MetLife 2008 Annual Report Download - page 211

Download and view the complete annual report

Please find page 211 of the 2008 MetLife annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

201 -

202

202 -

203

203 -

204

204 -

205

205 -

206

206 -

207

207 -

208

208 -

209

209 -

210

210 -

211

211 -

212

212 -

213

213 -

214

214 -

215

215 -

216

216 -

217

217 -

218

218 -

219

219 -

220

220 -

221

221 -

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

|

|

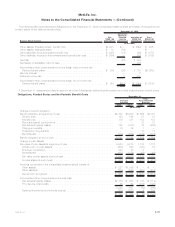

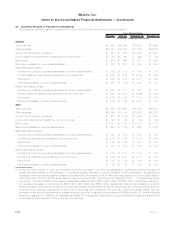

based upon the closing price of the Holding Company’s common stock on the date of grant, reduced by the present value of estimated

dividends to be paid on that stock during the performance period.

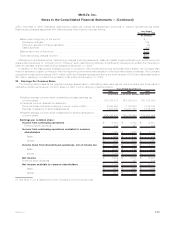

Compensation expense related to initial Performance Shares granted prior to January 1, 2006 and expected to vest is recognized

ratably during the performance period. Compensation expense related to initial Performance Shares granted on or after January 1, 2006

and expected to vest is recognized ratably over the performance period or the period to retirement eligibility, if shorter. Performance Shares

expected to vest and the related compensation expenses may be further adjusted by the performance factor most likely to be achieved, as

estimated by management, at the end of the performance period. Compensation expense of $70 million, $90 million and $74 million,

related to Performance Shares was recognized for the years ended December 31, 2008, 2007 and 2006, respectively.

At December 31, 2008, there were $57 million of total unrecognized compensation costs related to Performance Share awards. It is

expected that these costs will be recognized over a weighted average period of 1.65 years.

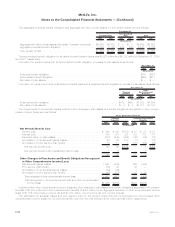

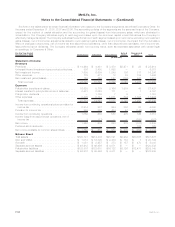

Long-Term Performance Compensation Plan

Prior to January 1, 2005, the Company granted stock-based compensation to certain members of management under the LTPCP. Each

participant was assigned a target compensation amount (an “Opportunity Award”) at the inception of the performance period with the final

compensation amount determined based on the total shareholder return on the Company’s common stock over the three-year perfor-

mance period, subject to limited further adjustment approved by the Company’s Board of Directors. Payments on the Opportunity Awards

were normally payable in their entirety (subject to certain contingencies) at the end of the three-year performance period, and were paid in

whole or in part with shares of the Company’s common stock, as approved by the Company’s Board of Directors. There were no new

grants under the LTPCP during the years ended December 31, 2008, 2007 and 2006.

A portion of each Opportunity Award under the LTPCP was settled in shares of the Holding Company’s common stock while the

remainder was settled in cash. The portion of the Opportunity Award settled in shares of the Holding Company’s common stock was

accounted for as an equity award with the fair value of the award determined based upon the closing price of the Holding Company’s

common stock on the date of grant. The compensation expense associated with the equity award, based upon the grant date fair value,

was recognized into expense ratably over the respective three-year performance period. The portion of the Opportunity Award settled in

cash was accounted for as a liability and was remeasured using the closing price of the Holding Company’s common stock on the final day

of each subsequent reporting period during the three-year performance period.

The final LTPCP performance period concluded during the six months ended June 30, 2007. Final Opportunity Awards in the amount of

618,375 shares of the Company’s common stock and $16 million in cash were paid on April 18, 2007. No significant compensation

expense related to LTPCP was recognized during the year ended December 31, 2008 and 2007. Compensation expense of $14 million

related to LTPCP Opportunity Awards was recognized for the year ended December 31, 2006.

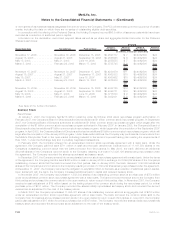

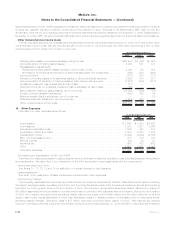

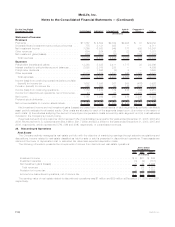

StatutoryEquityandIncome

Each insurance company’s state of domicile imposes minimum risk-based capital (“RBC”) requirements that were developed by the

National Association of Insurance Commissioners (“NAIC”). The formulas for determining the amount of RBC specify various weighting

factors that are applied to financial balances or various levels of activity based on the perceived degree of risk. Regulatory compliance is

determined by a ratio of total adjusted capital, as defined by the NAIC, to authorized control level RBC, as defined by the NAIC. Companies

below specific trigger points or ratios are classified within certain levels, each of which requires specified corrective action. Each of the

Holding Company’s U.S. insurance subsidiaries exceeded the minimum RBC requirements for all periods presented herein.

The NAIC has adopted the Codification of Statutory Accounting Principles (“Codification”). Codification is intended to standardize

regulatory accounting and reporting to state insurance departments. However, statutory accounting principles continue to be established

by individual state laws and permitted practices. The New York Insurance Department has adopted Codification with certain modifications

for the preparation of statutory financial statements of insurance companies domiciled in New York. Modifications by the various state

insurance departments may impact the effect of Codification on the statutory capital and surplus of the Holding Company’s insurance

subsidiaries.

Statutory accounting principles differ from GAAP primarily by charging policy acquisition costs to expense as incurred, establishing

future policy benefit liabilities using different actuarial assumptions, reporting surplus notes as surplus instead of debt and valuing

securities on a different basis.

In addition, certain assets are not admitted under statutory accounting principles and are charged directly to surplus. The most

significant assets not admitted by the Company are net deferred income tax assets resulting from temporary differences between statutory

accounting principles basis and tax basis not expected to reverse and become recoverable within a year. Further, statutory accounting

principles do not give recognition to purchase accounting adjustments.

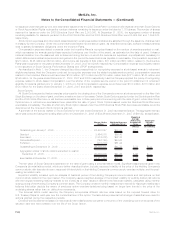

Statutory net income (loss) of Metropolitan Life Insurance Company, a New York domiciled insurer, was ($338) million, $2.1 billion and

$1.0 billion for the years ended December 31, 2008, 2007 and 2006, respectively. Statutory capital and surplus, as filed with the

Department, was $11.6 billion and $13.0 billion at December 31, 2008 and 2007, respectively.

Statutory net income of MetLife Insurance Company of Connecticut, a Connecticut domiciled insurer, was $242 million, $1.1 billion,

and $856 million for the years ended December 31, 2008, 2007 and 2006, respectively. Statutory capital and surplus, as filed with the

Connecticut Insurance Department, was $5.5 billion and $4.2 billion at December 31, 2008 and 2007, respectively.

Statutory net income of Metropolitan Property and Casualty Insurance Company (“MPC”), a Rhode Island domiciled insurer, was

$308 million, $400 million and $385 million for the years ended December 31, 2008, 2007 and 2006, respectively. Statutory capital and

surplus, as filed with the Insurance Department of Rhode Island, was $1.8 billion at both December 31, 2008 and 2007.

Statutory net income of Metropolitan Tower and Life Insurance Company (“MTL”), a Delaware domiciled insurer, was $212 million,

$103 million and $2.8 billion for the years ended December 31, 2008, 2007 and 2006, respectively. Statutory capital and surplus, as filed

with the Delaware Insurance Department was $885 million and $1.1 billion at December 31, 2008 and 2007, respectively.

F-88 MetLife, Inc.

MetLife, Inc.

Notes to the Consolidated Financial Statements — (Continued)