings was as follows: 93% Aaa, 4% Aa, 1% A, 1% Baa, and

1% Ba or below. At December 31, 2008, 84% of the holdings are in the 2005 and prior vintage years. At December 31, 2008, the Company

had no exposure to CMBX securities and its holdings of commercial real estate collateralized debt obligations (“CRE-CDO”) securities was

$121 million at estimated fair value.

Concentrations of Credit Risk (Fixed Maturity Securities) — Asset-Backed Securities. At December 31, 2008 and 2007, the

Company’s holdings in asset-backed securities was $10.5 billion and $10.6 billion, respectively, at estimated fair value. The Company’s

asset-backed securities are diversified both by sector and by issuer. At December 31, 2008 and 2007, $7.9 billion and $5.7 billion,

respectively, or 75% and 54%, respectively, of total asset-backed securities were rated Aaa/AAA by Moody’s, S&P or Fitch. At

December 31, 2008, the largest exposures in the Company’s asset-backed securities portfolio were credit card receivables, residential

mortgage-backed securities backed by sub-prime mortgage loans, automobile receivables and student loan receivables of 49%, 10%,

10% and 10% of the total holdings, respectively. Sub-prime mortgage lending is the origination of residential mortgage loans to customers

with weak credit profiles. At December 31, 2008 and 2007, the Company had exposure to fixed maturity securities backed by sub-prime

mortgage loans with estimated fair values of $1.1 billion and $2.0 billion, respectively, and unrealized losses of $730 million and

$198 million, respectively. At December 31, 2008, 37% of the asset-backed securities backed by sub-prime mortgage loans have been

guaranteed by financial guarantee insurers, of which 19% and 37% were guaranteed by financial guarantee insurers who were Aa and Baa

rated, respectively.

Concentrations of Credit Risk (Equity Securities). The Company is not exposed to any concentrations of credit risk of any single issuer

greater than 10% of the Company’s stockholders’ equity in its equity securities holdings.

F-31MetLife, Inc.

MetLife, Inc.

Notes to the Consolidated Financial Statements — (Continued)