MetLife 2008 Annual Report Download - page 14

Download and view the complete annual report

Please find page 14 of the 2008 MetLife annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

|

|

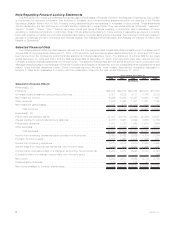

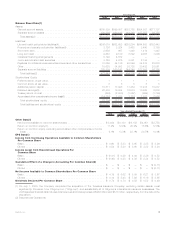

Throughout 2008 and continuing in 2009, Congress, the Federal Reserve Bank of New York, the U.S. Treasury and other agencies of

the Federal government took a number of increasingly aggressive actions (in addition to continuing a series of interest rate reductions that

began in the second half of 2007) intended to provide liquidity to financial institutions and markets, to avert a loss of investor confidence in

particular troubled institutions and to prevent or contain the spread of the financial crisis. How and to whom the U.S. Treasury distributes

amounts available under the governmental programs could have the effect of supporting some aspects of the financial services industry

more than others or provide advantages to some of our competitors. Governments in many of the foreign markets in which MetLife

operates have also responded to address market imbalances and have taken meaningful steps intended to restore market confidence. We

cannot predict whether the U.S. or foreign governments will establish additional governmental programs or the impact any additional

measures or existing programs will have on the financial markets, whether on the levels of volatility currently being experienced, the levels

of lending by financial institutions the prices buyers are willing to pay for financial assets or otherwise. See “Business — Regulation —

Governmental Responses to Extraordinary Market Conditions’’ in MetLife, Inc.’s Annual Report on Form 10-K for the year ended

December 31, 2008.

The economic crisis and the resulting recession have had and will continue to have an adverse effect on the financial results of

companies in the financial services industry, including the Company. The declining financial markets and economic conditions have

negatively impacted our investment income and the demand for and the cost and profitability of certain of our products, including variable

annuities and guarantee riders. See “— Results of Operations” and “— Liquidity and Capital Resources — Extraordinary Market

Conditions.

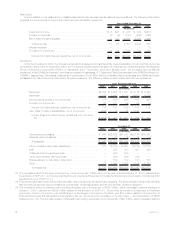

Demographics. In the coming decade, a key driver shaping the actions of the life insurance industry will be the rising income

protection, wealth accumulation and needs of the retiring Baby Boomers. As a result of increasing longevity, retirees will need to

accumulate sufficient savings to finance retirements that may span 30 or more years. Helping the Baby Boomers to accumulate assets for

retirement and subsequently to convert these assets into retirement income represents an opportunity for the life insurance industry.

Life insurers are well positioned to address the Baby Boomers’ rapidly increasing need for savings tools and for income protection. The

Company believes that, among life insurers, those with strong brands, high financial strength ratings and broad distribution, are best

positioned to capitalize on the opportunity to offer income protection products to Baby Boomers.

Moreover, the life insurance industry’s products and the needs they are designed to address are complex. The Company believes that

individuals approaching retirement age will need to seek information to plan for and manage their retirements and that, in the workplace, as

employees take greater responsibility for their benefit options and retirement planning, they will need information about their possible

individual needs. One of the challenges for the life insurance industry will be the delivery of this information in a cost effective manner.

Competitive Pressures. The life insurance industry remains highly competitive. The product development and product life-cycles have

shortened in many product segments, leading to more intense competition with respect to product features. Larger companies have the

ability to invest in brand equity, product development, technology and risk management, which are among the fundamentals for sustained

profitable growth in the life insurance industry. In addition, several of the industry’s products can be quite homogeneous and subject to

intense price competition. Sufficient scale, financial strength and financial flexibility are becoming prerequisites for sustainable growth in

the life insurance industry. Larger market participants tend to have the capacity to invest in additional distribution capability and the

information technology needed to offer the superior customer service demanded by an increasingly sophisticated industry client base. We

believe that the turbulence in financial markets that began in the latter half of 2008, its impact on the capital position of many competitors,

and subsequent actions by regulators and rating agencies have highlighted financial strength as the most significant differentiator from the

perspective of customers and certain distributors. In addition, the financial market turbulence and the economic recession have led many

companies in our industry to re-examine the pricing and features of the products they offer and may lead to consolidation in the life

insurance industry.

Regulatory Changes. The life insurance industry is regulated at the state level, with some products and services also subject to federal

regulation. As life insurers introduce new and often more complex products, regulators refine capital requirements and introduce new

reserving standards for the life insurance industry. Regulations recently adopted or currently under review can potentially impact the

reserve and capital requirements of the industry. In addition, regulators have undertaken market and sales practices reviews of several

markets or products, including equity-indexed annuities, variable annuities and group products. We expect the regulation of the financial

services industry to receive renewed scrutiny as a result of the disruptions in the financial markets in 2008. It is possible that significant

regulatory reforms could be implemented. We cannot predict whether any such reforms will be adopted, the form they will take or their

effect upon us. We also cannot predict how the various government responses to the current financial and economic difficulties will affect

the financial services and insurance industries or the standing of particular companies, including our Company, within those industries.

Pension Plans. On August 17, 2006, President Bush signed the Pension Protection Act of 2006 (“PPA”) into law. The PPA is a

comprehensive reform of defined benefit and defined contribution plan rules. The provisions of the PPA may, over time, have a significant

impact on demand for pension, retirement savings, and lifestyle protection products in both the institutional and retail markets. While the

impact of the PPA is generally expected to be positive over time, these changes may have adverse short-term effects on the Company’s

business as plan sponsors may react to these changes in a variety of ways as the new rules and related regulations begin to take effect. In

response to the current financial and economic environment, President Bush signed into the law the Worker, Retiree and Employer

Recovery Act (the “Employer Recovery Act”) in December 2008. This Act is intended to, among other things, ease the transition of certain

funding requirements of the PPA for defined benefit plans. The financial and economic environment and the enactment of the Employer

Recovery Act may delay the timing or change the nature of qualified plan sponsor actions and, in turn, affect the Company’s business.

11MetLife, Inc.