MetLife 2008 Annual Report Download - page 15

Download and view the complete annual report

Please find page 15 of the 2008 MetLife annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

|

|

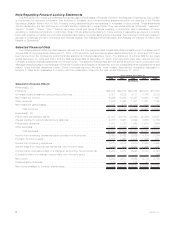

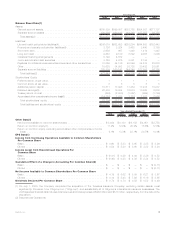

Summary of Critical Accounting Estimates

The preparation of financial statements in conformity with accounting principles generally accepted in the United States of America

(“GAAP”) requires management to adopt accounting policies and make estimates and assumptions that affect amounts reported in the

consolidated financial statements. The most critical estimates include those used in determining:

(i) the estimated fair value of investments in the absence of quoted market values;

(ii) investment impairments;

(iii) the recognition of income on certain investment entities;

(iv) the application of the consolidation rules to certain investments;

(v) the existence and estimated fair value of embedded derivatives requiring bifurcation;

(vi) the estimated fair value of and accounting for derivatives;

(vii) the capitalization and amortization of DAC and the establishment and amortization of VOBA;

(viii) the measurement of goodwill and related impairment, if any;

(ix) the liability for future policyholder benefits;

(x) accounting for income taxes and the valuation of deferred tax assets;

(xi) accounting for reinsurance transactions;

(xii) accounting for employee benefit plans; and

(xiii) the liability for litigation and regulatory matters.

The application of purchase accounting requires the use of estimation techniques in determining the estimated fair values of assets

acquired and liabilities assumed — the most significant of which relate to the aforementioned critical estimates. In applying the Company’s

accounting policies, management makes subjective and complex judgments that frequently require estimates about matters that are

inherently uncertain. Many of these policies, estimates and related judgments are common in the insurance and financial services

industries; others are specific to the Company’s businesses and operations. Actual results could differ from these estimates.

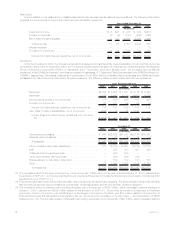

Fair Value

As described below, certain assets and liabilities are measured at estimated fair value on the Company’s consolidated balance sheets.

In addition, these footnotes to the consolidated financial statements include disclosures of estimated fair values. Effective January 1, 2008,

the Company adopted Statement of Financial Accounting Standards (“SFAS”) No. 157, Fair Value Measurements (“SFAS 157”). SFAS 157

defines fair value as the price that would be received to sell an asset or paid to transfer a liability (an exit price) in the principal or most

advantageous market for the asset or liability in an orderly transaction between market participants on the measurement date. In many

cases, the exit price and the transaction (or entry) price will be the same at initial recognition. However, in certain cases, the transaction

price may not represent fair value. Under SFAS 157, fair value of a liability is based on the amount that would be paid to transfer a liability to

a third party with the same credit standing. SFAS 157 requires that fair value be a market-based measurement in which the fair value is

determined based on a hypothetical transaction at the measurement date, considered from the perspective of a market participant. When

quoted prices are not used to determine fair value, SFAS 157 requires consideration of three broad valuation techniques: (i) the market

approach, (ii) the income approach, and (iii) the cost approach. The approaches are not new, but SFAS 157 requires that entities determine

the most appropriate valuation technique to use, given what is being measured and the availability of sufficient inputs. SFAS 157 prioritizes

the inputs to fair valuation techniques and allows for the use of unobservable inputs to the extent that observable inputs are not available.

The Company has categorized its assets and liabilities measured at estimated fair value into a three-level hierarchy, based on the priority of

the inputs to the respective valuation technique. The fair value hierarchy gives the highest priority to quoted prices in active markets for

identical assets or liabilities (Level 1) and the lowest priority to unobservable inputs (Level 3). An asset or liability’s classification within the

fair value hierarchy is based on the lowest level of significant input to its valuation. SFAS 157 defines the input levels as follows:

Level 1 Unadjusted quoted prices in active markets for identical assets or liabilities. The Company defines active markets based on

average trading volume for equity securities. The size of the bid/ask spread is used as an indicator of market activity for fixed

maturity securities.

Level 2 Quoted prices in markets that are not active or inputs that are observable either directly or indirectly. Level 2 inputs include

quoted prices for similar assets or liabilities other than quoted prices in Level 1; quoted prices in markets that are not active; or

other inputs that are observable or can be derived principally from or corroborated by observable market data for substantially

the full term of the assets or liabilities.

Level 3 Unobservable inputs that are supported by little or no market activity and are significant to the estimated fair value of the

assets or liabilities. Unobservable inputs reflect the reporting entity’s own assumptions about the assumptions that market

participants would use in pricing the asset or liability. Level 3 assets and liabilities include financial instruments whose values

are determined using pricing models, discounted cash flow methodologies, or similar techniques, as well as instruments for

which the determination of estimated fair value requires significant management judgment or estimation.

The measurement and disclosures under SFAS 157 in the accompanying financial statements and footnotes exclude certain items such

as nonfinancial assets and nonfinancial liabilities initially measured at estimated fair value in a business combination, reporting units

measured at estimated fair value in the first step of a goodwill impairment test and indefinite-lived intangible assets measured at estimated

fair value for impairment assessment. The effective date for these items was deferred to January 1, 2009.

Prior to adoption of SFAS 157, estimated fair value was determined based solely upon the perspective of the reporting entity. Therefore,

methodologies used to determine the estimated fair value of certain financial instruments prior to January 1, 2008, while being deemed

appropriate under existing accounting guidance, may not have produced an exit value as defined in SFAS 157.

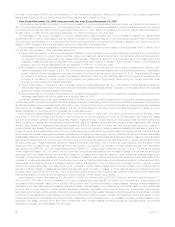

Estimated Fair Values of Investments

The Company’s investments in fixed maturity and equity securities, investments in trading securities, certain short-term investments,

most mortgage loans held-for-sale, and mortgage servicing rights (“MSRs”) are reported at their estimated fair value. In determining the

estimated fair value of these investments, various methodologies, assumptions and inputs are utilized, as described further below.

12 MetLife, Inc.