MetLife 2008 Annual Report Download - page 16

Download and view the complete annual report

Please find page 16 of the 2008 MetLife annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

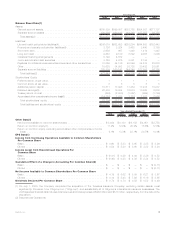

|

|

When available, the estimated fair value of securities is based on quoted prices in active markets that are readily and regularly

obtainable. Generally, these are the most liquid of the Company’s securities holdings and valuation of these securities does not involve

management judgment.

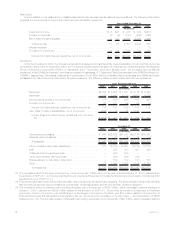

When quoted prices in active markets are not available, the determination of estimated fair value is based on market standard valuation

methodologies. The market standard valuation methodologies utilized include: discounted cash flow methodologies, matrix pricing or other

similar techniques. The assumptions and inputs in applying these market standard valuation methodologies include, but are not limited to:

interest rates, credit standing of the issuer or counterparty, industry sector of the issuer, coupon rate, call provisions, sinking fund

requirements, maturity, estimated duration and management’s assumptions regarding liquidity and estimated future cash flows. Accord-

ingly, the estimated fair values are based on available market information and management’s judgments about financial instruments.

The significant inputs to the market standard valuation methodologies for certain types of securities with reasonable levels of price

transparency are inputs that are observable in the market or can be derived principally from or corroborated by observable market data.

Such observable inputs include benchmarking prices for similar assets in active, liquid markets, quoted prices in markets that are not active

and observable yields and spreads in the market.

When observable inputs are not available, the market standard valuation methodologies for determining the estimated fair value of certain

types of securities that trade infrequently, and therefore have little or no price transparency, rely on inputs that are significant to the estimated

fair value that are not observable in the market or cannot be derived principally from or corroborated by observable market data. These

unobservable inputs can be based in large part on management judgment or estimation, and cannot be supported by reference to market

activity. Even though unobservable, these inputs are based on assumptions deemed appropriate given the circumstances and consistent

with what other market participants would use when pricing such securities.

The estimated fair value of residential mortgage loans held-for-sale are determined based on observable pricing of residential mortgage

loans held-for-sale with similar characteristics, or observable pricing for securities backed by similar types of loans, adjusted to convert the

securities prices to loan prices. Generally, quoted market prices are not available. When observable pricing for similar loans or securities

that are backed by similar loans are not available, the estimated fair values of residential mortgage loans held-for-sale are determined using

independent broker quotations, which is intended to approximate the amounts that would be received from third parties. Certain other

mortgages have also been designated as held-for-sale which are recorded at the lower of amortized cost or estimated fair value less

expected disposition costs determined on an individual loan basis. For these loans, estimated fair value is determined using independent

broker quotations or, when the loan is in foreclosure or otherwise determined to be collateral dependent, the estimated fair value of the

underlying collateral estimated using internal models.

Mortgage servicing rights (“MSRs”) are measured at estimated fair value and are either acquired or are generated from the sale of

originated residential mortgage loans where the servicing rights are retained by the Company. The estimated fair value of MSRs is

principally determined through the use of internal discounted cash flow models which utilize various assumptions as to discount rates,

loan-prepayments, and servicing costs. The use of different valuation assumptions and inputs as well as assumptions relating to the

collection of expected cash flows may have a material effect on MSRs estimated fair values.

Financial markets are susceptible to severe events evidenced by rapid depreciation in asset values accompanied by a reduction in

asset liquidity. The Company’s ability to sell securities, or the price ultimately realized for these securities, depends upon the demand and

liquidity in the market and increases the use of judgment in determining the estimated fair value of certain securities.

Investment Impairments

One of the significant estimates related to available-for-sale securities is the evaluation of investments for other-than-temporary

impairments. The assessment of whether impairments have occurred is based on management’s case-by-case evaluation of the

underlying reasons for the decline in estimated fair value. The Company’s review of its fixed maturity and equity securities for impairments

includes an analysis of the total gross unrealized losses by three categories of securities: (i) securities where the estimated fair value had

declined and remained below cost or amortized cost by less than 20%; (ii) securities where the estimated fair value had declined and

remained below cost or amortized cost by 20% or more for less than six months; and (iii) securities where the estimated fair value had

declined and remained below cost or amortized cost by 20% or more for six months or greater. An extended and severe unrealized loss

position on a fixed maturity security may not have any impact on the ability of the issuer to service all scheduled interest and principal

payments and the Company’s evaluation of recoverability of all contractual cash flows, as well as the Company’s ability and intent to hold

the security, including holding the security until the earlier of a recovery in value, or until maturity. In contrast, for certain equity securities,

greater weight and consideration are given by the Company to a decline in estimated fair value and the likelihood such estimated fair value

decline will recover.

Additionally, management considers a wide range of factors about the security issuer and uses its best judgment in evaluating the

cause of the decline in the estimated fair value of the security and in assessing the prospects for near-term recovery. Inherent in

management’s evaluation of the security are assumptions and estimates about the operations of the issuer and its future earnings potential.

Considerations used by the Company in the impairment evaluation process include, but are not limited to:

(i) the length of time and the extent to which the estimated fair value has been below cost or amortized cost;

(ii) the potential for impairments of securities when the issuer is experiencing significant financial difficulties;

(iii) the potential for impairments in an entire industry sector or sub-sector;

(iv) the potential for impairments in certain economically depressed geographic locations;

(v) the potential for impairments of securities where the issuer, series of issuers or industry has suffered a catastrophic type of

loss or has exhausted natural resources;

(vi) the Company’s ability and intent to hold the security for a period of time sufficient to allow for the recovery of its value to an

amount equal to or greater than cost or amortized cost;

(vii) unfavorable changes in forecasted cash flows on mortgage-backed and asset-backed securities; and

(viii) other subjective factors, including concentrations and information obtained from regulators and rating agencies.

The cost of fixed maturity and equity securities is adjusted for impairments in value deemed to be other-than temporary in the period in

which the determination is made. These impairments are included within net investment gains (losses) and the cost basis of the fixed

13MetLife, Inc.